PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043832

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043832

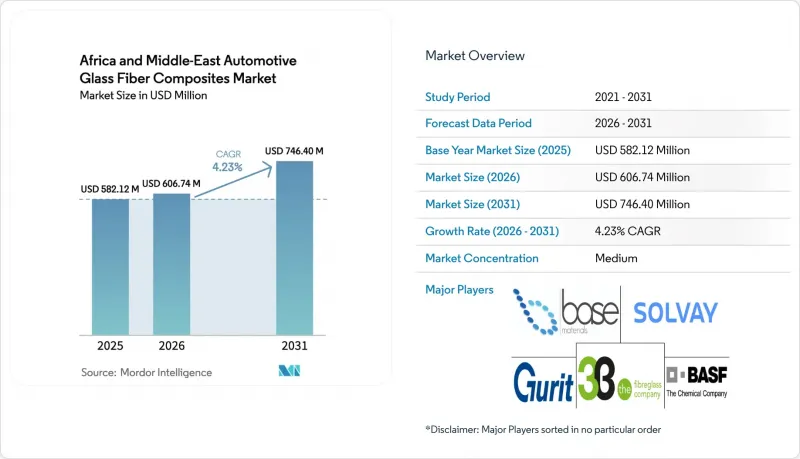

Africa And Middle-East Automotive Glass Fiber Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Africa And Middle-East Automotive Glass Fiber Composites Market size is projected to be USD 582.12 million in 2025, USD 606.74 million in 2026, and reach USD 746.40 million by 2031, growing at a CAGR of 4.23% from 2026 to 2031. A shift in policy toward downstream processing in the Gulf, coupled with domestic-content mandates in key African assembly hubs, is driving investment away from basic hydrocarbon exports toward value-added composite molding. Saudi Arabia's allocation of USD 987 million from the Public Investment Fund to CEER suppliers in February 2026 highlights this transition, as the program supports tooling for glass-fiber door modules and battery trays. GCC lightweighting regulations and UAE tax incentives are reducing entry barriers for European molders, although logistical challenges through the Red Sea continue to increase the cost of imported roving. African CKD plants are replacing stamped steel with hand-laid composites to meet localization requirements, despite technician shortages in South Africa and Egypt leading to quality rejections under ISO 527 tensile tests.

Africa And Middle-East Automotive Glass Fiber Composites Market Trends and Insights

Regulatory Push for Fuel-Efficient Lightweighting

Saudi Arabia's SASO 2864:2019 standard lowers fleet consumption to 5.8 L/100 km by 2028, forcing automakers to remove 80-120 kg per vehicle through material substitution. Glass-fiber panels deliver 25-30% weight savings versus mild steel and remain cost-competitive against carbon fiber. The UAE starts EURO 6B in January 2026 and moves to EURO 6D by 2030, increasing pressure on OEMs to amortize lightweight components across GCC runs. While the rules accelerate composite uptake, end-of-life recycling gaps persist because thermoset glass fiber cannot be remelted, raising the prospect of landfill surcharges after 2028.

Shift to Battery-Electric Powertrains Raises Glass-Fiber Demand for EV Enclosures

SGL Carbon's glass-fiber battery enclosure for BMW's iX trims pack weight by 15% compared with aluminum housing. CEER's prototype sedan mirrors this approach with a glass-fiber lower tray that offsets its 600 kg battery. Resin-transfer molding offers complex geometries without the capital intensity of aluminum presses, a key benefit for African plants with tight budgets. Egypt's Dr. Greiche will open a USD 16.2 million infusion line in Q4 2026 to supply EV underbody shields, underscoring the cross-over between traditional glazing firms and composite components.

Volatile Glass-Fiber Import Prices Due to Red Sea Freight Premiums

Houthi attacks in 2024 caused 28% of Asia-to-Europe cargo to be rerouted via the Cape of Good Hope, leading to a 150-200% increase in freight rates. This raised the landed cost of Chinese and Indian rovings by 12-18% for Egyptian and Kenyan molders without hedging tools. Even after the conflict subsides, insurers have added an 8-10% surcharge to premiums, expected to remain through 2027, embedding structural volatility into the Africa and Middle-East automotive glass fiber composites market.

Other drivers and restraints analyzed in the detailed report include:

- Localisation Incentives in Saudi and UAE Tier-1 Supply Chains

- Surge in CKD/IKD Assembly Plants Across Africa Adopting Low-CAPEX Hand Lay-Up Parts

- Shortage of Certified Composite Technicians Causing OEM Quality Rejections

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Compression molding accounted for 34.28% of revenue in 2025, remaining a key production method in the Africa and Middle-East automotive glass fiber composites market. Advanced Fibreform's 12 presses produce over 3,000 parts weekly for Toyota and Isuzu pickups. Vacuum infusion processing is projected to grow at a 4.47% CAGR through 2031, driven by demand for complex, void-free laminates in EV battery trays and underbody shields. Johns Manville's USD 55 million Ohio line expansion aims to meet this demand, with output designated for GCC importers.

Hand lay-up continues to be utilized in CKD operations producing fewer than 15,000 units, offering a cost-effective solution to meet local-content regulations in Algeria, Egypt, and Kenya. Resin-transfer molding is used for niche structural components like seat frames, where fiber architecture is critical. Injection-molded short-fiber compounds are employed for high-volume interior brackets.

The Africa and Middle-East Automotive Glass Fiber Composites Market Report is Segmented by Production Type (Compression Molding, Hand Lay-Up, and More), Application Type (Exterior, Structural Assembly, Powertrain Components, Interior, and Other Application Types), and Geography (South Africa, Egypt, United Arab Emirates, Saudi Arabia, and Rest of Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3B - the fibreglass company

- Base Materials Ltd.

- BASF

- BorgWarner

- Chongqing Polycomp International Corporation (CPIC)

- Far-UK

- General Motors Company

- Gurit Holding AG

- Hexcel Corporation

- Johns Manville

- LyondellBasell

- Nippon Electric Glass

- Praana Group

- Saint-Gobain Vetrotex

- SGL Carbon

- Solvay

- Taishan Fiberglass

- Teijin Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Regulatory push for fuel-efficient lightweighting

- 4.2.2 Shift to battery-electric powertrains raises glass-fiber demand for EV enclosures

- 4.2.3 Localisation incentives in Saudi and UAE Tier-1 supply chains

- 4.2.4 Growing demand for corrosion-resistant composites in desert climates (fleets/buses)

- 4.2.5 Surge in CKD/IKD assembly plants across Africa adopting low-CAPEX hand lay-up parts

- 4.3 Market Restraints

- 4.3.1 Volatile glass-fiber import prices due to Red Sea freight premiums

- 4.3.2 Limited regional Tier-2 resin formulators inflating composite costs

- 4.3.3 Shortage of certified composite technicians causing OEM quality rejections

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Production Type

- 5.1.1 Compression Molding

- 5.1.2 Hand Lay-up

- 5.1.3 Resin Transfer Molding

- 5.1.4 Vacuum Infusion Processing

- 5.1.5 Injection Molding

- 5.2 By Application Type

- 5.2.1 Exterior

- 5.2.2 Structural Assembly

- 5.2.3 Powertrain Components

- 5.2.4 Interior

- 5.2.5 Other Application Types

- 5.3 By Geography

- 5.3.1 South Africa

- 5.3.2 Egypt

- 5.3.3 United Arab Emirates

- 5.3.4 Saudi Arabia

- 5.3.5 Rest of Middle-East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3B - the fibreglass company

- 6.4.2 Base Materials Ltd.

- 6.4.3 BASF

- 6.4.4 BorgWarner

- 6.4.5 Chongqing Polycomp International Corporation (CPIC)

- 6.4.6 Far-UK

- 6.4.7 General Motors Company

- 6.4.8 Gurit Holding AG

- 6.4.9 Hexcel Corporation

- 6.4.10 Johns Manville

- 6.4.11 LyondellBasell

- 6.4.12 Nippon Electric Glass

- 6.4.13 Praana Group

- 6.4.14 Saint-Gobain Vetrotex

- 6.4.15 SGL Carbon

- 6.4.16 Solvay

- 6.4.17 Taishan Fiberglass

- 6.4.18 Teijin Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment