PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043848

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043848

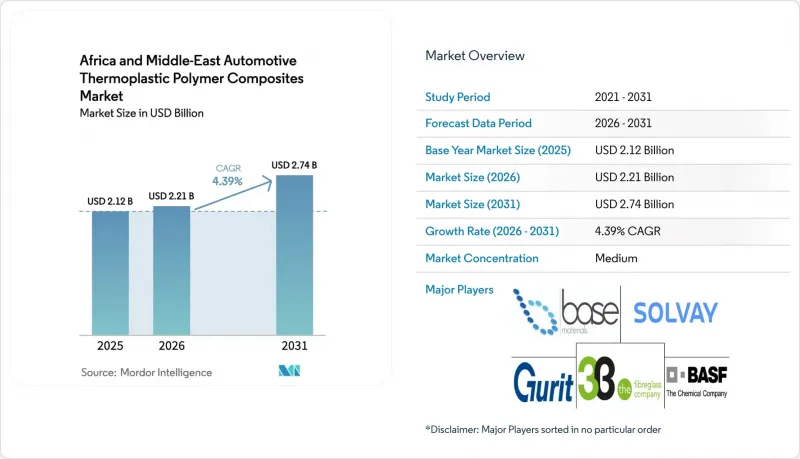

Africa And Middle-East Automotive Thermoplastic Polymer Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Africa And Middle-East Automotive Thermoplastic Polymer Composites Market size is expected to grow from USD 2.12 billion in 2025 to USD 2.21 billion in 2026 and is forecast to reach USD 2.74 billion by 2031 at 4.39% CAGR over 2026-2031. Light-weighting mandates, localization incentives in Saudi Arabia and the United Arab Emirates, and the growing transition to electric vehicles are driving increased demand for glass- and carbon-fiber-reinforced polypropylene and polyamide components. Injection molding continues to dominate in producing interior trim and small exterior parts due to its high-volume capabilities. However, compression molding is expanding rapidly, supported by the adoption of continuous-fiber organo-sheets, which reduce cycle times to under 90 seconds. Regional carbon-pricing pilots, though currently limited, are providing a clear price signal that benefits OEMs capable of demonstrating lower life-cycle emissions. Consequently, supply chain strategies are shifting toward in-region compounding and multi-year fiber offtake agreements, which help mitigate raw material price volatility and reduce lead times.

Africa And Middle-East Automotive Thermoplastic Polymer Composites Market Trends and Insights

Stringent Regional CO2/CAFE-Like Auto-Emission Policies

Fleet-average fuel-economy targets planned for Saudi Arabia in 2025 and Egypt's implementation of Euro 5 norms are driving the replacement of steel with long-glass-fiber polyamide in components such as door modules, front-end carriers, and instrument panels. This transition achieves 30%-40% mass savings while meeting crash-performance standards. Additionally, UAE programs aiming for 50% electric or hybrid vehicle sales by 2030 are reinforcing this trend, as battery packs increase vehicle curb weight, heightening the demand for lightweight materials. OEM bid documents increasingly reference ISO 14040 life-cycle assessments, requiring suppliers to measure carbon footprints from polymerization to end-of-life recycling.

OEM Localization Incentives in Saudi Arabia and UAE Free Zones

Ten-year tax holidays, duty-free equipment imports, and subsidized land in King Abdullah Economic City and Abu Dhabi's KIZAD are motivating tier-1 converters to establish local compounding and molding facilities. For instance, Lucid Motors shifted the production of long-glass-fiber polypropylene interior panels from U.S. plants to a Saudi-based source, reducing logistics costs by 18% and shortening lead times from eight weeks to three. Similar agreements with Chinese material producers are anchoring polyamide-66 and polyphenylene-sulfide extrusion capacities for EV powertrain components.

Import-Driven Raw-Material Price Volatility (Glass and Carbon Fiber)

Glass and carbon fiber costs experienced fluctuations of 15%-25% during 2024-2025 due to disruptions in Red Sea shipping and increased energy costs at European furnaces. Saudi and UAE OEMs managed to partially mitigate these fluctuations through multi-year contracts. However, smaller converters in Egypt and Kenya faced challenges, as they had to either absorb the cost increases or risk losing fixed-price component agreements. Additionally, currency depreciation, such as 18% for the Egyptian pound in 2024 and 12% for the South African rand in 2025, further increased local-currency fiber prices, putting pressure on converter margins.

Other drivers and restraints analyzed in the detailed report include:

- Rapid EV Component Sourcing Shift Toward Recyclable PP/PA Composites

- GCC Carbon-Pricing Pilots Boosting Lightweight Demand

- Deficit of Skilled Composite Technicians across North and Sub-Saharan Africa

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Compression molding is anticipated to grow at a 4.78% CAGR through 2031. Injection molding maintained 36.42% of 2025 output due to its cost advantages for high-volume applications such as interior trim, under-hood covers, and small exterior skins. Hand lay-up continues to be used for boutique luxury interiors, but its scalability is restricted by inconsistent fiber distribution and high labor costs. Resin transfer molding is gaining acceptance for battery enclosures, with fast-cure polyamide 6 reducing cycle times to 4-6 minutes. Vacuum infusion remains primarily limited to prototype production.

Organo-sheet technology serves as a key enabler for compression molding. Pre-consolidated continuous fibers embedded in a thermoplastic matrix enable cycle times of less than 90 seconds with consistent quality. Ceer's first electric vehicle model incorporates compression-molded polyamide-6 underbody shields, achieving a 35% weight reduction and a 20% decrease in total cost of ownership over the vehicle's lifecycle. UAE regulations requiring ISO 527 tensile and ISO 14125 flexural data favor automated processes that ensure quality metrics, accelerating the transition away from manual lay-ups.

The Africa and Middle-East Automotive Thermoplastic Polymer Composites Market Report is Segmented by Production Type (Injection Molding, Hand Lay-Up, and More), Application Type (Interior, Exterior, Structural Assembly, Powertrain Components, and More), and Geography (South Africa, Egypt, United Arab Emirates, Saudi Arabia, and Rest of Middle-East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- 3B - the fibreglass company

- Base Materials Ltd.

- BASF

- Chongqing Polycomp International Corporation (CPIC)

- Solvay

- BorgWarner

- Far-UK

- General Motors Company

- Gurit Holding AG

- Hexcel Corporation

- Johns Manville

- LyondellBasell

- Nippon Electric Glass

- Praana Group

- Saint-Gobain Vetrotex

- SGL Carbon

- Taishan Fiberglass

- Teijin Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Stringent regional CO2/CAFE-like auto-emission policies

- 4.2.2 OEM localisation incentives in Saudi Arabia and UAE free-zones

- 4.2.3 Rapid EV component sourcing shift towards recyclable PP/PA composites

- 4.2.4 GCC carbon-pricing pilots boosting lightweight material demand

- 4.2.5 3D-printed long-fibre thermoplastic tooling lowering cap-ex

- 4.3 Market Restraints

- 4.3.1 Import-driven raw-material price volatility (glass and carbon fibre)

- 4.3.2 Deficit of skilled composite technicians across North and Sub-Saharan Africa

- 4.3.3 Fragmented recycling streams for mixed thermoplastic laminates

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Consumers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Production Type

- 5.1.1 Injection Molding

- 5.1.2 Hand Lay-Up

- 5.1.3 Resin Transfer Molding (RTM)

- 5.1.4 Vacuum Infusion Processing

- 5.1.5 Compression Molding

- 5.2 By Application Type

- 5.2.1 Interior

- 5.2.2 Exterior

- 5.2.3 Structural Assembly

- 5.2.4 Powertrain Components

- 5.2.5 Other Application Types

- 5.3 By Geography

- 5.3.1 South Africa

- 5.3.2 Egypt

- 5.3.3 United Arab Emirates

- 5.3.4 Saudi Arabia

- 5.3.5 Rest of Middle-East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3B - the fibreglass company

- 6.4.2 Base Materials Ltd.

- 6.4.3 BASF

- 6.4.4 Chongqing Polycomp International Corporation (CPIC)

- 6.4.5 Solvay

- 6.4.6 BorgWarner

- 6.4.7 Far-UK

- 6.4.8 General Motors Company

- 6.4.9 Gurit Holding AG

- 6.4.10 Hexcel Corporation

- 6.4.11 Johns Manville

- 6.4.12 LyondellBasell

- 6.4.13 Nippon Electric Glass

- 6.4.14 Praana Group

- 6.4.15 Saint-Gobain Vetrotex

- 6.4.16 SGL Carbon

- 6.4.17 Taishan Fiberglass

- 6.4.18 Teijin Limited

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment