PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043855

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043855

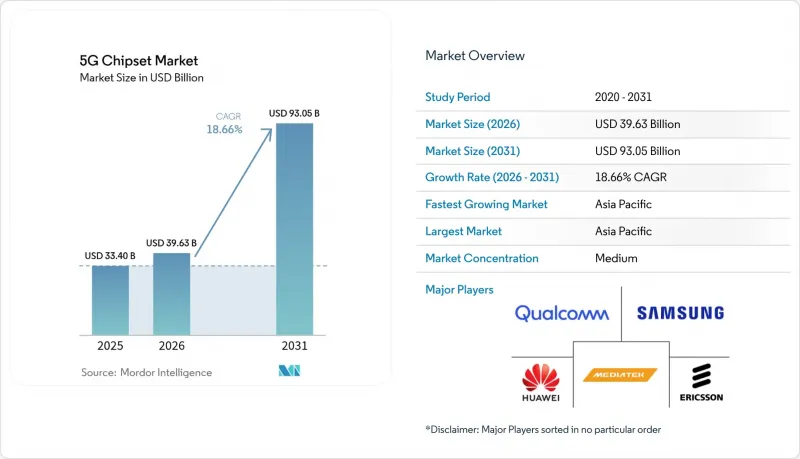

5G Chipset - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The 5G Chipset Market size is projected to expand from USD 33.40 billion in 2025 and USD 39.63 billion in 2026 to USD 93.05 billion by 2031, registering a CAGR of 18.66% between 2026 to 2031.

Sustained infrastructure spending, growing edge-AI workloads, and intensified private-network adoption continue to fuel demand for specialized silicon. Sub-6 GHz roll-outs keep volumes high, while mmWave and sub-3 nm migrations add value through premium pricing. Government incentives, most notably the USD 52.7 billion CHIPS Act, are boosting domestic fab capacity in the United States. Rising geopolitical risk around export controls and gallium supply underscores the need for dual-sourcing strategies. Against this backdrop, the 5G chipset market is benefiting from tighter vertical integration among device makers and network vendors that seek to secure differentiated IP and supply resilience.

Global 5G Chipset Market Trends and Insights

Surging Global 5G RAN Roll-outs Drive Infrastructure Semiconductor Demand

Commercial 5G population coverage is set to reach 80% by 2029, up from 40% in 2024, pushing operators to densify networks and invest in high-capacity backhaul. Small-cell architectures require efficient RF front-end modules optimized for mid-band and mmWave operation, while massive MIMO deployments call for advanced power-management ICs that keep energy budgets in check. Demand spikes are most visible across Asia-Pacific, where China added over 800,000 5G base stations in 2024 alone. These factors sustain a broad revenue base for both digital and analog 5G chipset market participants.

mmWave Spectrum Auctions Unlock Advanced Silicon Opportunities

Aggressive spectrum auctions in the 24-47 GHz bands have attracted more than USD 35 billion in bids since 2024 in the United States, Japan, and South Korea. mmWave's short propagation range mandates advanced beam-forming ICs, high-linearity power amplifiers, and adaptive antenna-tuning chips, each commanding premium gross margins. Fixed-wireless access roll-outs place particular stress on thermal design and yield improvements, rewarding vendors that can offer integrated front-end reference designs with robust calibration software.

Geopolitical Export Controls Create Strategic Semiconductor Bottlenecks

The U.S. Bureau of Industry and Security has expanded its Entity List to restrict the export of advanced EDA tools, lithography systems, and HBM to select Chinese fabless firms. China's countermeasure limiting gallium and germanium exports could raise gallium prices by 150% and shave USD 3.4 billion off U.S. GDP. These moves force design houses to requalify nodes, build inventory buffers, and invest in diversified supply routes, trimming near-term profitability across the 5G chipset market.

Other drivers and restraints analyzed in the detailed report include:

- Edge-AI Workloads Accelerate Advanced Node Adoption

- Open RAN Disaggregation Transforms Vendor Ecosystem Dynamics

- Supply-Chain Fragility Threatens Compound Semiconductor Availability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

ASICs captured the largest 25.40% revenue share in 2025 as OEMs pursued power-optimized, application-specific performance. This dominance is evident in radio-unit baseband processors that offload Layer-1 scheduling duties. By contrast, FPGAs are forecast to outpace all peers at a 19.94% CAGR, buoyed by Open RAN pilots that value reconfigurability for evolving 3GPP releases. The 5G chipset market size allocated to ASIC-based baseband units is expected to reach USD 34.2 billion by 2031. System-on-Chip solutions with integrated modems continue gaining popularity in smartphones, wearables, and C-V2X modules because they shrink PCB footprint and lower bill-of-materials costs.

FPGAs also underpin inline accelerator cards that relieve x86 servers of forward-error correction tasks, thereby improving spectral efficiency in virtualized RAN deployments. RFICs maintain steady volume, delivering wide-band front-end filtering and phase-array beam-forming at both mid-band and mmWave frequencies. Millimeter-wave technology chips, antenna tuners, LNAs, power amplifiers, and power-management ICs round out an ecosystem built around mix-and-match reference designs. Collectively, these categories ensure that the 5G chipset market remains vibrant across both commodity and high-margin niches.

The 5 nm platform accounted for 31.10% of 2025 sales thanks to strong tape-out volume from smartphone modems and cloud accelerator ASICs. Yet sub-3 nm wafers will generate the fastest 20.12% CAGR because edge-AI workloads demand superior performance per watt. The 5G chipset market share for 2 nm chips is projected to climb as TSMC ramps N2 in H2 2025 and Samsung introduces MBCFET gate-all-around architecture. 7 nm remains the node of choice for mid-range handsets, while 16 nm and 28 nm continue serving cost-sensitive IoT gateways and RF switch matrices.

Mature nodes above 28 nm anchor power-management and analog peripherals, where voltage tolerance outweighs density. This balanced node mix cushions supply-demand swings and offers design-for-availability flexibility when geopolitical or natural-disaster shocks disrupt cutting-edge capacity.

The 5G Chipset Market Report is Segmented by Chipset Type (Application-Specific Integrated Circuits, System-On-Chip With Integrated Modem, and More), Technology Node (<3nm, 3nm, 5nm, 7nm, and More), Operational Frequency (Sub-6 GHz, 26-39 GHz, and Above 39 GHz), End-User Industry (IT, Telecom and Network Infrastructure, Consumer Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 47.50% of global revenue in 2025 and is projected to grow at a 19.22% CAGR through 2031. China alone installed more than 1.8 million 5G base stations by mid-2025 despite export-control pressure, securing local demand for RF front-ends and baseband ASICs. South Korea and Japan emphasize mmWave densification, encouraging higher-margin chipset bill-of-materials. India's PLI scheme supports emerging fab projects targeting 28 nm power-management and RF switch nodes, broadening regional supply diversity.

North America benefits from the CHIPS Act's infusion and early mmWave adoption. The United States accounts for over 80% of global mmWave device shipments and drives demand for beam-forming ICs. Canada focuses on rural fixed-wireless initiatives that favor sub-6 GHz C-band front-ends. Europe lags in standalone-core adoption; only 2% of sites had full SA functionality by 2025, compared with 24% in the United States. Nordic operators, however, maintain near-complete coverage, driving localized silicon content for energy-efficient macro-cells suited to cold climates.

The Middle East and Africa experience stepped growth, with Gulf Cooperation Council nations building large-scale IoT corridors. South America sees uneven progress as Brazil pushes forward while Argentina grapples with macroeconomic constraints. Overall, regional policy support and spectrum allocation pace remain leading determinants of 5G chipset market momentum.

List of Companies Covered in this Report:

- Qualcomm Incorporated

- MediaTek Inc.

- Samsung Electronics Co., Ltd.

- Huawei Technologies Co., Ltd.

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Broadcom Inc.

- Fujitsu Limited

- Renesas Electronics Corporation

- Marvell Technology, Inc.

- Texas Instruments Incorporated

- NXP Semiconductors N.V.

- Skyworks Solutions, Inc.

- Qorvo, Inc.

- Analog Devices, Inc.

- STMicroelectronics N.V.

- Infineon Technologies AG

- Murata Manufacturing Co., Ltd.

- Anokiwave, Inc.

- pSemi Corporation

- GlobalFoundries Inc.

- Taiwan Semiconductor Manufacturing Company Ltd.

- United Microelectronics Corporation

- Cree Wolfspeed, Inc.

- Integrated Device Technology, Inc. (Renesas Subsidiary)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Global 5G RAN Roll-outs

- 4.2.2 mmWave Spectrum Auctions Unlocking New Silicon Demand

- 4.2.3 Edge-AI Workloads Shifting Toward 5 nm and Below Nodes

- 4.2.4 Open RAN Disaggregation Driving Merchant Silicon Uptake

- 4.2.5 Private-5G Adoption Across Industry 4.0 Facilities

- 4.2.6 Government CHIPS-style Subsidies for Domestic Fabs

- 4.3 Market Restraints

- 4.3.1 Geopolitical Export Controls on Advanced Nodes

- 4.3.2 Supply-chain Fragility for Compound Semiconductors

- 4.3.3 High Cap-ex Requirements Below 3 nm

- 4.3.4 Power-efficiency Trade-offs in mmWave Devices

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Chipset Type

- 5.1.1 Application-Specific Integrated Circuits (ASICs)

- 5.1.2 System-on-Chip with Integrated Modem (SoC)

- 5.1.3 Radio-Frequency Integrated Circuits (RFICs)

- 5.1.4 Millimeter-Wave Technology Chips

- 5.1.5 Field-Programmable Gate Arrays (FPGAs)

- 5.1.6 Power Management ICs

- 5.1.7 Antenna Tuner ICs

- 5.1.8 Switches

- 5.1.9 LNAs and Power Amplifiers

- 5.1.10 Others (Filters, Discrete Memory, Converters, etc.)

- 5.2 By Technology Node

- 5.2.1 < 3 nm

- 5.2.2 3 nm

- 5.2.3 5 nm

- 5.2.4 7 nm

- 5.2.5 16 nm

- 5.2.6 28 nm

- 5.2.7 > 28 nm

- 5.3 By Operational Frequency

- 5.3.1 Sub-6 GHz

- 5.3.2 26-39 GHz

- 5.3.3 Above 39 GHz

- 5.4 By End-User Industry

- 5.4.1 IT, Telecom and Network Infrastructure

- 5.4.2 Consumer Electronics (incl. Smart Home)

- 5.4.3 Industrial Automation

- 5.4.4 Automotive and Transportation

- 5.4.5 Energy and Utilities

- 5.4.6 Healthcare

- 5.4.7 Retail

- 5.4.8 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 South Korea

- 5.5.4.4 India

- 5.5.4.5 Singapore

- 5.5.4.6 Australia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Egypt

- 5.5.5.2.4 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Qualcomm Incorporated

- 6.4.2 MediaTek Inc.

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 Huawei Technologies Co., Ltd.

- 6.4.5 Telefonaktiebolaget LM Ericsson

- 6.4.6 Nokia Corporation

- 6.4.7 Broadcom Inc.

- 6.4.8 Fujitsu Limited

- 6.4.9 Renesas Electronics Corporation

- 6.4.10 Marvell Technology, Inc.

- 6.4.11 Texas Instruments Incorporated

- 6.4.12 NXP Semiconductors N.V.

- 6.4.13 Skyworks Solutions, Inc.

- 6.4.14 Qorvo, Inc.

- 6.4.15 Analog Devices, Inc.

- 6.4.16 STMicroelectronics N.V.

- 6.4.17 Infineon Technologies AG

- 6.4.18 Murata Manufacturing Co., Ltd.

- 6.4.19 Anokiwave, Inc.

- 6.4.20 pSemi Corporation

- 6.4.21 GlobalFoundries Inc.

- 6.4.22 Taiwan Semiconductor Manufacturing Company Ltd.

- 6.4.23 United Microelectronics Corporation

- 6.4.24 Cree Wolfspeed, Inc.

- 6.4.25 Integrated Device Technology, Inc. (Renesas Subsidiary)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment