PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043839

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043839

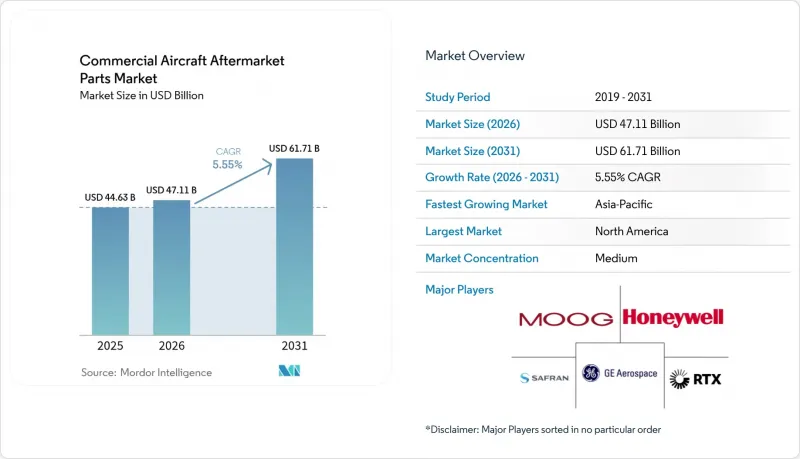

Commercial Aircraft Aftermarket Parts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The commercial aircraft aftermarket parts market size is expected to grow from USD 44.63 billion in 2025 to USD 47.11 billion in 2026 and is projected to reach USD 61.71 billion by 2031 at a 5.55% CAGR.

The growth path reflects persistent OEM delivery delays, aging narrowbody fleets staying in service longer, and higher shop-visit intensity on next-generation engines. Airlines are expanding the use of serviceable material sourcing as a hedge against long lead times and high new-part pricing. At the same time, digitization of parts planning and predictive maintenance supports improved uptime. Additive manufacturing reduces long-tail lead times for approved interior and secondary structure components, helping airlines and MROs balance inventory and service-level goals. Supply chain friction still adds cost and complexity, keeping the commercial aircraft aftermarket parts market focused on resiliency and life-cycle support outcomes rather than transactional spot buys.

Backlogs and certification safeguards shape near-term dynamics. A global order backlog that exceeds 17,000 aircraft extends the in-service life of legacy fleets and sustains parts demand despite slower new-build ramp rates. Airlines continue to absorb extra costs linked to supplier constraints, while regulators emphasize documentation and traceability for airworthiness-critical parts. OEMs strengthen digital channels and USM programs to stabilize availability, and leading MROs scale data-driven planning to keep aircraft on wing. This favors integrated ecosystems that combine physical parts, shop capacity, and connected analytics to protect operational reliability in the commercial aircraft aftermarket parts market.

Global Commercial Aircraft Aftermarket Parts Market Trends and Insights

Aging Global Single-Aisle Fleet Amid OEM Production Delays

Global order backlogs constrain replacement cycles, which pushes operators to extend legacy aircraft and sustain higher parts consumption for cycle-driven items. The backlog above 17,000 units indicates a multi-year queue that keeps assets on wing and drives recurring demand for rotables and consumables across the commercial aircraft aftermarket parts market. The longer service lives also reinforce the need for structural inspections and directed modifications mandated by airworthiness directives for high-cycle fleets. Regulators have issued updated guidance on continuing airworthiness and operator compliance, which supports stable demand for flight controls, landing gear, and systems parts subject to recurring checks. Airlines face elevated operating costs from broader supply chain friction, which slows material availability and increases planning buffers for heavy checks. The near-term effect is sustained aftermarket intensity for narrowbody fleets and targeted upgrades that bridge to delayed delivery slots in the commercial aircraft aftermarket parts market.

Unscheduled Shop Visits from Next-Gen Engine Durability Issues

Airlines and MROs continue to manage inspection campaigns and accelerated shop visits on select next-generation engines, which tighten module and LRU availability. The inspection and recovery plans on geared turbofan programs remain a major capacity variable through 2026, and investments in forging and critical rotating parts aim to address structural supply needs that flow into aftermarket repair pipelines. Engine OEMs and authorized shops coordinate module flow, but elongated turnaround times can cascade across fleets and inflate spare engine and rotable pool requirements. The result is greater emphasis on predictive planning, early material positioning, and alternative sourcing to protect dispatch reliability in the commercial aircraft aftermarket parts market. Regulatory oversight of repair data and airworthiness documentation continues to influence shops and operators performing major work on critical modules, shaping the balance between OEM-captive and independent capacity in the medium term. Airlines managing mixed engine portfolios balance short-term mitigation efforts with long-term maintenance strategies, including service bulletin implementation and shop load planning.

Global Technician Shortage Lengthening Turnaround Times

The maintenance labor pipeline remains a structural constraint, slowing throughput and raising costs across airframe, engine, and component shops. Global forecasts indicate that long-term demand for new aviation technicians significantly exceeds current training output, with the gap most pronounced in high-skill engine and avionics work scopes. MROs and airlines are addressing the issue by expanding training programs and forming partnerships with educational institutions. However, certification timelines and the need for experience continue to challenge capacity and turnaround times. The effect is longer intervals between heavy shop visits and more frequent use of exchange assets and leased modules, keeping aircraft available in the market. Regulators continue to oversee training and certification under established standards, which maintains safety and reliability but limits the rapid scaling of specialized skills. Over time, automation, digital work instructions, and AI-based diagnostics can help amplify productivity, but the near-term profile still points to tight labor conditions.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of Used-Serviceable-Material (USM) Ecosystems

- AI-Enabled Predictive Maintenance Improving Parts Planning

- OEM IP/Licensing Limits on Independent Part Repairs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Narrowbody aircraft held 59.87% of the commercial aircraft aftermarket parts market share in 2025, reflecting higher cycle counts that accelerate wear on wheels, brakes, environmental control systems, and line-replaceable avionics. As airlines prioritize high-frequency short-haul routes, utilization and turn times generate steady demand for consumables and rotables that can be exchanged on the line. Widebody platforms constitute a smaller installed base; however, they involve more complex work scopes and longer check durations. As a result, their projected growth from 2026 to 2031 is expected to surpass the fleet average. Regional jets remain essential in point-to-point networks and secondary airports, which sustains demand for hydraulics, pneumatics, and specialized avionics at regional MRO hubs. Regulatory directives for aging aircraft checks also favor narrowbody platforms due to higher cycles, which amplify inspection-driven material flows.

Widebody platforms are expected to grow at a CAGR of 6.45% through 2031, driven by airlines extending the service life of long-haul aircraft and retrofitting cabins and connectivity to meet passenger expectations. Airlines balance shop workloads between structural work and systems overhauls that must meet strict continuing airworthiness standards, which drives steady parts consumption for landing gear, flight controls, and cabin systems. Service bulletins and airworthiness directives reinforce inspection routines for high-cycle narrowbody fleets, increasing demand for certified replacement hardware and structural kits. Suppliers and MROs position rotable pools and exchange programs near operators with high aircraft utilization to reduce downtime. These patterns maintain strong parts velocity in areas where block hours and cycles are highest, which is crucial to the commercial aircraft aftermarket parts market.

Engine components accounted for 48.70% of the commercial aircraft aftermarket parts market size in 2025, highlighting the concentration of value in turbine hardware, hot-section materials, fuel systems, and control electronics. Next-generation engines introduce advanced alloys, coatings, and additively manufactured features that require OEM-authorized repairs and documented traceability. Shop capacity and module availability remain central variables for operators that must manage planned removals alongside unscheduled events. Avionics is the fastest-growing category, projected to grow at a 6.35% CAGR through 2031, driven by connectivity upgrades, IFE refresh cycles, and cockpit modernization that improve reliability and the passenger experience. Airframe components sustain steady demand as aging fleets undergo structural inspections and corrosion-prevention treatments under FAA and EASA programs.

As digital systems proliferate, software configuration control and cybersecurity updates accompany hardware swaps, which create recurring service lines for approved avionics providers. Technical standard orders and design approvals define supplier eligibility for safety-critical boxes, thereby limiting PMA penetration in classes such as TCAS, EGPWS, and SATCOM units. Cabin modernization remains a clear priority as airlines standardize on USB-C power, Wi-Fi, and slimline seating, resulting in multi-shipset programs that roll out across fleets over several years. Composites repair capability is expanding within MRO networks to support newer airframe platforms and control surfaces, and shops add tooling and training to execute approved repairs under Part 145. These conditions keep the engine and avionics at the center of growth, while the airframe and interiors maintain a steady, programmatic cadence in the commercial aircraft aftermarket parts market.

The Commercial Aircraft Aftermarket Parts Report is Segmented by Platform (Narrowbody, Widebody, and Regional Jets), Component Type (Engine, Airframe, Interior, and More), Parts Category (MRO Parts and Rotable Replacement Parts), End User (Airlines and Cargo Operators, and More), and Geography (North America, Europe, Asia-Pacific, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 36.54% of the commercial aircraft aftermarket parts market in 2025, supported by an extensive operator base, a strong OEM services presence, and a dense network of FAA-approved MRO facilities. Operators in the region maintain high utilization and adopt digital and predictive processes early, thereby strengthening planning and sparing allocation across fleets. Compliance with FAA airworthiness directives drives steady demand for parts for systems, structures, and engines on high-cycle narrow-body aircraft. OEM distribution platforms, such as Boeing's and Airbus's integrated channels, improve transactional efficiency and documentation flow, supporting audit and reliability needs.

Asia Pacific is projected to grow at a 7.10% CAGR through 2031, the fastest among regions, as carriers add capacity and restore international connectivity. China's fleet growth trajectory toward 9,570 aircraft by the next two decades underpins a large future services base and creates long-run demand for engines, components, and cabin upgrades. India's connectivity programs add new city pairs and stimulate narrow-body utilization, increasing the need for rotables and consumables to support higher daily cycles. Regional MRO capability continues to expand, with established hubs and new entrants receiving approvals for line, airframe, engine, and component maintenance. Predictive platforms and OEM service packages are seeing broader adoption as operators seek to reduce unplanned events and improve reliability.

Europe remains a mature, high-value region with robust MRO networks and strict EASA oversight that keeps inspection and documentation standards at the forefront of planning. Flag carriers and low-cost operators extend the economic life of existing fleets through cabin modernization and connectivity retrofits to manage delivery shortfalls and match demand. The Middle East continues to scale wide-body maintenance and component services around large hub carriers, while Africa and South America strengthen facilities and approvals to nearshore work from North American and European operators. Tariff and logistics considerations encourage nearshoring of parts flows to Caribbean and Central American sites that can offer cost and proximity advantages for US operators. Public programs that fund advanced materials and process technologies also contribute to regional supply resilience and talent development for future parts demand.

- Aventure International Aviation Services

- Honeywell International Inc.

- RTX Corporation

- Parker-Hannifin Corporation

- General Electric Company

- Moog Inc.

- GKN Aerospace Services Limited

- A J Walter Aviation Limited

- Bombardier Inc.

- The Boeing Company

- Safran SA

- Rolls-Royce Holdings plc

- Lufthansa Technik AG

- Singapore Technologies Engineering Ltd.

- AAR Corp.

- StandardAero, Inc.

- Eaton Corporation plc

- Kellstrom Aerospace

- VAS Aero Services, LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aging global single-aisle fleet amid OEM production delays

- 4.2.2 Unscheduled shop visits from next-gen engine durability issues

- 4.2.3 Rapid expansion of used-serviceable-material (USM) ecosystems

- 4.2.4 AI-enabled predictive maintenance improving parts planning

- 4.2.5 On-demand 3D printing shortening long-tail parts lead-times

- 4.2.6 Tariff-driven near-shoring of parts supply chains

- 4.3 Market Restraints

- 4.3.1 Global technician shortage lengthening turnaround times

- 4.3.2 OEM IP/licensing limits on independent part repairs

- 4.3.3 Counterfeit-part risk tightening certification compliance

- 4.3.4 Raw-material cost and forging/casting bottlenecks

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Narrowbody

- 5.1.2 Widebody

- 5.1.3 Regional Jets

- 5.2 By Component Type

- 5.2.1 Engine

- 5.2.2 Airframe

- 5.2.3 Interior

- 5.2.4 Avionics and Others

- 5.3 By Parts Category

- 5.3.1 MRO Parts

- 5.3.2 Rotable Replacement Parts

- 5.4 By End User

- 5.4.1 Airlines and Cargo Operators

- 5.4.2 Independent MRO Providers

- 5.4.3 Aircraft Leasing Companies

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Israel

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 United Arab Emirates

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Aventure International Aviation Services

- 6.4.2 Honeywell International Inc.

- 6.4.3 RTX Corporation

- 6.4.4 Parker-Hannifin Corporation

- 6.4.5 General Electric Company

- 6.4.6 Moog Inc.

- 6.4.7 GKN Aerospace Services Limited

- 6.4.8 A J Walter Aviation Limited

- 6.4.9 Bombardier Inc.

- 6.4.10 The Boeing Company

- 6.4.11 Safran SA

- 6.4.12 Rolls-Royce Holdings plc

- 6.4.13 Lufthansa Technik AG

- 6.4.14 Singapore Technologies Engineering Ltd.

- 6.4.15 AAR Corp.

- 6.4.16 StandardAero, Inc.

- 6.4.17 Eaton Corporation plc

- 6.4.18 Kellstrom Aerospace

- 6.4.19 VAS Aero Services, LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment