PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043841

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043841

Europe Retail Analytics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

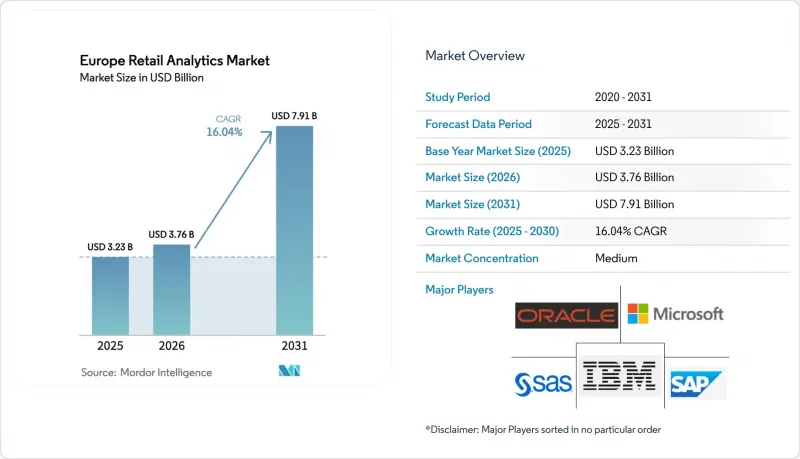

The Europe retail analytics market size is projected to be USD 3.23 billion in 2025, USD 3.76 billion in 2026, and reach USD 7.91 billion by 2031, growing at a CAGR of 16.04% from 2026 to 2031.

Surging investment in first-party data platforms, inflation-era margin pressure, and unified commerce mandates are accelerating platform renewals across the region. Cloud-native services that blend elastic compute with advanced AI are increasingly preferred as merchants deploy real-time pricing and computer-vision workloads. Growing reliance on privacy-enhancing technologies is steering spending toward vendors that embed consent management and explainability features by design. Competitive intensity, meanwhile, is rising as ERP incumbents embed analytics into core workflows and data-platform specialists differentiate on open architecture and EU data-residency options.

Europe Retail Analytics Market Trends and Insights

Data-Driven Personalization Lifts In-Store Conversion

European chains are embedding predictive models into kiosks, mobile apps, and point-of-sale terminals to surface individualized offers that lift basket size and drive repeat visits. Adobe's 2024 benchmarking found that unified customer-data platforms improved fashion and grocery conversion rates by 20%-30%. GDPR's value-exchange ethos makes such personalization a competitive necessity rather than a differentiator. KPMG reported that 68% of retailers plan to boost AI-led personalization budgets by 2026. Agentic commerce pilots, where AI agents negotiate bundles and payments on a shopper's behalf, will further intensify real-time profile requirements. As data-sharing consent becomes harder to secure, merchants must showcase tangible benefits to retain first-party relationships.

AI-Powered Pricing Engines Optimize Margin in Inflationary Europe

Inflation volatility pushed grocers and fashion retailers to replace weekly price cycles with algorithms that recalibrate shelf prices several times per day. McKinsey's 2025 grocery study documented 1-2 percentage-point gross-margin lifts among adopters during the 2024 cost-of-living squeeze. Modern engines ingest competitor feeds, weather updates, and local events, then optimize markdown calendars while guarding brand perception. BCG forecasts EUR 10 billion-EUR 15 billion (USD 11.3 billion-USD 16.9 billion) in incremental margin by 2027, provided transparency safeguards assuage regulator and consumer concerns. Vendors now bundle explainability dashboards to comply with EU AI-Act disclosure clauses.

Data-Privacy Tightening Under GDPR and ePrivacy Regulation

Proposed ePrivacy rules broaden explicit-consent demands for cookies, device fingerprinting, and location analytics, curtailing third-party identifiers that feed personalization and attribution models. The European Commission recorded a 62% refusal rate for tracking consent in 2025, shrinking campaign reach. Article 22 of GDPR introduces human-in-the-loop mandates for automated decision-making, slowing dynamic pricing rollouts. Retailers are piloting differential privacy, federated learning, and synthetic datasets, but lack of mature tooling raises cost and complexity.

Other drivers and restraints analyzed in the detailed report include:

- Unified Commerce Mandates Single View of Customer

- Proliferation of Edge Analytics for Real-Time Shelf Monitoring

- Shortage of Retail Data-Science Talent Pool

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud captured 63.13% of Europe retail analytics market share in 2025, reflecting merchants' shift toward scalable infrastructure for real-time pricing and vision workloads. Public-cloud migration also unlocks managed AI, disaster recovery, and multi-region replication, reducing total cost of ownership for mid-cycle hardware refreshes. On-premise estates persist among grocers with legacy ERP and stringent data-residency contracts, notably in Germany and France. Hybrid architectures are emerging as a compliance hedge, allowing sensitive transactions to stay on-premise while heavy analytics batches run in the cloud. Microsoft's 2025 hybrid SKU syncs point-of-sale data to Azure Synapse without full migration. Snowflake's 2024 residency controls let merchants query distributed warehouses through one interface, sidestepping Article 44 cross-border hurdles.

Greater elasticity means retailers can spin up GPU clusters during peak pricing or vision workloads, then shut them down, slashing idle costs. Vendors incentivize the transition to SAP and Oracle by discounting licenses for multi-year cloud terms, effectively funding migration projects. The Europe retail analytics market size attributable to cloud is thus forecast to widen its lead through 2031, while hybrid gains incremental traction among regulated sectors. As retailers embed edge-compute nodes inside stores, hybrid topologies will likely dominate workloads requiring both in-store latency and cloud-scale training cycles.

Marketing and customer insight suites held 27.54% revenue in 2025, underscoring continued appetite for personalization and retail-media measurement. Yet supply-chain and fulfillment tools are expanding fastest at an 18.02% CAGR, driven by autonomous replenishment and last-mile optimization engines that release working capital. Zalando cut overstock by 15% and achieved 98% in-stock accuracy after rolling out AI-based demand sensing. Accenture recorded 10%-20% safety-stock reductions among adopters, freeing cash for digital reinvestment. The Europe retail analytics market size attached to supply-chain modules is expected to outstrip legacy assortment-planning suites through 2031. Loss-prevention solutions fusing computer vision with shrinkage analytics are gaining ground as camera prices drop and ESG frameworks demand food-waste reporting.

Adoption trajectories differ by retailer maturity. Vertically integrated fashion houses focus on allocation and markdown optimization to preserve brand equity, while grocery chains prioritize demand forecasting to curb perishables. Category-management suites remain sticky because decades-old business rules are hard-wired, capping their growth relative to newer AI-first products. Meanwhile, financial-performance dashboards that blend P&L with operational metrics are consolidating multiple legacy BI stacks into single views, streamlining decision-maker workflows.

The Europe Retail Analytics Market Report is Segmented by Mode of Deployment (On-Premise, Cloud, and Hybrid), Module Type (Strategy and Planning, Marketing and Customer Insights, and More), Business Size (Small and Medium Enterprises, and Large Enterprises), Retail Format (Brick-And-Mortar, E-Commerce, and Omnichannel Retail), and Country (Germany, Italy, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- SAP SE

- Oracle Corporation

- IBM Corporation

- SAS Institute Inc.

- Microsoft Corporation

- Fractal Analytics

- Tableau Software LLC

- MicroStrategy Incorporated

- Sensormatic Solutions

- Alteryx Inc.

- RetailNext Inc.

- Blue Yonder GmbH

- NielsenIQ

- ThoughtSpot Inc.

- Sisense Ltd.

- Domo Inc.

- Looker Data Sciences (Google)

- Snowflake Inc.

- Databricks Inc.

- C3.ai Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Data-Driven Personalization Lifts In-Store Conversion

- 4.2.2 AI-Powered Pricing Engines Optimise Margin in Inflationary Europe

- 4.2.3 Proliferation of Edge Analytics for Real-Time Shelf Monitoring

- 4.2.4 Unified Commerce Mandates Single View of Customer

- 4.2.5 Retail Media Network Analytics Unlocking Incremental Revenue Streams

- 4.2.6 ESG-Aligned Shrinkage Analytics Integrating Computer Vision

- 4.3 Market Restraints

- 4.3.1 Shortage of Retail Data-Science Talent Pool

- 4.3.2 Data-Privacy Tightening Under GDPR and ePrivacy Regulation

- 4.3.3 Legacy POS Fragmentation Impedes Data Integration

- 4.3.4 Capital-Expenditure Freeze Among SME Retailers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Mode of Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Module Type

- 5.2.1 Strategy and Planning

- 5.2.2 Marketing and Customer Insights

- 5.2.3 Financial Management

- 5.2.4 Store Operations and Loss Prevention

- 5.2.5 Merchandising and Category Optimisation

- 5.2.6 Supply-Chain and Fulfilment

- 5.3 By Business Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By Retail Format

- 5.4.1 Brick-and-Mortar

- 5.4.2 E-Commerce

- 5.4.3 Omnichannel Retail

- 5.5 By Country

- 5.5.1 United Kingdom

- 5.5.2 Germany

- 5.5.3 France

- 5.5.4 Italy

- 5.5.5 Spain

- 5.5.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Oracle Corporation

- 6.4.3 IBM Corporation

- 6.4.4 SAS Institute Inc.

- 6.4.5 Microsoft Corporation

- 6.4.6 Fractal Analytics

- 6.4.7 Tableau Software LLC

- 6.4.8 MicroStrategy Incorporated

- 6.4.9 Sensormatic Solutions

- 6.4.10 Alteryx Inc.

- 6.4.11 RetailNext Inc.

- 6.4.12 Blue Yonder GmbH

- 6.4.13 NielsenIQ

- 6.4.14 ThoughtSpot Inc.

- 6.4.15 Sisense Ltd.

- 6.4.16 Domo Inc.

- 6.4.17 Looker Data Sciences (Google)

- 6.4.18 Snowflake Inc.

- 6.4.19 Databricks Inc.

- 6.4.20 C3.ai Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment