PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043854

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043854

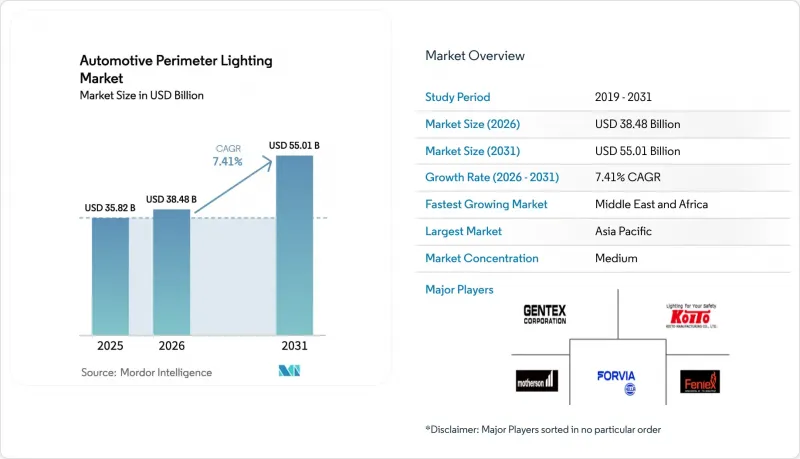

Automotive Perimeter Lighting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The automotive perimeter lighting market size was valued at USD 35.82 billion in 2025 and is estimated to grow from USD 38.48 billion in 2026 to reach USD 55.01 billion by 2031, at a CAGR of 7.41% during the forecast period (2026-2031).

As electrification advances and global lighting regulations tighten, lighting is evolving from a mere safety feature into a dynamic communication tool. Tier 1 suppliers are enhancing headlamps with adaptive matrix LED arrays that possess optical communication capabilities. These advancements allow headlamps to project warning symbols onto the road and sync with advanced driver-assistance systems. Meanwhile, as battery-electric platforms enforce stringent power limits, there's a surging demand for low-power solutions like OLEDs, fiber optics, and micro-LEDs. In recent years, the Asia-Pacific region has maintained a dominant position in global revenue generation. However, looking ahead, the Middle East and Africa are poised to emerge as the fastest-growing regions, driven by the Gulf Cooperation Council's integration of V2X lighting into their new smart transport corridors.

Global Automotive Perimeter Lighting Market Trends and Insights

Rapid LED Penetration for Energy-Efficient Illumination

LED packages, operating at junction temperatures below a certain threshold, achieve an impressive output with high efficiency. This efficiency significantly reduces power consumption compared to halogen lights, freeing up battery capacity for cabin climate controls, as highlighted in Tesla's recent engineering disclosures . Recently, a significant milestone was reached as Chinese factories lowered LED module prices to a highly competitive level, erasing the economic advantage that had long protected halogen lamps. The European retrofit market gained momentum following regulatory endorsements of street-legal LED replacements, creating substantial opportunities across the region's extensive vehicle base. Despite these advancements, LED driver chips continued to face prolonged lead times, reflecting ongoing semiconductor supply challenges.

Regulatory Mandates for Enhanced Road-Safety Lighting

United Nations Regulation 48 amendments now oblige new European passenger cars to carry adaptive driving beams from 2025, while China's GB 25991-2024 adds automatic high-beam control for vehicles over 1,800 kg. Automakers have swapped static halogens for matrix LED arrays that blank out glare zones, and the U.S. National Highway Traffic Safety Administration finally legalized adaptive-beam technology in 2024, unleashing pent-up demand among North American OEMs . Divergent roll-out calendars split global platforms into mandatory-fit regions and option-package regions, raising per-unit costs and fragmenting supply chains. Japan's new glare-measurement protocol also forced recalibration of beam intensity in 2025, delaying several model releases by one to two quarters.

High Cost of Advanced LED/OLED & Adaptive Systems

Matrix LED headlamps are significantly more expensive than static units, while OLED tail-lamps also come at a noticeable premium over LED equivalents, restricting their adoption primarily to the premium market segment. In markets like India and Brazil, halogen lights remain the preferred choice for vehicles in the affordable price range. This preference necessitates suppliers to operate dual production lines. In the near future, Valeo is expected to achieve a notable reduction in OLED module costs by increasing production volumes. This development suggests a potential path toward cost parity within a few years, provided there is a substantial increase in orders.

Other drivers and restraints analyzed in the detailed report include:

- EV Adoption Driving Demand for Low-Power Lighting

- Software-Defined / V2X Communicative Lighting Platforms

- Semiconductor Supply-Chain Volatility for LED Drivers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

LED continued to dominate the automotive perimeter lighting market with a 63.17% share in 2025, and is projected to record a 7.43% CAGR to 2031, outpacing all other sources. Automakers value LED flexibility that removes bulky diffusers, trimming part count almost in half while enabling sculpted 3-D lamp surfaces. Xenon high-intensity discharge and halogen technologies now form a shrinking niche as regulatory deadlines in China and the EU phase them out by 2028. Suppliers are advancing micro-LED arrays, which deliver ten-fold pixel density improvements and pave the way for high-resolution road-surface projections.

The automotive perimeter lighting market size for LED segments is forecast to remain above USD 30 billion throughout the forecast period. Still, LED revenue will triple from a small base as luxury models adopt zone-specific dimming. Micro-LED and laser-phosphor modules, though accounting for under 2% of 2025 volume, absorb a disproportionate share of R&D budget as Koito, Valeo, and HELLA file patents on thermal management and beam-steering optics.

Plastics such as polycarbonate and ABS accounted for 57.71% of the automotive perimeter lighting market share in 2025, driven by well-established molding supply chains. Yet, fiber-reinforced composites are growing at a 7.51% CAGR as OEMs pursue mass savings in battery-electric vehicles. Carbon-fiber-reinforced polycarbonate lenses deliver weight reductions while maintaining impact resistance and optical clarity, attracting premium EV programs. Glass lenses persist on flagship nameplates where long-term scratch resistance is paramount, though shares slip as polycarbonate hard coats replicate glass durability.

The automotive perimeter lighting market share that plastics command is expected to contract marginally as composites gain market share. Suppliers such as Covestro now offer bio-attributed polycarbonate that reduces lifecycle carbon emissions by a minimal amount, aligning with OEM scope-3 emission targets. Fiber-optic light guides further reduce wiring runs and shave 20 seconds off assembly time, though high alignment precision keeps volume restricted to platforms that can justify automated fixtures.

The Automotive Perimeter Lighting Market Report is Segmented by Light Type (LED, Halogen, and More), Material (Plastic, Glass, and More), Application (Interior and Exterior), Vehicle Type (Passenger Cars and More), Sales Channel (OEM and Aftermarket), and Geography. The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

Asia-Pacific accounted for 43.26% of the automotive perimeter lighting market revenue in 2025, driven by China's strong LED manufacturing capabilities, Japan's advanced OLED research and development, and South Korea's expertise in electronics integration. A regulatory mandate in China requiring adaptive driving beams for heavier vehicles is expected to make matrix LEDs standard equipment across most domestic platforms, ensuring consistent growth in the coming years. Meanwhile, Japan's Koito and Stanley, which hold a significant share of the global OEM headlamp market, are advancing their micro-LED pilot lines. Additionally, Hyundai Mobis has committed substantial investments to expand its OLED production facilities in Cheonan.

The Middle East and Africa will be the fastest-growing region, with a 7.47% CAGR through 2031. Gulf smart-city initiatives, such as Dubai's V2X testbeds, are driving the demand for communicative lighting solutions. Furthermore, Turkey's robust vehicle export activities are prompting local suppliers to enhance their LED module production capacities. In South Africa, the country's role as a right-hand-drive assembly hub for major automakers like BMW and Mercedes-Benz is fostering local lens production to mitigate tariff-related challenges.

Europe and North America remain content-rich markets, albeit with slower growth rates. The EU's General Safety Regulation, which links advanced driver-assistance systems (ADAS) to glare-free lighting, has effectively mandated adaptive matrix LEDs for all new vehicle models. In the United States, regulatory changes now allow adaptive beams and LED retrofit bulbs, creating a significant upgrade market opportunity. In South America, although growth is slower, Brazil's fleet-renewal program is accelerating the transition away from halogen lighting, laying the groundwork for a broader shift to LED technology.

- Koito Manufacturing Co., Ltd.

- Valeo SA

- HELLA GmbH & Co. KGaA (FORVIA)

- Gentex Corporation

- Magna International Inc.

- Stanley Electric Co., Ltd.

- OSRAM Continental GmbH

- ZKW Group GmbH

- Varroc Engineering Ltd.

- Marelli Holdings Co., Ltd.

- Samvardhana Motherson Group

- Hyundai Mobis Co., Ltd.

- DENSO Corporation

- TYC Brother Industrial Co., Ltd.

- Changzhou Xingyu Automotive Lighting Systems Co., Ltd.

- SL Corporation

- HASCO Vision Technology Co., Ltd.

- Lumax Industries Limited

- Depo Auto Parts Industrial Co., Ltd.

- Nichia Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid LED Penetration for Energy-Efficient Illumination

- 4.2.2 Regulatory Mandates for Enhanced Road-Safety Lighting

- 4.2.3 EV Adoption Driving Demand for Low-Power Perimeter Lighting

- 4.2.4 OEM Shift to Modular Front-End Architectures Integrating Lighting

- 4.2.5 Software-Defined / V2X Communicative Lighting Platforms

- 4.2.6 Aftermarket Customization Culture Boosting Lighting Upgrades

- 4.3 Market Restraints

- 4.3.1 High Cost of Advanced Led/Oled & Adaptive Systems

- 4.3.2 Semiconductor Supply-Chain Volatility for Led Drivers

- 4.3.3 Cyber-Security & Functional-Safety Certification Hurdles

- 4.3.4 Light-Pollution Compliance Limiting Beam Patterns/Brightness

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value (USD) and Volume (Units))

- 5.1 By Light Type

- 5.1.1 LED Lights

- 5.1.2 Halogen

- 5.1.3 Xenon

- 5.1.4 Others

- 5.2 By Material

- 5.2.1 Plastic

- 5.2.2 Glass

- 5.2.3 Fiber

- 5.2.4 Others

- 5.3 By Application

- 5.3.1 Interior Perimeter Lighting

- 5.3.2 Exterior Perimeter Lighting

- 5.4 By Vehicle Type

- 5.4.1 Passenger Cars

- 5.4.2 Light Commercial Vehicles (LCV)

- 5.4.3 Medium and Heavy Commercial Vehicles (HCV)

- 5.5 By Sales Channel

- 5.5.1 OEM (Original Equipment Manufacturers)

- 5.5.2 Aftermarket

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Rest of North America

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Turkey

- 5.6.5.5 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, SWOT Analysis, and Recent Developments)

- 6.4.1 Koito Manufacturing Co., Ltd.

- 6.4.2 Valeo SA

- 6.4.3 HELLA GmbH & Co. KGaA (FORVIA)

- 6.4.4 Gentex Corporation

- 6.4.5 Magna International Inc.

- 6.4.6 Stanley Electric Co., Ltd.

- 6.4.7 OSRAM Continental GmbH

- 6.4.8 ZKW Group GmbH

- 6.4.9 Varroc Engineering Ltd.

- 6.4.10 Marelli Holdings Co., Ltd.

- 6.4.11 Samvardhana Motherson Group

- 6.4.12 Hyundai Mobis Co., Ltd.

- 6.4.13 DENSO Corporation

- 6.4.14 TYC Brother Industrial Co., Ltd.

- 6.4.15 Changzhou Xingyu Automotive Lighting Systems Co., Ltd.

- 6.4.16 SL Corporation

- 6.4.17 HASCO Vision Technology Co., Ltd.

- 6.4.18 Lumax Industries Limited

- 6.4.19 Depo Auto Parts Industrial Co., Ltd.

- 6.4.20 Nichia Corporation

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment