PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035160

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2035160

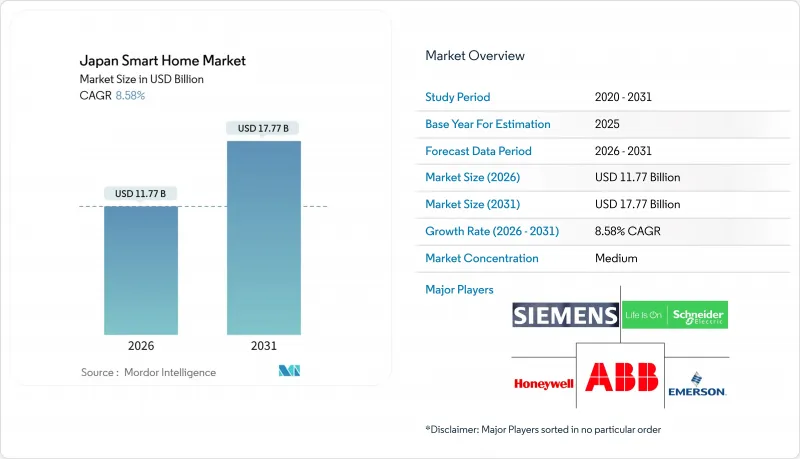

Japan Smart Home - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Japan smart home market size is USD 11.77 billion in 2026 and is projected to reach USD 17.77 billion by 2031, advancing at an 8.58% CAGR.

Strong demographic pressure from an aging population, rising energy-efficiency mandates, and government subsidies for zero-energy houses are redirecting demand from novelty devices toward assistive living and energy-management solutions. Insurance discounts for connected security equipment, the spread of Matter-certified devices, and telecom-operator bundles are further lowering adoption hurdles. Competition revolves around ecosystem lock-in, with domestic appliance majors leveraging trusted brands while global platforms subsidize voice-assistant hardware to win recurring service revenue. Thread-based sensors are mitigating Wi-Fi congestion in dense apartments, and edge AI processing is easing privacy concerns by keeping data on-device.

Japan Smart Home Market Trends and Insights

Ageing-in-Place Needs Driving Assistive Technologies

Japan's over-65 cohort reached 36.2 million in 2025, and municipalities now subsidize motion sensors, fall-detection wearables, and voice-activated lighting to let seniors remain at home rather than relocate to care facilities. Panasonic's HomeX platform integrates locks, emergency buttons, and caregiver dashboards, while NEC pilots AI anomaly detection that alerts families when routines deviate. These solutions resonate in rural prefectures where medical facilities are sparse and response times long. Uptake is accelerating as hardware bundles spread through telecom contracts that spread costs over 24 months. The demographic shift will keep assistive technology at the center of Japan smart home market growth well into the next decade.

Advances in IoT, AI, and Voice-Controlled Assistants

Cumulative Alexa and Google Assistant installations surpassed 15 million units by 2025, yet local players such as Sony embed Japanese-language AI in TVs and appliances to overcome privacy and dialect concerns. Matter 1.3 certification lets users mix Panasonic air conditioners with Sharp refrigerators under one app, reducing fragmentation that previously deterred multi-brand households. Edge AI controllers from Mitsubishi Electric optimize HVAC without sending raw data to cloud servers, aligning with strict data-residency rules. Hardware subsidies, tighter speech recognition, and cross-brand interoperability are shortening replacement cycles, and in turn enlarging the Japan smart home market base across urban and rural regions.

High Upfront Hardware and Installation Cost

A professionally installed whole-home package can top JPY 800,000 (USD 5,400), placing smart automation beyond many middle-income buyers. Import tariffs, limited economies of scale, and premium finish requirements inflate equipment prices above North American norms. Labor adds 20-30% because electricians in major cities charge more than JPY 8,000 (USD 54) per hour. Telecom bundles and subscription models spread payments over time, yet sticker shock remains the largest brake on the Japan smart home market, especially in rural districts where incomes are lower.

Other drivers and restraints analyzed in the detailed report include:

- Rising Concern About Home Security and Safety

- Government Energy-Efficiency Subsidies for Smart Devices

- Interoperability and Legacy System Issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Security devices will generate the highest incremental revenue, advancing at a 10.81% CAGR through 2031 as insurers incentivize adoption and urban residents seek remote monitoring. Smart appliances nonetheless dominated the Japan smart home market share at 27.43% in 2025 on the back of Panasonic, Hitachi, and Sharp ecosystems that sync with energy-management dashboards.

Security offerings now bundle biometric locks, AI cameras, and cloud storage, creating service revenue that offsets hardware price erosion. Control hubs and speakers from Amazon and Google bridge multiple devices, while home entertainment rivals seek growth in rural prefectures where broadband rollout is closing the digital divide. Energy-management devices are mandated in zero-energy houses, forcing manufacturers to integrate across formerly stand-alone categories and compressing margins in single-function product lines.

Wi-Fi accounted for 45.12% of connectivity in 2025 thanks to existing router infrastructure, yet Thread sensors are set to erode share with a 9.23% CAGR through 2031. Thread's low-power mesh reduces battery drain and network congestion in dense apartments, traits valued by younger renters who lead DIY purchases.

Bluetooth remains popular for smart speakers and locks, though range limits restrict full-home coverage. Z-Wave adoption lags due to frequency restrictions and limited vendor support. Matter certification is accelerating cross-brand compatibility, and IPv6 transition is laying groundwork for massive device counts in future smart-city deployments, keeping interoperability front and center in the Japan smart home market size expansion.

The Japan Smart Home Market Report is Segmented by Product Type (Comfort and Lighting, Control and Connectivity, and More), Technology (Wi-Fi, Bluetooth, Zigbee, Z-Wave, and More), Sales Channel (Offline Retail, Online Retail, Professional Installer, and More), Installation Type (DIY, and Professional), Dwelling Type (Detached Houses, Apartments, and More). The Market Forecasts are in Value (USD).

List of Companies Covered in this Report:

- Schneider Electric SE

- Emerson Electric co.

- ABB Ltd

- Honeywell International Inc.

- Siemens AG

- Signify Holding

- Microsoft Corporation

- Google LLC

- Buffalo Inc.

- Hitachi Ltd.

- Zhejiang Dahua Technology Co., Ltd.

- D-Link Corporation

- Panasonic Holdings Corporation

- Sony Group Corp.

- Mitsubishi Electric Corporation

- Toshiba Corporation

- NEC Corporation

- Sharp Corporation

- Amazon.com Inc.

- Rakuten Group Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Concern About Home Security and Safety

- 4.2.2 Advances in IoT, AI and Voice-Controlled Assistants

- 4.2.3 Ageing-in-Place Needs Driving Assistive Technologies

- 4.2.4 Government Energy-Efficiency Subsidies for Smart Devices

- 4.2.5 Smart-City Pilot Subsidies Integrating Residential Data

- 4.2.6 Property-Insurance Discounts for Smart-Home Devices

- 4.3 Market Restraints

- 4.3.1 High Upfront Hardware and Installation Cost

- 4.3.2 Interoperability and Legacy System Issues

- 4.3.3 Data-Residency Rules Limiting Foreign Cloud Platforms

- 4.3.4 Shortage of Certified Installers in Rural Prefectures

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Technological Outlook

- 4.7 Regulatory Landscape

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Comfort and Lighting

- 5.1.1.1 Smart Lighting (Bulbs, Switches, Dimmers)

- 5.1.1.2 Smart Curtains/Blinds

- 5.1.2 Control and Connectivity

- 5.1.2.1 Smart Hubs/Controllers

- 5.1.2.2 Smart Speakers

- 5.1.3 Energy Management

- 5.1.3.1 Smart Thermostats

- 5.1.3.2 Smart Meters

- 5.1.4 Home Entertainment

- 5.1.4.1 Smart TVs

- 5.1.4.2 Streaming Devices

- 5.1.5 Security

- 5.1.5.1 Smart Cameras

- 5.1.5.2 Smart Doorbells

- 5.1.5.3 Smart Locks

- 5.1.6 Smart Appliances

- 5.1.6.1 Smart Refrigerators

- 5.1.6.2 Smart Washing Machines

- 5.1.7 HVAC Control

- 5.1.7.1 Smart Air-Conditioners

- 5.1.1 Comfort and Lighting

- 5.2 By Technology

- 5.2.1 Wi-Fi

- 5.2.2 Bluetooth

- 5.2.3 Zigbee

- 5.2.4 Z-Wave

- 5.2.5 Thread

- 5.2.6 Other Technologies (LTE, PLC, etc.)

- 5.3 By Sales Channel

- 5.3.1 Offline Retail/CE Stores

- 5.3.2 Online Retail and Marketplaces

- 5.3.3 Professional Installer/Dealer Channel

- 5.3.4 Telecom-Operator Bundles

- 5.4 By Installation Type

- 5.4.1 DIY (Self-Install)

- 5.4.2 Professional Install

- 5.5 By Dwelling Type

- 5.5.1 Detached Houses

- 5.5.2 Apartments and Condominiums

- 5.5.3 Other Dwelling Types

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Emerson Electric co.

- 6.4.3 ABB Ltd

- 6.4.4 Honeywell International Inc.

- 6.4.5 Siemens AG

- 6.4.6 Signify Holding

- 6.4.7 Microsoft Corporation

- 6.4.8 Google LLC

- 6.4.9 Buffalo Inc.

- 6.4.10 Hitachi Ltd.

- 6.4.11 Zhejiang Dahua Technology Co., Ltd.

- 6.4.12 D-Link Corporation

- 6.4.13 Panasonic Holdings Corporation

- 6.4.14 Sony Group Corp.

- 6.4.15 Mitsubishi Electric Corporation

- 6.4.16 Toshiba Corporation

- 6.4.17 NEC Corporation

- 6.4.18 Sharp Corporation

- 6.4.19 Amazon.com Inc.

- 6.4.20 Rakuten Group Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment