PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043837

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043837

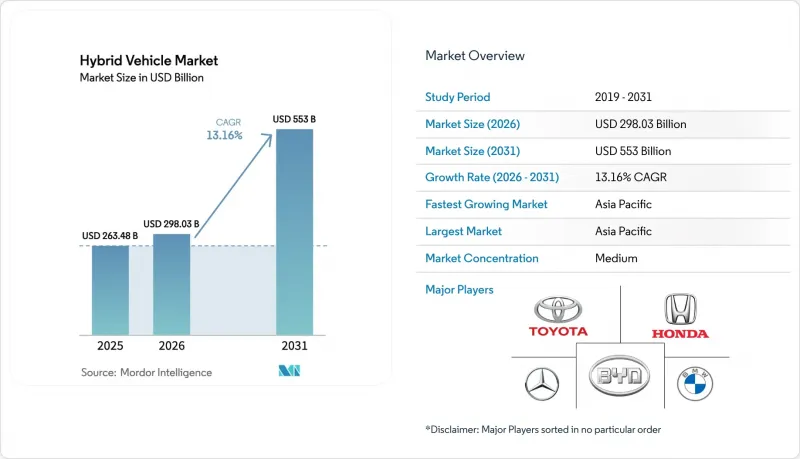

Hybrid Vehicle - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The hybrid vehicle market size is expected to grow from USD 263.48 billion in 2025 to USD 298.03 billion in 2026, and is forecast to reach USD 553 billion by 2031, at a CAGR of 13.16% during the forecast period (2026-2031).

Tightening global greenhouse gas rules, falling battery costs, and multipathway powertrain strategies are simultaneously expanding demand and protecting automakers from an uncertain pace of electrification. Plug-in hybrids are the fastest-growing configuration due to declines in battery pack costs and policy credits that reward electric-only range. In contrast, conventional hybrids maintain volume leadership because they impose the lightest burden on charging infrastructure. Permanent-magnet motors still dominate, but induction architectures are gaining as manufacturers reduce exposure to rare-earth supply risks. Lithium-iron-phosphate chemistry is now the battery of choice in most hybrids because it strikes a balance between cost, safety, and cycle life. Competition is intensifying as Japanese incumbents defend engineering leads against Chinese brands that leverage in-house battery production to undercut prices.

Global Hybrid Vehicle Market Trends and Insights

Battery Cost-Parity Tipping Point for PHEVs by 2027

By the mid-term future, automakers are steering towards significantly lower lithium-ion pack costs. Ford, in its recent earnings call, revealed a substantial year-on-year drop in the F-150 PowerBoost pack cost, attributing the decline to the United States-sourced lithium-hydroxide contracts . General Motors has set its sights on introducing plug-in crossovers with a competitive price premium, a strategic move that would negate the cost penalty seen in earlier years. Toyota, in its latest report, affirmed that the Prius Prime's battery cost per kilowatt-hour has fallen to a level that allows the company to maintain a healthy operating margin despite price reductions . With rapid cell-to-pack integration, reduced cobalt content, and a surge in LFP usage, plug-in hybrids are on track to match the sticker prices of gasoline models in the upcoming cycle.

Stricter Global CAFE/GHG Norms & Zero-Emission Mandates

Regulatory tightening is the primary driver of the surge in hybrid adoption. The U.S. Environmental Protection Agency has set stringent light-duty standards for the near future, mandating significantly lower fleet emissions. This move pushes manufacturers to integrate electrified drivetrains or face hefty penalties. Meanwhile, Europe's upcoming regulations will require real-world emissions compliance under all ambient conditions. This has led to the adoption of mild-hybrids, even in compact cars. In China, the dual-credit scheme offers substantial incentives for each plug-in hybrid electric vehicle. This incentive enables OEMs to balance out their internal-combustion deficits . In California, the Advanced Clean Cars II initiative recognizes plug-in hybrids in zero-emission quotas, provided they meet a specific electric range requirement. This requirement is not only boosting battery sizes but also providing a buffer for compliance. Together, these regulatory measures are shaping the hybrid landscape, ensuring sustained demand through the end of the decade.

BEV Total-Cost-of-Ownership Parity Achieved in Urban Fleets

In cities with affordable electricity and depot charging, battery-electric vans are proving to be more cost-effective over the long term than their plug-in hybrid counterparts. In early 2025, Amazon announced plans to phase out its plug-in hybrid vans within a few years, citing that Rivian's battery-electric vehicles (BEVs) offer superior uptime and reduced maintenance costs. Similarly, UPS highlighted a significant reduction in the cost per mile for its all-electric trucks operating on European city routes, underscoring a broader industry trend away from plug-in hybrids for fleets with set routes. London's Ultra Low Emission Zone has introduced daily fees for hybrids not operating in a zero-emission mode, diminishing their financial advantage over BEVs. With more cities likely to adopt similar measures, urban fleets might leap directly from diesel to fully electric vehicles, bypassing hybrids altogether.

Other drivers and restraints analyzed in the detailed report include:

- Soaring Fuel-Price Volatility Post-2024

- OEM Multi-Pathway Carbon Strategies

- Scarcity of Sustainably Mined Nickel & Cobalt

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Traditional hybrid electric vehicles held 41.37% of the hybrid vehicle market share in 2025, whereas plug-in hybrids are on track to log a 13.17% CAGR to 2031. This leadership reflects the minimal charging dependency of standard hybrids, a decisive advantage in grids where public chargers remain scarce. Plug-in hybrids, however, benefit from larger policy credits, and their batteries are steadily dropping in cost, allowing OEMs to price them near gasoline trim levels. BYD's Qin Plus DM-i undersells conventional sedans in China, bundling a 55 km electric range with an 18.3 kWh LFP pack.

Fleet demand continues to skew toward plug-in hybrids, where urban low-emission rules reward zero-tailpipe operation. Stellantis is committed to expanding the Wrangler 4xe battery capacity to 21.5 kWh in 2026, thereby qualifying for California's 50-mile electric range rule. Mild hybrids, now standard on many North American pickups, strike a balance between fleet needs by offering 8-12% fuel savings at a fraction of the cost of full-hybrid models. However, HEVs will still account for the largest absolute volume in regions with limited charging infrastructure.

Passenger cars accounted for 77.31% of the hybrid vehicle market share in 2025; however, light commercial vehicles are the fastest-growing class, with a 13.24% CAGR through 2031. Ford rolled out its Transit Custom plug-in hybrid in Europe in early 2025. With a moderate electric range, the vehicle enables emission-free deliveries in city centers, while also offering a substantial total driving radius. In Germany, Mercedes-Benz noted that orders for its eSprinter hybrid significantly outpaced those for BEV variants, highlighting fleet preferences to sidestep charging downtimes. Meanwhile, medium and heavy trucks are now integrating mild-hybrid systems, capturing braking energy during intercity journeys without compromising payload capacity.

By the end of the decade, the hybrid vehicle market share for LCVs may dwindle, especially as low-emission zone regulations extend from Europe to major capitals in South America. While passenger-car hybrids, particularly compact crossovers, will continue to hold a foothold in the Asia Pacific, their growth is expected to slow as urban consumers shift towards more affordable BEVs. On the other hand, commercial vans value the fueling flexibility that hybrids offer, especially for their diverse urban-rural routes and varying daily mileage.

The Hybrid Vehicle Market Report is Segmented by Hybrid Vehicle Type (Mild-Hybrid and More), Vehicle Type (Passenger Cars, Light Commercial Vehicles, and Medium and Heavy Commercial Vehicles), Motor Type (PMSM, Induction AC Motor, and More), Battery Type (Nickel-Metal Hydride, Lithium-Iron Phosphate, and Others), and Geography. Market Forecasts are Provided in Value (USD) and Volume (Units).

Geography Analysis

Asia Pacific commanded 38.73% of the hybrid vehicle market share in 2025 and is projected to grow at a 13.21% CAGR through 2031. In recent years, China's sales of plug-in hybrids have surged, driven by supportive policies that incentivize production and sales, as well as competitive pricing strategies by leading manufacturers. Japan remains the world's leading exporter of conventional hybrids, serving key markets in Southeast Asia, the Middle East, and Latin America. Tax reductions on hybrid vehicles in India have narrowed the price gap with diesel vehicles, leading to a notable increase in hybrid vehicle registrations. In South Korea, national subsidies are providing substantial support to plug-in hybrid variants of popular models, boosting their adoption.

North America is witnessing a resurgence in hybrids as automakers address uncertainties surrounding battery-electric vehicles. Hybrid sales in the United States have grown significantly, with major players dominating the market. Canada has extended incentives for plug-in hybrids with longer electric ranges, sustaining demand for popular models.

In contrast, Europe has experienced a decline in plug-in hybrid registrations, mainly due to the withdrawal of subsidies in key markets and uncertainty surrounding future zero-emission credit policies. The United Kingdom has maintained a reduced grant for affordable plug-in vehicles, shifting consumer interest towards mainstream crossovers rather than premium hybrids.

While South America and the Middle East are still in the early stages of hybrid adoption, they are experiencing rapid growth. In Brazil, tariff reductions on hybrids have significantly boosted the market share of leading models. In the United Arab Emirates, incentives such as free parking and toll exemptions for plug-in hybrids with longer electric ranges have encouraged luxury brands to introduce models that comply with these requirements. Saudi Arabia, as part of its Vision 2030 sustainability goals, plans to procure a substantial number of hybrid vehicles for its government fleets in the coming years. Although current volumes remain relatively low, these initiatives are expected to drive future demand as charging infrastructure develops.

- Toyota Motor Corporation

- Honda Motor Co., Ltd.

- Nissan Motor Co., Ltd.

- Hyundai Motor Company

- Kia Corporation

- Ford Motor Company

- General Motors Company

- Stellantis N.V.

- BMW AG

- Mercedes-Benz Group AG

- Volkswagen AG

- BYD Co., Ltd.

- SAIC Motor Corporation

- Geely Automobile Holdings Ltd.

- Renault S.A.

- AB Volvo

- Subaru Corporation

- Mazda Motor Corporation

- Mitsubishi Motors Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Battery Cost-Parity Tipping Point For PHEVs By 2027

- 4.2.2 Stricter Global CAFE/GHG Norms & Zero-Emission Mandates

- 4.2.3 Soaring Fuel-Price Volatility Post-2024

- 4.2.4 OEM Multi-Pathway Carbon Strategies (ICE + BEV + HEV)

- 4.2.5 48-V Architecture Standardisation In Light Trucks

- 4.2.6 Grid-Independent Emergency-Power Use Case In Disaster-Prone Regions

- 4.3 Market Restraints

- 4.3.1 BEV Total-Cost-Of-Ownership Parity Achieved in Urban Fleets

- 4.3.2 Scarcity Of Sustainably Mined Nickel & Cobalt

- 4.3.3 Consumer Range-Anxiety Bias Shifting Straight To BEV

- 4.3.4 Looming End-Of-Life Recycling Liabilities for Ni-MH Packs

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Hybrid Vehicle Type

- 5.1.1 Mild-Hybrid

- 5.1.2 Hybrid Electric Vehicle (HEV)

- 5.1.3 Plug-in Hybrid (PHEV)

- 5.2 By Vehicle Type

- 5.2.1 Passenger Cars

- 5.2.2 Light Commercial Vehicles

- 5.2.3 Medium and Heavy Commercial Vehicles

- 5.3 By Motor Type

- 5.3.1 Permanent Magnet Synchronous AC Motor (PMSM)

- 5.3.2 Induction (Asynchronous) AC Motor

- 5.3.3 Switched Reluctance Motor (SRM)

- 5.3.4 Axial-Flux Motor

- 5.4 By Battery Type

- 5.4.1 Nickel-Metal Hydride

- 5.4.2 Lithium-iron Phosphate Battery

- 5.4.3 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Turkey

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Toyota Motor Corporation

- 6.4.2 Honda Motor Co., Ltd.

- 6.4.3 Nissan Motor Co., Ltd.

- 6.4.4 Hyundai Motor Company

- 6.4.5 Kia Corporation

- 6.4.6 Ford Motor Company

- 6.4.7 General Motors Company

- 6.4.8 Stellantis N.V.

- 6.4.9 BMW AG

- 6.4.10 Mercedes-Benz Group AG

- 6.4.11 Volkswagen AG

- 6.4.12 BYD Co., Ltd.

- 6.4.13 SAIC Motor Corporation

- 6.4.14 Geely Automobile Holdings Ltd.

- 6.4.15 Renault S.A.

- 6.4.16 AB Volvo

- 6.4.17 Subaru Corporation

- 6.4.18 Mazda Motor Corporation

- 6.4.19 Mitsubishi Motors Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment