PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043844

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043844

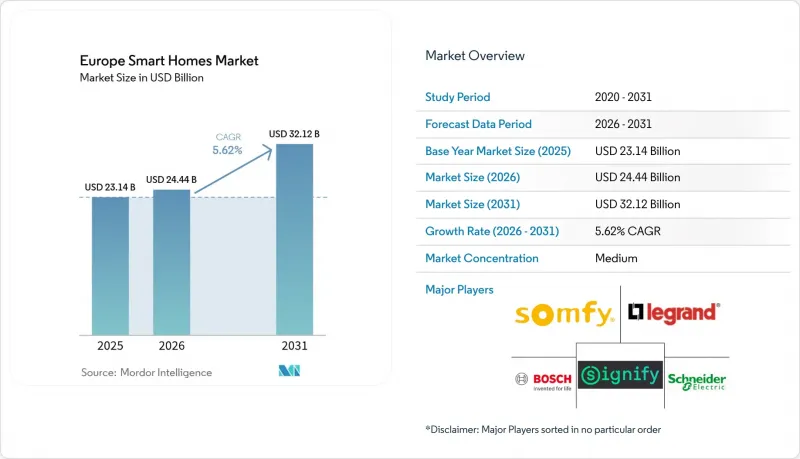

Europe Smart Homes - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe smart homes market size is projected to expand from USD 23.14 billion in 2025 and USD 24.44 billion in 2026 to USD 32.12 billion by 2031, registering a CAGR of 5.62% between 2026-2031.

Mandated zero-emission construction rules, subsidy-linked heat-pump rollouts, and dynamic power tariffs are repositioning connected devices as regulatory necessities rather than discretionary gadgets. Grid operators across the Nordics and the Netherlands now expose tariff APIs that reward automated load-shifting, accelerating uptake of demand-responsive thermostats and smart chargers. Meanwhile, the halogen-lamp phase-out and rising burglary claim severities are steering households toward networked lighting and security bundles. Vendor rivalry remains intense as building-automation incumbents defend installer channels while direct-to-consumer specialists capture do-it-yourself upgrades. Compliance-anchored demand, a maturing Matter standard, and falling component prices collectively underpin the Europe smart homes market's medium-term momentum.

Europe Smart Homes Market Trends and Insights

EU-wide Energy-Performance Mandates For Residential Buildings

The revised Energy Performance of Buildings Directive compels every member state to transpose zero-emission standards by 2026, forcing developers and homeowners to embed automation for heating, lighting, and ventilation into project scopes. Germany's draft law requires smart thermostats on all new heating systems after January 2026, while France extends mandatory lighting controls to large multifamily blocks, effectively enlarging the addressable Europe smart homes market. Vendors with end-to-end platforms benefit because compliance assessments now score "automation readiness", nudging buyers toward integrated ecosystems rather than single-purpose gadgets.

Surge In Security And Lighting Upgrades Among Existing Homeowners

Insurers across Germany, France, and the United Kingdom offer 5-15% premium rebates for certified smart-security packages, turning doorbells and smart locks into quick-return investments. Concurrently, the EU halogen ban is accelerating LED adoption, giving smart bulbs a natural entry point. Signify reported that one-third of its 2025 luminaires included connectivity modules, up from just over one-fifth in 2023. Together these forces amplify retrofit demand and sustain the Europe smart homes market beyond early adopters.

High Upfront Hardware And Installation Costs

Comprehensive smart-home packages average EUR 3,500-8,000 (USD 3,920-8,960) and professional labor adds EUR 1,200-2,500 (USD 1,344-2,800). Payback stretches beyond nine years in some Southern markets where tariffs are lower, deterring middle-income households. Modular starter kits below EUR 500 (USD 560) soften entry barriers but often lack the interoperability necessary for whole-home automation, tempering immediate growth in the broader Europe smart homes market.

Other drivers and restraints analyzed in the detailed report include:

- Rising Consumer Preference For Integrated, Voice-Controlled Ecosystems

- Smart-Appliance Subsidies Under National Electrification Programs

- Persistent Data-Privacy And Cyber-Security Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Security and access-control delivered USD 6.86 billion of 2025 revenue, equal to 29.63% of the Europe smart homes market share, yet HVAC and climate-control leads growth with a 6.73% CAGR. Subsidy-eligible heat pumps that must couple with smart thermostats position HVAC as the centerpiece of compliance spending. Retrofit-friendly wireless thermostats, predictive boiler controllers, and sensor-rich air handlers now outsell traditional single-zone units. Energy-management devices ride similar tailwinds as dynamic tariffs spread, while lighting controls surge on the back of the halogen withdrawal timetable and Matter certification. Smart appliances and entertainment linger behind because replacement cycles are longer and perceived incremental utility remains thin.

The competitive map is shifting accordingly. Schneider Electric and Bosch integrate HVAC, energy, and security under single dashboards, capturing bundle premiums. Conversely, camera specialists face margin pressure as generic Wi-Fi silicon lowers entry hurdles. Vendors that weld HVAC, lighting, and metering into coherent packages stand to win the next wave of Europe smart homes market demand.

Retrofit projects tallied 63.41% of 2025 spending because more than 220 million European dwellings predate 1990. Wireless Thread and Zigbee kits reduce drilling requirements in heritage structures and cut labor costs by nearly one-third. Nevertheless, zero-emission directives and smart-ready building codes propel new-build smart systems at a brisk 5.94% CAGR. Germany and the Netherlands, buoyed by healthy construction pipelines, already see new-build share crest 40%.

Professional wholesalers stock differentiated lines for the two formats. Legrand and ABB aim retrofit ranges at electricians lacking networking expertise, while Bosch packages premounted rails for developers. Through 2031 retrofit will remain the volume anchor of the Europe smart homes market, yet the revenue gap will narrow as smart-ready construction becomes the continental norm.

The Europe Smart Homes Market is Segmented by Product Type (Lighting Controls, and More), Installation Type (New-Build Integrated Systems and Retrofit/Existing-Home Upgrades), Distribution Channel (Professional/Installer Channel and Retail and E-Commerce), Communication Technology (Wi-Fi, Zigbee, and More), Application (Security and Safety, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Signify N.V.

- Robert Bosch GmbH (Bosch Smart Home)

- Schneider Electric SE

- Legrand SA

- Somfy SA

- ABB Ltd.

- Lutron Electronics Co., Inc.

- TP-Link Deutschland GmbH

- Netatmo SAS

- Eve Systems GmbH

- tado GmbH

- Nuki Home Solutions GmbH

- Fibaro Group S.A.

- Gira Giersiepen GmbH and Co. KG

- Hager Group

- Devolo GmbH

- Ekinex S.p.A.

- Centrica Hive Limited

- AXIS Communications AB

- Johnson Controls International plc

- Control4 Corporation (Wirepath Home Systems, LLC)

- Ring (Amazon subsidiary)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU-wide Energy-Performance Mandates for Residential Buildings

- 4.2.2 Surge in Security and Lighting Upgrades Among Existing Homeowners

- 4.2.3 Rising Consumer Preference for Integrated, Voice-Controlled Ecosystems

- 4.2.4 Smart-Appliance Subsidies Under National Electrification Programs

- 4.2.5 Growth of Retrofit-Ready Modular Kits for Heritage Housing

- 4.2.6 Dynamic-Tariff Driven Demand for Home Energy-Management Platforms

- 4.3 Market Restraints

- 4.3.1 High Upfront Hardware and Installation Costs

- 4.3.2 Persistent Data-Privacy and Cyber-Security Concerns

- 4.3.3 Fragmented Protocol Standards Hinder Interoperability

- 4.3.4 Shortage of Certified Smart-Home Installers

- 4.4 Industry Value Chain Analysis

- 4.5 Ecosystem Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.7.1 Major Communication and Connectivity Technologies

- 4.7.2 Key Industry Standards and Policies

- 4.7.3 Product Innovations and Cyber-Security Emphasis

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

- 4.9 Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Lighting Controls

- 5.1.2 Energy-Management Devices

- 5.1.3 Security and Access-Control

- 5.1.4 Smart Entertainment

- 5.1.5 Smart Appliances

- 5.1.6 HVAC and Climate-Control

- 5.2 By Installation Type

- 5.2.1 New-Build Integrated Systems

- 5.2.2 Retrofit/Existing-Home Upgrades

- 5.3 By Distribution Channel

- 5.3.1 Professional/Installer Channel

- 5.3.2 Retail and E-commerce (DIY)

- 5.4 By Communication Technology

- 5.4.1 Wi-Fi

- 5.4.2 Zigbee

- 5.4.3 Z-Wave

- 5.4.4 Bluetooth and BLE

- 5.4.5 Thread

- 5.4.6 Other Communication Technologies (EnOcean, Matter, RF, etc.)

- 5.5 By Application

- 5.5.1 Security and Safety

- 5.5.2 Energy and Utilities Management

- 5.5.3 Comfort and Lighting

- 5.5.4 Entertainment and Lifestyle

- 5.5.5 Health and Assisted Living

- 5.6 By Country

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Netherlands

- 5.6.7 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Signify N.V.

- 6.4.2 Robert Bosch GmbH (Bosch Smart Home)

- 6.4.3 Schneider Electric SE

- 6.4.4 Legrand SA

- 6.4.5 Somfy SA

- 6.4.6 ABB Ltd.

- 6.4.7 Lutron Electronics Co., Inc.

- 6.4.8 TP-Link Deutschland GmbH

- 6.4.9 Netatmo SAS

- 6.4.10 Eve Systems GmbH

- 6.4.11 tado GmbH

- 6.4.12 Nuki Home Solutions GmbH

- 6.4.13 Fibaro Group S.A.

- 6.4.14 Gira Giersiepen GmbH and Co. KG

- 6.4.15 Hager Group

- 6.4.16 Devolo GmbH

- 6.4.17 Ekinex S.p.A.

- 6.4.18 Centrica Hive Limited

- 6.4.19 AXIS Communications AB

- 6.4.20 Johnson Controls International plc

- 6.4.21 Control4 Corporation (Wirepath Home Systems, LLC)

- 6.4.22 Ring (Amazon subsidiary)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment