PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043827

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043827

Electrocoating (E-coat) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

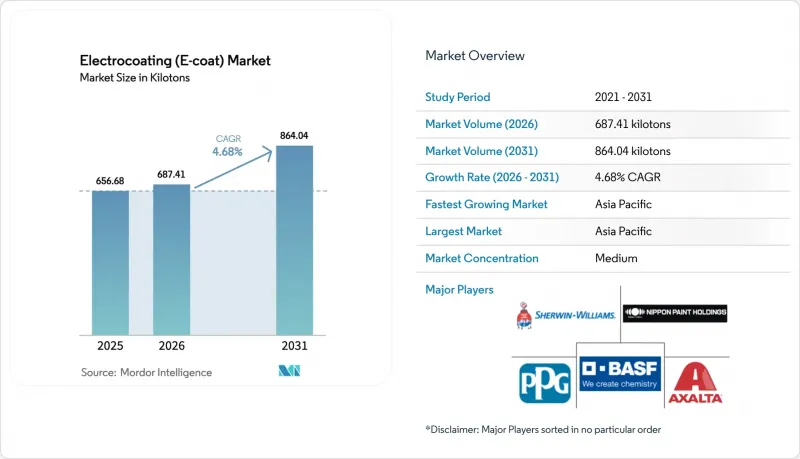

The Electrocoating Market size is projected to expand from 656.68 kilotons in 2025 and 687.41 kilotons in 2026 to 864.04 kilotons by 2031, registering a CAGR of 4.68% between 2026 to 2031.

Three key shifts are reshaping the landscape: the Asia-Pacific region is increasing its vehicle production, electric-vehicle (EV) battery housings now mandate dielectric shielding for systems surpassing 800 V, and agricultural-equipment assembly is moving closer to home in the Latin America region. This realignment is shifting coating demand away from traditional centers in Europe and North America. Cathodic epoxy systems, known for their high dielectric strength and impressive transfer efficiency, have emerged as the preferred choice. This advantage enables automotive and appliance OEMs to not only adhere to stringent corrosion and sustainability benchmarks but also to significantly reduce volatile organic compound (VOC) emissions compared to conventional spray primers.

Global Electrocoating (E-coat) Market Trends and Insights

Automotive Production Growth in Asia-Pacific

In 2024, the Asia-Pacific region produced a significant number of vehicles, with China and India being major contributors. This output solidified the region's dominance in structural coating demand. To meet a decade-long OEM corrosion warranty, every body-in-white underwent cathodic e-coat immersion. Following a GST reduction in 2025, India's local vehicle sales experienced substantial growth, compelling toll coaters to implement second shifts. Both Thailand and South Korea saw similar upticks. Additionally, as EVs now bear heavier battery packs, regulations mandate thicker films on their underbodies. With production concentrated in specific areas, formulators strategically co-located plants, effectively mitigating inventory risks associated with short-shelf-life epoxy dispersions. These trends are projected to account for a significant portion of the Electrocoating market volume by 2031.

Superior Corrosion-Resistance vs. Solvent-Borne Primers

Cathodic e-coat exhibits superior salt-spray durability compared to solvent primers. This advantage has become more prominent as OEM warranties have extended. Due to its high transfer efficiency, overspray waste is significantly reduced, leading to lower VOC output per vehicle. This development facilitates compliance with U.S. EPA Tier 3 and EU Stage V regulations. BASF's CathoGuard 800 RE has successfully reduced bake temperatures, which decreases natural gas consumption while maintaining optimal edge coverage. Although establishing a greenfield dip line requires substantial investment, spreading this cost over time ensures that the per-unit coating expense remains competitive, supporting the growth of the Electrocoating market during the forecast period of 2026-2031.

Limited UV Stability for Exterior Plastic Parts

Extended exposure to 340 nm UV light causes epoxy e-coats to chalk. Consequently, OEMs often apply powder clearcoats or choose acrylic primers, particularly on bumpers and mirror caps. While acrylic e-coats preserve their gloss after extended QUV-A exposure, epoxy e-coats do not fare as well. However, acrylics have limitations, lacking in edge-coverage toughness and dielectric strength. In sun-drenched regions like the Middle-East and Australia, premium vehicle programs are gravitating towards unpainted black plastics. This trend has resulted in a decreased e-coatable surface per unit. Current patent filings indicate no forthcoming advancements in resin technology, posing a continuing challenge for the Electrocoating market, with projections extending through the forecast period of 2026-2031.

Other drivers and restraints analyzed in the detailed report include:

- EV Battery Housings Adopting E-Coat for Dielectric Shielding

- Nano-Enabled Formulas Improving Throw Power

- Skilled-Operator Gap for Automated Dip-Tank Processes

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, cathodic systems dominated the market, capturing 97.72% of the volume, and are projected to grow at a compound annual growth rate (CAGR) of 4.67% during the forecast period of 2026-2031. Their dominance is attributed to features such as a high salt-spray endurance and strong dielectric ratings, both of which are crucial for modern electric vehicle (EV) bodies. This segment represented a significant portion of the Electrocoating market in 2025. Ongoing reformulations ensure that cathodic options remain compliant with EU REACH regulations while maintaining strong edge-coverage ratios. Although anodic e-coat occupies a small niche for aluminum extrusions, benefiting from oxide formation that enhances adhesion, its growth rate lags behind the broader Electrocoating market. Anodic baths, which dissolve more metal and generate higher sludge loads, have led many architects and appliance original equipment manufacturers (OEMs) to shift toward powder coatings. This transition, while limiting anodic coatings' growth potential, highlights their favorable adhesion properties on non-ferrous substrates.

Despite the near-monopoly of cathodic technology, which stifles new entrants, opportunities exist in bio-based epoxy dispersions and nano-pigment packages. These innovations could further optimize film build in concealed cavities. Given that ISO 12944 qualification cycles span up to 24 months, any disruptive chemistries aiming to challenge established cathodic suppliers must demonstrate clear sustainability or cost advantages. Looking ahead, anodic coatings are expected to maintain a small market share in the Electrocoating sector through 2031, focusing primarily on architectural aluminum and select consumer electronics housings.

The Electrocoating Market Report is Segmented by Type (Cathodic and Anodic), Technology (Epoxy Coating Technology and Acrylic Coating Technology), Application (Passenger Cars, Commercial Vehicles, Automotive Parts and Accessories, Heavy Duty Equipment, Appliances, and Other Applications), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

In 2025, the Asia-Pacific region dominated the electrocoating market, accounting for 55.45% of the volume. Projections indicate steady growth at a CAGR of 5.05% during the forecast period of 2026-2031. China's robust output, coupled with a sales surge in India, driven by the GST, fuels this expansion. In 2025, China's production of BEVs spiked the demand for dielectric shielding. Concurrently, Thailand and South Korea rolled out hybrid lines, necessitating thicker 25 μm films for their heavier battery packs. Japan's pivot towards hybrids has ensured its base volumes remain stable.

North America, boasting a significant share in 2025, is poised for consistent growth. Mexico's export boom has spurred the creation of new dip tanks in Guanajuato and Queretaro, serving both automotive and agricultural machinery frames. However, a notable write-down on EV assets has tempered enthusiasm for ultra-high-voltage battery trays. In the United States, a shortage of skilled operators has constrained capacity utilization, inching first-pass yields towards their optimal mark.

Europe, commanding a substantial portion of the 2025 volume, is on a steady growth path. The region faced hurdles with a slower-than-expected BEV adoption and stringent tin catalyst restrictions, resulting in costly reformulations. While Germany led the demand charge, the United Kingdom and Italy experienced volume declines as OEMs pivoted to more cost-effective eastern plants. South America, with its modest share, saw growth driven by tractor nearshoring in Brazil and Argentina. In contrast, the Middle-East lagged, hindered by limited local vehicle assembly and a reliance on pre-coated imports.

- Axalta Coating Systems

- B.L DOWNEY Company LLC

- BASF SE

- Burkard Industries

- Dymax Corporation

- Electro Coatings Inc.

- Greenkote

- H.E. Orr Company

- Hawking Electrotechnology Limited

- Henkel AG & Co. KGaA

- Lippert Components Inc.

- Nippon Paint Holdings Co., Ltd.

- PPG Industries Inc.

- The Sherwin-Williams Company

- Valmont Industries Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Dynamics

- 4.1 Drivers

- 4.1.1 Automotive production growth in Asia-Pacific

- 4.1.2 Superior corrosion-resistance vs. solvent-borne primers

- 4.1.3 EV battery housings adopting e-coat for dielectric shielding

- 4.1.4 Nano-enabled formulas improving edge-coverage and throw-power

- 4.1.5 Nearshoring of ag-equipment production in LATAM Countries

- 4.2 Restraints

- 4.2.1 Limited UV stability for exterior plastic parts

- 4.2.2 Skilled-operator gap for automated dip-tank processes

- 4.2.3 Volatile supply of bio-based epoxy dispersions

- 4.3 Industry Value Chain Analysis

- 4.4 Porter's Five Forces Analysis

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Consumers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitute Products and Services

- 4.4.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Type

- 5.1.1 Cathodic

- 5.1.2 Anodic

- 5.2 By Technology

- 5.2.1 Epoxy Coating Technology

- 5.2.2 Acrylic Coating Technology

- 5.3 By Application

- 5.3.1 Passenger Cars

- 5.3.2 Commercial Vehicles

- 5.3.3 Automotive Parts and Accessories

- 5.3.4 Heavy Duty Equipment

- 5.3.5 Appliances

- 5.3.6 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 Italy

- 5.4.3.4 France

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Axalta Coating Systems

- 6.4.2 B.L DOWNEY Company LLC

- 6.4.3 BASF SE

- 6.4.4 Burkard Industries

- 6.4.5 Dymax Corporation

- 6.4.6 Electro Coatings Inc.

- 6.4.7 Greenkote

- 6.4.8 H.E. Orr Company

- 6.4.9 Hawking Electrotechnology Limited

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Lippert Components Inc.

- 6.4.12 Nippon Paint Holdings Co., Ltd.

- 6.4.13 PPG Industries Inc.

- 6.4.14 The Sherwin-Williams Company

- 6.4.15 Valmont Industries Inc.

7 Market Opportunities and Future Trends

- 7.1 White-space and Unmet-need Assessment