PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043833

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043833

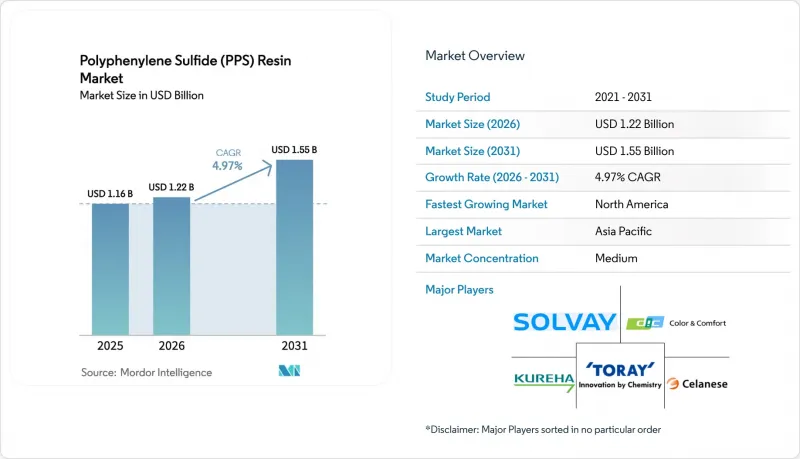

Polyphenylene Sulfide (PPS) Resin - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Polyphenylene Sulfide Resin Market size was valued at USD 1.16 billion in 2025 and is estimated to grow from USD 1.22 billion in 2026 to reach USD 1.55 billion by 2031, at a CAGR of 4.97% during the forecast period (2026-2031).

Driven by the miniaturization of electronics, a surge in hydrogen fuel-cell systems, and upgrades in industrial flue-gas filtration that require consistent service above 190°C, the market is witnessing steady momentum. The Asia-Pacific region leads in consumption, while North America is catching up, spurred by battery onshoring incentives. Meanwhile, Europe is pivoting toward halogen-free, flame-retardant resins. Although price increases are being moderated by capacity expansions in China, established suppliers are strategically repositioning themselves, focusing on specialty grades, vertically integrating into compounding, and enhancing digital processes. In essence, the Polyphenylene Sulfide (PPS) resin market is grappling with cost pressures but is distinctly shifting toward high-temperature, regulatory-compliant applications, an area where commodity thermoplastics struggle.

Global Polyphenylene Sulfide (PPS) Resin Market Trends and Insights

Miniaturized 5G and AI Electronics Need Dielectric-Stable PPS

5G millimeter-wave radios and edge AI hardware require substrates that not only exhibit low dielectric loss above 10 GHz but can also withstand lead-free solder reflow at 260°C. Newly commercialized low-dielectric PPS films meet these stringent criteria, boasting minimal moisture uptake and maintaining mechanical integrity even under repeated thermal shocks. Smartphone manufacturers, automotive ECU suppliers, and base-station producers are increasingly adopting these films as cost-effective alternatives to liquid-crystal polymers. In tandem with the expansion of 5G, industry giants Toray, DIC, and Unitika have rolled out new capacities in recent years. This collective momentum is propelling the Polyphenylene Sulfide (PPS) resin market, particularly in high-frequency connectors and antenna housings, which must achieve UL 94 V-0 standards at thinner sections without relying on halogenated additives.

Shift to Chlorine-Free PPS Grades After 2025 US and EU Toxicity Regulations

In 2025, Dechlorane Plus was added to the EU's Persistent Organic Pollutants Regulation, with a near-zero allowable concentration set for 2028. This regulatory shift has spurred electronics OEMs to move away from halogenated flame retardants. Importantly, PPS naturally meets the UL 94 V-0 standard at thin sections, enabling suppliers to avoid costly reformulations. Responding to the surging demand for halogen-free solutions, new compounding plants in Germany and the United States began operations in 2025, drastically cutting lead times for clients in Europe and North America. This rapid regulatory adaptation is expected to resonate with Asia-Pacific exporters, positioning the Polyphenylene Sulfide (PPS) resin market as the preferred choice for compliance across diverse value chains.

Rising Competition from Lower-Cost High-Temperature Nylons

Polyphthalamides have secured a Comparative Tracking Index of 600 V and achieved UL 94 V-0 certification at a thickness of 0.4 mm. These materials, processed in molds at temperatures between 90-110°C, are now rivaling PPS in numerous automotive connectors. In 2025, BASF introduced its Ultramid T6000. Although a continuous-use temperature range of 150-160°C is adequate, OEMs are adjusting specifications to reduce bills of material, thereby decreasing their stake in the cost-sensitive Polyphenylene Sulfide (PPS) resin market.

Other drivers and restraints analyzed in the detailed report include:

- On-Board Hydrogen Fuel-Cell Balance-of-Plant Adoption

- AI-Optimized Compounding Cuts Scrap and Widens PPS Use

- Recycling End-of-Life Hurdles for Cross-Linked PPS

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Linear PPS held a 56.11% share of the Polyphenylene Sulfide (PPS) resin market and is projected to grow at a 5.03% CAGR through the forecast period of 2026-2031. Its lower viscosity and compatibility with standard injection equipment make Linear PPS ideal for thin-wall molding, particularly in automotive high-voltage connectors and pump impellers. Cured PPS, which undergoes post-polymerization cross-linking, maintains tight dimensional tolerances above 200°C and is used in niche applications such as aerospace ducts and industrial pump parts. Branched PPS offers a higher modulus while ensuring recyclability, making it suitable for structural components in electric vehicle (EV) batteries. In 2024, DIC launched a plateable PPS compound for 5G antenna housings, enabling direct metallization and eliminating the need for metal inserts, thereby reducing weight. This broadened application spectrum boosts the volume of linear and branched grades, while specialty cured variants command premium prices.

The Polyphenylene Sulfide (PPS) Resin Market Report is Segmented by Type (Linear PPS, Cured PPS, and Branched PPS), End-User Industry (Automotive, Electrical and Electronics, Industrial, Aerospace, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, South America, Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region dominated the Polyphenylene Sulfide (PPS) resin market, accounting for 67.26% of its size. This leadership position was strengthened by the burgeoning production of new-energy vehicles and a thriving electronics supply chain in nations such as China, Japan, South Korea, and Taiwan. China's production capacity saw a boost in 2024, with forecasts suggesting it could more than double by 2027, thanks to the momentum from several large-scale projects. In response to these market shifts, established suppliers are now focusing on differentiated grades and enhanced technical services to counter heightened price competition.

North America is on a growth trajectory, boasting the fastest rate at a CAGR of 5.16% through the forecast period of 2026-2031, driven by robust domestic investments in batteries and hydrogen. This growth is further supported by local consumption of PPS at Fortron Industries' Wilmington plant.

On the other hand, Europe faces challenges with its stringent halogen and recycled-content regulations. While these rules open doors for substitutions, they also inflate compliance costs, making it tough for smaller converters. Meanwhile, South America, the Middle-East, and Africa are emerging as fledgling markets, with their limited demand for PPS being spurred by industrial filtration and oil-and-gas applications.

- Celanese Corporation

- Chengdu Letian Plastics Co. , Ltd

- Chevron Phillips Chemical Company LLC.

- DIC Corporation

- Ensinger

- Glion

- IDEMITSU FINE COMPOSITES CO., LTD.

- Kolon Plastics Inc.

- KUREHA CORPORATION

- NHU Materials Co.

- Polyplastics Co. Ltd

- RTP Company

- SABIC

- SK Innovation

- Solvay

- TEIJIN LIMITED.

- TORAY INDUSTRIES, INC.

- Tosoh Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Drivers

- 4.1.1 Miniaturised 5G/AI electronics need dielectric-stable PPS

- 4.1.2 Shift to chlorine-free PPS grades after 2025 US/EU tox regs

- 4.1.3 On-board hydrogen fuel-cell balance-of-plant adoption

- 4.1.4 AI-optimised compounding cuts scrap and widens PPS use

- 4.1.5 Rapid Asia-Pacific filter-bag upgrades for ultra-low-NOx boilers

- 4.2 Market Restraints

- 4.2.1 Rising competition from lower-cost high-temp nylons

- 4.2.2 Recycling-end-of-life hurdles for cross-linked PPS

- 4.2.3 Talent gap in high-temperature polymer processing

- 4.3 Value Chain Analysis

- 4.4 Porter's Five Forces

- 4.4.1 Bargaining Power of Suppliers

- 4.4.2 Bargaining Power of Buyers

- 4.4.3 Threat of New Entrants

- 4.4.4 Threat of Substitutes

- 4.4.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Linear PPS

- 5.1.2 Cured PPS

- 5.1.3 Branched PPS

- 5.2 By End-user Industry

- 5.2.1 Automotive

- 5.2.2 Electrical and Electronics

- 5.2.3 Industrial

- 5.2.4 Aerospace

- 5.2.5 Other End-user Industries

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 India

- 5.3.1.3 Japan

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 Italy

- 5.3.3.4 France

- 5.3.3.5 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Celanese Corporation

- 6.4.2 Chengdu Letian Plastics Co. , Ltd

- 6.4.3 Chevron Phillips Chemical Company LLC.

- 6.4.4 DIC Corporation

- 6.4.5 Ensinger

- 6.4.6 Glion

- 6.4.7 IDEMITSU FINE COMPOSITES CO., LTD.

- 6.4.8 Kolon Plastics Inc.

- 6.4.9 KUREHA CORPORATION

- 6.4.10 NHU Materials Co.

- 6.4.11 Polyplastics Co. Ltd

- 6.4.12 RTP Company

- 6.4.13 SABIC

- 6.4.14 SK Innovation

- 6.4.15 Solvay

- 6.4.16 TEIJIN LIMITED.

- 6.4.17 TORAY INDUSTRIES, INC.

- 6.4.18 Tosoh Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment