PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043849

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043849

Cybersecurity Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

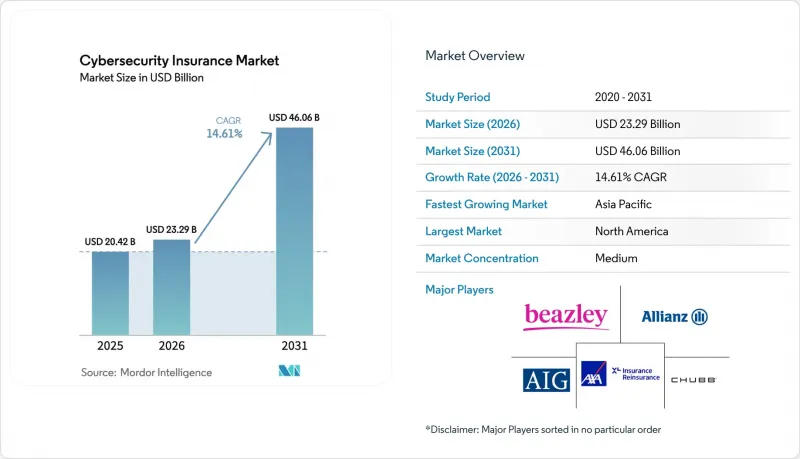

The cybersecurity insurance market size is projected to be USD 20.42 billion in 2025, USD 23.29 billion in 2026, and reach USD 46.06 billion by 2031, growing at a CAGR of 14.61% from 2026 to 2031.

Premium rate moderation, wider regulatory coverage requirements, and growing board-level demand for quantified cyber-risk transfer are reinforcing demand momentum. Capacity is expanding, yet underwriting discipline remains tight as carriers reserve capital for sectors with concentrated systemic exposure. The shift from indemnity-only offerings toward integrated InsurSec models is compressing loss ratios because embedded controls lower claim severity. Growth prospects also benefit from parametric innovation that shortens claims cycles and attracts under-served small and medium enterprises, particularly in Asia-Pacific where new data-protection statutes are raising minimum coverage limits.

Global Cybersecurity Insurance Market Trends and Insights

Cloud-First Digitalization Upsizes Cyber-Loss Exposure

Rapid migration to multi-tenant cloud platforms has widened breach pathways through misconfigured storage, compromised service accounts, and lateral movement between tenants. The February 2024 ransomware strike on Change Healthcare, which generated USD 2.3 billion in direct and business-interruption costs, showed how a single service disruption can ripple through critical U.S. healthcare workflows. Insurers now demand multi-factor authentication, privileged-access controls, and immutable backups before binding coverage, and many apply sub-limits to cloud-service-provider outages. Demand for first-party business-interruption extensions is therefore rising because a cloud outage can paralyze geographically dispersed operations within hours. These technical prerequisites are tightening selection standards even as headline capacity grows, thereby preserving profitability while sustaining policy uptake among cloud-heavy enterprises.

Escalating Regulatory Mandates (GDPR, NY DFS, DORA, SEC Rules)

Harmonized resilience laws are transforming cybersecurity insurance from discretionary spending into a compliance instrument. The Digital Operational Resilience Act, effective January 2025, obliges more than 20,000 EU financial entities to test cyber-resilience annually and disclose incidents within strict timelines. New York's 2023 DFS amendment compels large financial firms to certify cybersecurity programs and imposes penalties of up to USD 1,000 per day for non-compliance. Parallel disclosure rules from the U.S. SEC require listed companies to announce material incidents within four business days and describe board oversight, embedding cyber-risk reporting in fiduciary duty. Together these statutes elevate baseline coverage limits, particularly for third-party fines and legal defense, thereby lifting overall premium volume.

Actuarial Data Scarcity and Modeling Uncertainty

Attack vectors mutate faster than loss data accumulates, undermining classical actuarial techniques. The 2021 Kaseya ransomware campaign spread through managed-service providers and harmed more than 1,500 downstream clients, showing how a zero-day exploit can distort correlation assumptions overnight. Carriers react by capping per-event aggregates, excluding incidents tied to unpatched vulnerabilities older than 30 days, and charging steep additional premiums for undefended remote-desktop ports. Fragmented breach-reporting laws outside Europe and North America suppress accurate frequency statistics, inflating pricing buffers against modeling error and delaying expansion in jurisdictions lacking transparent notification regimes.

Other drivers and restraints analyzed in the detailed report include:

- Board-Level Focus on Quantifying Cyber Risk

- SME-Focused Low-Cost Parametric Covers Emerging

- High Premium and Retention Levels Deter SMEs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Third-party liability coverage is projected to outstrip first-party demand at a 15.32% CAGR through 2031 as privacy fines and class actions proliferate under stringent statutes such as Illinois's Biometric Information Privacy Act. First-party protection, which commanded 42.66% of cybersecurity insurance market share in 2025, remains foundational for funding incident response, business-interruption, and ransom outlays but is maturing in North America and Europe where attachment points keep rising. Growing reliance on operational technology in healthcare and manufacturing multiplies direct-loss scenarios, so insurers are adding sub-limits for cloud-outage or equipment-recalibration costs, sustaining incremental demand even as pricing moderates.

Litigation risk from regulatory fines under the EU GDPR, which allows sanctions up to 4% of global turnover, is propelling uptake of defense and settlement towers, especially among international platforms that process data across member states. Hybrid products that consolidate both loss types under unified limits help multinationals avoid allocation disputes when a ransom payment morphs into class-action liability. This hybridization stabilizes combined ratios by ensuring balanced premium inflows across frequency-prone first-party and severity-heavy liability claims, keeping the cybersecurity insurance market attractive for reinsurers.

Stand-alone contracts captured 53.17% of global premiums in 2025 and are accelerating at 15.72% as risk managers decouple cyber perils from property and casualty covers to secure clearer wording. The NotPetya disputes that followed Zurich's denial of Mondelez's USD 100 million property claim highlighted ambiguity in "all-risk" forms and spurred demand for bespoke language that overrides war exclusions. Dedicated policies now integrate granular warranties such as mandatory multifactor authentication and 30-day patching windows, which general-liability endorsements rarely enforce.

Packaged extensions retain relevance for micro-enterprises where price sensitivity trumps coverage breadth, yet many carriers have removed ransomware, social engineering, and business-interruption protections from these endorsements. Continuous-scanning offerings like Coalition's active-insurance model reinforce the stand-alone preference by giving insureds real-time visibility into external attack surfaces and allowing underwriters to amend terms mid-policy when high-risk vulnerabilities appear. This dynamic underpins sustainable growth in the cybersecurity insurance market size for stand-alone products.

The Cybersecurity Insurance Market Report is Segmented by Coverage Type (First-Party Coverage, Third-Party Liability, and Bundled/Hybrid), Insurance Type (Stand-Alone Cyber, and Packaged/Endorsement), Organization Size (SMEs, and Large Enterprises), End-User Industry (BFSI, Healthcare, Retail and E-Commerce, IT and Telecom, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America generated 39.66% of global premiums in 2025, anchored by pervasive disclosure laws and a litigious environment that magnifies third-party settlement values. SEC rules obliging public issuers to report incidents within four business days standardize claims timelines and improve model accuracy. Canada's 2024 breach-notification amendments have harmonized cross-border requirements, making regional programs easier to structure. Yet saturation among Fortune 500 buyers is tempering volume growth, directing carrier focus toward middle-market firms and municipalities.

Asia-Pacific is expected to log the fastest expansion at 16.12% through 2031, propelled by China's Personal Information Protection Law and India's CERT-In six-hour incident-report directive, both of which compel multinational companies to arrange local-admitted policies. Singapore and Hong Kong regulators now encourage cyber insurance as part of operational-risk capital planning for banks, while Australia's revised Security of Critical Infrastructure Act imposes 12-hour outage reporting and heavy penalties for non-compliance, driving uptake in telecom and energy sectors. Low historical claims data still suppresses capacity, but carriers are partnering with regional reinsurers to share accumulation risk.

Europe's trajectory is shaped by DORA, which forces financial entities to test resilience triennially and hold boards accountable for cyber oversight. Germany's BaFin now links capital reserves to measured exposure, nudging banks toward third-party transfer. Lloyd's war-exclusion clause LMA5565, introduced in 2023, excludes state-sponsored operations and has driven European buyers to negotiate carve-backs or secure supplemental political-risk covers. South America, the Middle East and Africa remain nascent; while the United Arab Emirates and Saudi Arabia have national cyber-security mandates, local underwriting capacity remains thin, opening space for parametric, fronted, or reinsurance-backed solutions to seed market development.

- American International Group (AIG)

- Chubb Limited

- Zurich Insurance Group

- AXA XL

- Allianz Global Corporate and Specialty

- Fairfax Financial Holdings

- Beazley plc

- Munich Re Group

- Berkshire Hathaway Insurance Group

- Travelers Companies

- CNA Financial

- Hiscox Ltd.

- AXIS Capital Holdings

- Tokio Marine Holdings

- Sompo Holdings

- Aon plc

- Marsh McLennan

- Lockton Companies

- Coalition, Inc.

- Cowbell Cyber

- Swiss Reinsurance Company

- Lloyd's of London

- At-Bay

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-First Digitalization Upsizes Cyber-Loss Exposure

- 4.2.2 Escalating Regulatory Mandates (GDPR, NY DFS, DORA, SEC Rules)

- 4.2.3 Board-Level Focus on Quantifying Cyber Risk

- 4.2.4 SME-Focused Low-Cost Parametric Covers Emerging

- 4.2.5 InsurSec Models Bundling Security Services and Cover

- 4.2.6 Tokenized Cyber ILS Attracting New Capacity

- 4.3 Market Restraints

- 4.3.1 Actuarial Data Scarcity and Modeling Uncertainty

- 4.3.2 High Premium and Retention Levels Deter SMEs

- 4.3.3 Contractual War and Systemic-Risk Exclusions

- 4.3.4 Reinsurance Capacity Caps for Critical-Infrastructure Risks

- 4.4 Industry Supply-Chain Analysis

- 4.5 Regulatory Landscape and Industry Guidelines

- 4.6 Technological Outlook (AI Underwriting, CAT Models, Blockchain Parametrics)

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Consumers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Coverage Type

- 5.1.1 First-Party Coverage

- 5.1.2 Third-Party Liability

- 5.1.3 Bundled / Hybrid

- 5.2 By Insurance Type

- 5.2.1 Stand-Alone Cyber

- 5.2.2 Packaged / Endorsement

- 5.3 By Organisation Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-User Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare

- 5.4.3 Retail and E-Commerce

- 5.4.4 IT and Telecom

- 5.4.5 Manufacturing

- 5.4.6 Government and Public Sector

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Sweden

- 5.5.3.5 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Australia

- 5.5.4.5 South Korea

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 American International Group (AIG)

- 6.4.2 Chubb Limited

- 6.4.3 Zurich Insurance Group

- 6.4.4 AXA XL

- 6.4.5 Allianz Global Corporate and Specialty

- 6.4.6 Fairfax Financial Holdings

- 6.4.7 Beazley plc

- 6.4.8 Munich Re Group

- 6.4.9 Berkshire Hathaway Insurance Group

- 6.4.10 Travelers Companies

- 6.4.11 CNA Financial

- 6.4.12 Hiscox Ltd.

- 6.4.13 AXIS Capital Holdings

- 6.4.14 Tokio Marine Holdings

- 6.4.15 Sompo Holdings

- 6.4.16 Aon plc

- 6.4.17 Marsh McLennan

- 6.4.18 Lockton Companies

- 6.4.19 Coalition, Inc.

- 6.4.20 Cowbell Cyber

- 6.4.21 Swiss Reinsurance Company

- 6.4.22 Lloyd's of London

- 6.4.23 At-Bay

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment