PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043856

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043856

Japan Property And Casualty Insurance - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

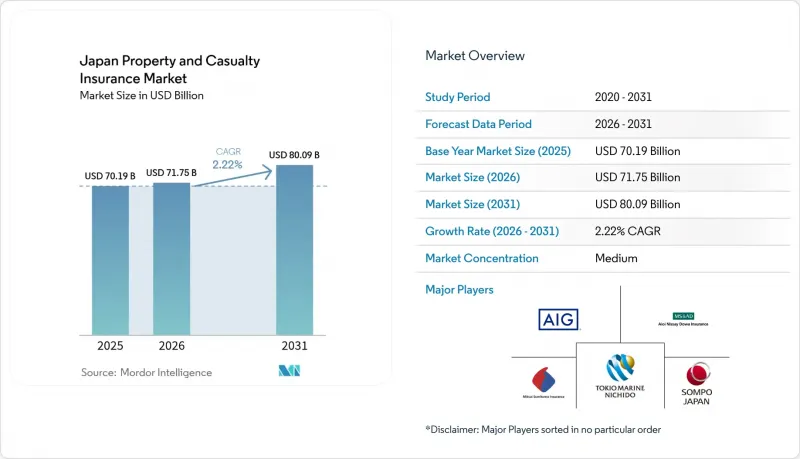

The Japan Property And Casualty Insurance Market size is projected to expand from USD 70.19 billion in 2025 and USD 71.75 billion in 2026 to USD 80.09 billion by 2031, registering a CAGR of 2.22% between 2026 to 2031.

The Japan property and casualty insurance market shows steady expansion in 2026, as carriers rebalance pricing and coverage terms after several intense catastrophe seasons that reset risk appetites and underwriting standards. The Japan property and casualty insurance market is also adapting to a new regulatory capital regime, with the Financial Services Agency implementing an economic value-based solvency framework by March 2026 that heightens capital discipline and disclosure requirements. Loss experience from 2024 events, including the Noto Peninsula earthquake and severe convective storms, continues to influence property rate adequacy and deductibles as claim settlements progress through 2025. New embedded and affinity pathways in payments and real estate transactions are widening reach in personal lines through point-of-sale integration and paperless onboarding that aligns with consumer expectations for digital convenience. Strategic moves by leading groups, including a definitive merger plan at MS&AD and an international acquisition by Sompo, signal active portfolio optimization and inorganic growth to support resilience in the Japan property and casualty insurance market.

Japan Property And Casualty Insurance Market Trends and Insights

Telematics-Driven Auto Adoption Accelerates Premium Growth

Usage-based and behavior-based programs continue to scale in 2026, supported by an expanding installed base and proven safety outcomes that help stabilize motor loss experience in the Japan property and casualty insurance market. Cambridge Mobile Telematics reported surpassing 1 million active drivers on its platform in Japan by mid-2025, and partner programs recorded crash frequency reductions and improved customer satisfaction among enrolled drivers . The General Insurance Rating Organization of Japan introduced a model-specific vehicle classification that segments automobiles into 17 classes, which supports more granular risk pricing and aligns with telematics insights used by leading carriers. Several insurers are expanding capabilities for in-vehicle incident video and real-time alerts to improve claims adjudication and enhance road safety, with product updates scheduled into 2026. Rising distraction-related crash statistics reinforce the value of behavior scoring and driver coaching, which underpins ongoing investment in telematics by insurers seeking more stable results in the Japan property and casualty insurance market.

Sustained Repricing in Fire/Property from Natural Catastrophe and Repair-Cost Inflation

Carriers continued to adjust fire and property pricing in late 2024 and through 2025 after a series of severe events, with loss experience and higher repair inputs requiring stricter underwriting in the Japan property and casualty insurance market. Claims from the January 2024 Noto Peninsula earthquake totaled USD 0.67 billion (JPY 104.8 billion) across 126,698 policies, and a large hail event in Hyogo in April 2024 generated USD 0.87 billion (JPY 135.96 billion) in claims across 149,612 policies. Typhoon Shanshan in 2024 added USD 0.35 billion (JPY 54.9 billion) in claims, with a large proportion borne by fire insurance, which further pressured underwriting margins. The Financial Services Agency's second climate scenario analysis indicates that average annual claim payments for typhoons and floods increase in higher warming paths, which supports continued repricing and capacity calibration by insurers. Leading carriers responded with targeted actions, including the identification and remediation of unprofitable policies and more selective deployment of capacity in risk-sensitive property classes, which supports resilience in the Japan property and casualty insurance market.

Heavy Agent Dependence Amid Compliance Tightening Slows Channel Shifts

The sector features a large multi-agency footprint that has historically anchored personal and SME sales, which can slow the pace of digital channel substitution in the Japan property and casualty insurance market. The Financial Services Agency has strengthened supervisory guidance that requires insurers to enhance governance, ensure appropriate sales practices, and manage conflicts of interest more rigorously at shared agencies. Carriers are revising partner oversight, separating claims functions from sales, and refining commission frameworks to prioritize quality and compliance outcomes, which takes time to implement at scale. The transition requires training, new controls, and better data integration across carriers and intermediaries, which temporarily limits the speed of channel mix change in the Japan property and casualty insurance market. Over time, these measures are designed to restore trust, improve customer outcomes, and enable healthier competition.

Other drivers and restraints analyzed in the detailed report include:

- Earthquake Add-On Penetration and Stable State-Backed Capacity Lift Homeowner Cover

- Data-Led Natural Catastrophe Claims Enable Parametric Products

- Corporate Coinsurance Scrutiny and Cartel Fallout Elongate Placement Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Automobile insurance accounted for 50.38% of the Japan property and casualty insurance market size in 2025, which reflects mandatory coverages and the large in-force vehicle base that drives premium volume in personal lines. Cyber, grouped under other P&C lines, is projected to grow at a 17.38% CAGR through 2031, making it the fastest expanding line by growth rate in the Japan property and casualty insurance market. Property pricing remained firm into 2025 after repeated catastrophe years, and carriers pivoted capacity toward risks with better resilience attributes and clearer catastrophe mitigation features. Earthquake coverage attached to household fire policies continued to gain traction, supported by stable reinsurance capacity and risk-sharing mechanisms that enhance system durability. These dynamics are influencing product design, deductibles, and endorsements as insurers balance affordability and sustainability in the Japan property and casualty insurance industry.

Carriers are refining auto underwriting with vehicle-level risk classes and telematics, which tighten alignment between premium and expected loss and support the stability of the Japan property and casualty insurance market. In property, underwriting has tightened around older structures and exposures with adverse loss experience, paired with support for mitigation steps that qualify for discounts or favorable terms. Cyber adoption is accelerating across SMEs and mid-market corporates that face operational risk from ransomware and business interruption, with insurers investing in preventive controls and response services as part of bundled offerings. Data-enabled claims management, satellite imagery, and drone assessments are improving cycle times and cost accuracy after events, which reduces leakage and enhances customer experience within the Japan property and casualty insurance market. Across lines, the regulatory shift to economic value-based solvency is reinforcing capital discipline and transparency that shape product and portfolio decisions in the Japan property and casualty insurance industry.

The Japan Property and Casualty Insurance Market is Segmented Into Insurance Type (Property Insurance (Residential, Commercial, and More), Auto Insurance (Personal and Commercial Auto), Liability Insurance (Marine, Aviation and Transit, and More)), Distribution Channel (Direct, Agency Network, and More), End User (Individuals, Smes, Large Corporations, and More), and Geography. The Market Forecasts are Provided in Value (USD).

List of Companies Covered in this Report:

- Tokio Marine & Nichido Fire Insurance Co., Ltd.

- Mitsui Sumitomo Insurance Co., Ltd.

- Aioi Nissay Dowa Insurance Co., Ltd.

- Sompo Japan Insurance Inc.

- AIG General Insurance Company, Ltd. (AIG Japan)

- Sony Assurance Inc.

- Rakuten General Insurance Co., Ltd.

- SBI Insurance Co., Ltd.

- Mitsui Direct General Insurance Co., Ltd.

- Saison Automobile & Fire Insurance Co., Ltd.

- Kyoei Fire & Marine Insurance Co., Ltd.

- Nisshin Fire & Marine Insurance Co., Ltd.

- AXA General Insurance Co., Ltd. (AXA Direct Japan)

- Zurich Insurance Company Ltd, Japan Branch

- Chubb Insurance Japan

- HDI Global SE, Japan Branch

- Secom General Insurance Co., Ltd.

- E.design Insurance Co., Ltd. (Sompo Group)

- au Insurance Company, Limited (KDDI)

- Tokio Marine & Nichido Risk Consulting Co., Ltd. (risk solutions)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Telematics-driven auto adoption accelerates premium growth

- 4.2.2 Sustained repricing in fire/property from nat-cat and repair-cost inflation

- 4.2.3 Economic value-based solvency transition tightens capital discipline

- 4.2.4 Earthquake add-on penetration and stable state-backed capacity lift homeowner cover

- 4.2.5 Embedded and affinity distribution unlocks new micro-covers

- 4.2.6 Data-led nat-cat claims (satellite/drone/telematics) enable parametric products

- 4.3 Market Restraints

- 4.3.1 Auto claims inflation and parts/repair bottlenecks pressure loss ratios

- 4.3.2 Catastrophe aggregation and EQ cover caps create protection gaps

- 4.3.3 Heavy agent dependence amid compliance tightening slows channel shifts

- 4.3.4 Corporate coinsurance scrutiny and cartel fallout elongate placement cycles

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Supplier Power

- 4.7.3 Buyer Power

- 4.7.4 Threat of Substitutes

- 4.7.5 Threat of New Entrants

- 4.8 Japan Earthquake Insurance scheme mechanics and capacity stack (residential add-on)

- 4.9 CALI-voluntary auto split and 2025 risk-class reform (17-class model)

5 Market Size & Growth Forecasts

- 5.1 By Line of Business

- 5.1.1 Property Insurance

- 5.1.2 Auto Insurance

- 5.1.3 Liability Insurance

- 5.1.4 Marine, Aviation & Transit Insurance

- 5.1.5 Personal Accident & Miscellaneous Casualty

- 5.1.6 Other P&C Lines (incl. emerging Cyber, D&O, etc.)

- 5.2 By Distribution Channel

- 5.2.1 Agency Network

- 5.2.2 Direct

- 5.2.3 Bancassurance

- 5.2.4 Brokers

- 5.2.5 Affinity & Embedded Partnerships

- 5.2.6 Other Channels

- 5.3 By End-User

- 5.3.1 Individuals

- 5.3.2 SMEs

- 5.3.3 Large Corporations

- 5.3.4 Government & Public Sector

- 5.4 By Geography

- 5.4.1 Hokkaido & Tohoku

- 5.4.2 Kanto

- 5.4.3 Chugoku

- 5.4.4 Kyushu & Okinawa

- 5.4.5 Rest of Japan

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Tokio Marine & Nichido Fire Insurance Co., Ltd.

- 6.4.2 Mitsui Sumitomo Insurance Co., Ltd.

- 6.4.3 Aioi Nissay Dowa Insurance Co., Ltd.

- 6.4.4 Sompo Japan Insurance Inc.

- 6.4.5 AIG General Insurance Company, Ltd. (AIG Japan)

- 6.4.6 Sony Assurance Inc.

- 6.4.7 Rakuten General Insurance Co., Ltd.

- 6.4.8 SBI Insurance Co., Ltd.

- 6.4.9 Mitsui Direct General Insurance Co., Ltd.

- 6.4.10 Saison Automobile & Fire Insurance Co., Ltd.

- 6.4.11 Kyoei Fire & Marine Insurance Co., Ltd.

- 6.4.12 Nisshin Fire & Marine Insurance Co., Ltd.

- 6.4.13 AXA General Insurance Co., Ltd. (AXA Direct Japan)

- 6.4.14 Zurich Insurance Company Ltd, Japan Branch

- 6.4.15 Chubb Insurance Japan

- 6.4.16 HDI Global SE, Japan Branch

- 6.4.17 Secom General Insurance Co., Ltd.

- 6.4.18 E.design Insurance Co., Ltd. (Sompo Group)

- 6.4.19 au Insurance Company, Limited (KDDI)

- 6.4.20 Tokio Marine & Nichido Risk Consulting Co., Ltd. (risk solutions)

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment