PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043863

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043863

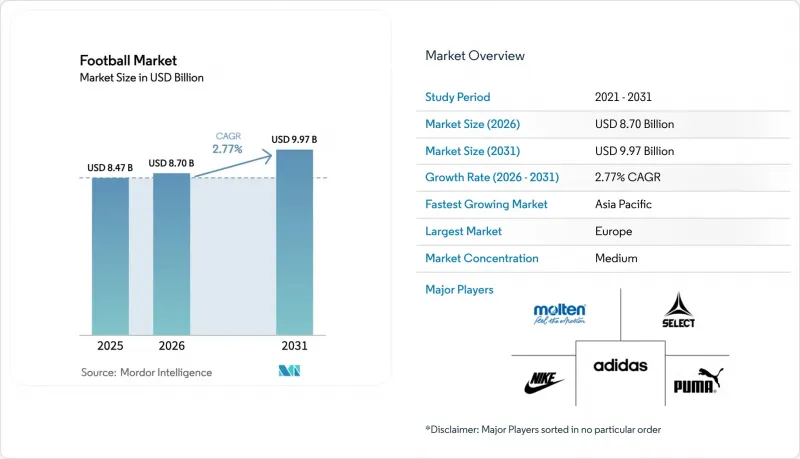

Football - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The global football market size recorded at USD 8.47 billoin in 2025, and reached USD 8.70 billion in 2026 and is projected to attain USD 9.97 billion by 2031, reflecting a CAGR of 2.77% over the period.

Despite certain segments of the gaming industry experiencing stagnation, live-match attendance continues to demonstrate strong engagement, highlighting the enduring appeal of in-person stadium experiences. Digital commerce is witnessing significant acceleration as brands increasingly integrate loyalty programs with online-exclusive offerings. At the same time, offline retail stores maintain their relevance by catering to consumers' preference for tactile shopping experiences. Sialkot, Pakistan, serves as a critical manufacturing hub, contributing significantly to global football production. This concentration provides notable scale efficiencies but also exposes the supply chain to potential geopolitical risks. In Europe and North America, the adoption of premium sensor-enabled footballs is driving an increase in average selling prices. Conversely, in regions such as Asia and Africa, mass-market PVC footballs continue to dominate in terms of volume. Suppliers that successfully combine technological innovation with cost-effective production strategies are well-positioned to capture market share across both grassroots and elite segments of the football market.

Global Football Market Trends and Insights

Rising popularity of football as a global sport

Football's growing popularity is significantly driving the global market, with a notable rise in demand for broadcasting rights, sponsorships, and merchandise. This growth is propelled by extensive fan bases, the appeal of global tournaments such as the World Cup, and increasing participation rates, particularly among youth and women. These factors are generating substantial revenue streams across various segments, including media, apparel, equipment, and digital platforms, thereby expanding the economic ecosystem from elite professional clubs to grassroots initiatives. For example, Sport England reported that in 2024, 40% of children in England participated in football, highlighting the sport's widespread appeal . Institutional investments and advancements in digital engagement are further enhancing football's global reach, ensuring consistent demand for equipment across all levels of participation. During the 2024/25 season, UEFA competitions attracted over 240 million spectators, showcasing the sport's ability to drive cross-border consumer spending . This immense popularity translates into increased equipment sales through two primary channels: direct participation, which includes schools, amateur clubs, and personal use, and aspirational purchases, often influenced by the excitement surrounding major tournament cycles.

Growth of professional leagues and competitions

As leagues continue to expand and diversify their competition formats, they are unlocking new commercial opportunities, which are driving a surge in institutional ball procurement. This evolving model is being replicated across Asia. For instance, India's Indian Super League has significantly increased its viewership base, which has, in turn, attracted lucrative multi-year broadcast agreements, further solidifying its market presence. Similarly, in China, multi-club ownership groups are implementing standardized equipment specifications across their portfolio of clubs. This standardization creates economies of scale, benefiting suppliers capable of meeting centralized procurement requirements efficiently. In Europe, the introduction of post-season playoffs and modifications to league formats are contributing to an increase in match inventory, thereby enhancing commercial potential. Additionally, Puma's forthcoming five-year partnership with the Premier League, set to commence in the 2025/26 season and replacing Nike, highlights the critical role of league rights in shaping market dynamics. These rights not only amplify brand visibility but also necessitate significant research and development investments. Suppliers are required to develop footballs that consistently meet FIFA Quality Pro standards, ensuring optimal performance under varying weather conditions and across diverse pitch surfaces throughout the league's 38 matchweeks.

Growing popularity of online gaming

The growing intersection between physical football and video game engagement introduces a substitution risk. An EA executive noted that younger fans increasingly discover football through video games rather than attending matches, leading to a generation whose primary connection to the sport is digital. This trend carries notable commercial implications. The substitution occurs in two key ways: time spent gaming reduces the hours available for physical play, and spending on in-game microtransactions, such as Ultimate Team packs, competes with discretionary spending on physical football equipment. The expansion of internet access further supports online gaming. For example, the International Telecommunication Union estimated that by 2025, approximately 6 billion people, about three-quarters of the global population, will have internet access, up from 5.8 billion in 2024 . If digital engagement declines, physical football equipment could see a resurgence, especially if clubs and federations enhance grassroots programs to rebuild physical participation rates among Gen Z.

Other drivers and restraints analyzed in the detailed report include:

- Technological advancements in football manufacturing

- Rising sponsorships and partnerships from brands

- High equipment and infrastructure costs limit accessibility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Size 5 balls, the official standard for players aged 12 and older, accounted for 51.28% of the market share, highlighting their importance in both professional competitions and adult recreational activities. Meanwhile, Size 1 and 2 balls, measuring 18-20 inches in circumference and primarily designed for skill development among children under 8, are expected to grow at a rate of 2.98% through 2031, representing the fastest growth within the size segmentation. This growth is largely driven by FIFA's "Football for Schools" initiative, which works with national education ministries to distribute age-appropriate equipment. This strategy bypasses traditional retail channels and ensures a steady demand for smaller sizes. Size 3 balls, commonly used by players aged 8-12, occupy a moderate position in terms of both volume and growth. In contrast, Size 4 balls, previously the standard for youth competitions aged 8-12 in certain regions, are increasingly being replaced. Many leagues are shifting to Size 5 for players as young as 10 to accelerate skill development.

These trends indicate that suppliers must optimize production lines to accommodate different size specifications, each with distinct margin characteristics. While Size 1 and 2 balls generate lower revenue per unit, their high turnover, driven by institutional procurement, offsets this limitation. Conversely, Size 5 balls command premium pricing due to technological advancements. For instance, innovations like Adidas's "Connected Ball" and Select's "iBalls" are exclusively available in Size 5. This exclusivity stems from challenges such as sensor miniaturization and battery life, which make smaller sizes economically unviable at current cost levels. Additionally, Molten's AFC Asian Qualifiers ball, designed with heat-resistant adhesives for artificial turf and high-temperature conditions, demonstrates the R&D investments that are feasible for Size 5 but not for smaller sizes. Manufacturers focusing on Asia-Pacific growth must address these complexities: China's school football programs prioritize Size 4 and 5 balls, while India's grassroots initiatives favor Size 3. This requires localized inventory strategies, increasing working capital demands but aligning with regional demand patterns.

In 2025, mass-market footballs accounted for 76.32% of the market share. These footballs, designed for recreational players, schools, and amateur clubs, focused on affordability rather than performance. Conversely, premium footballs, featuring advancements like thermal bonding, sensor technology, and FIFA Quality Pro certification, are projected to grow at a rate of 3.28% through 2031. This growth rate surpasses the market average by 51 basis points, driven by their adoption in professional leagues and elite training academies. Adidas's FUSSBALLLIEBE exemplifies this premium segment. Priced at EUR 150 (approximately USD 163) and set to debut in UEFA Euro 2024, the ball incorporates a 500Hz IMU sensor. This technology enables real-time offside detection and provides broadcasters with trajectory analytics, justifying its 5-7x price premium over mass-market alternatives. Similarly, Select Sport's iBalls, which have earned FIFA Quality Pro certification and feature integrated KINEXON sensors, extend these capabilities to training environments. These sensors allow coaches to measure shot metrics, a capability previously confined to lab testing.

Mass-market footballs, typically made with PVC covers and butyl bladders, compete primarily on price and durability. These affordable products drive the market's volume. For example, Decathlon's expansion in India, with a goal of achieving 85% local sourcing by 2026, relies on strong demand for mass-market footballs in tier-2 and tier-3 cities, where lower income levels limit premium product adoption. This market segmentation has created distinct competitive dynamics: premium brands like Adidas, Select, and Molten focus on innovation and partnerships with federations, while mass-market players such as Decathlon, Baden, and unbranded manufacturers emphasize distribution reach and cost efficiency. Puma, aiming to capture a share of the premium market, has secured a partnership with the Premier League for the 2025/26 season. By leveraging the league's visibility, Puma seeks to justify higher price points. However, the brand faces execution risks due to recent financial challenges and inventory issues.

The Football Market Report is Segmented by Size (Size 1 and 2, Size 3, Size 4, and Size 5), Category (Mass and Premium), End Use (Personal and Commercial), Distribution Channel (Online Stores and Offline Stores), and Geography (North America, South America, Europe, Asia-Pacific, Middle East, and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Units).

Geography Analysis

In 2025, Europe accounted for 41.21% of the market share, supported by its strong professional leagues, high participation rates, and established retail networks. Europe's football infrastructure is highly developed: Germany's Bundesliga and England's Premier League consistently achieve over 95% stadium capacity utilization. This high level of engagement drives consistent demand for match balls and training equipment. Additionally, lower-tier leagues attracted over 80 million spectators during the 2024/25 season, highlighting widespread interest beyond top-tier competitions. Puma will replace Nike as the Premier League's partner starting in the 2025/26 season, a move expected to boost premium product adoption as the league's global visibility generates aspirational demand in international markets. Women's football is growing rapidly, creating a new procurement segment as federations integrate women's teams into club structures and enforce minimum investment requirements. However, economic challenges are reducing discretionary spending. Puma's revised 2025 forecast, which anticipates an operating loss due to U.S. tariffs and weak consumer sentiment, highlights increasing margin pressures. These challenges may push suppliers to focus on volume sales rather than pricing power in the short term.

Asia-Pacific is projected to grow at a rate of 4.22% through 2031, making it the fastest-growing region. This growth is driven by institutional investments in China and India, the expansion of grassroots programs, and increasing participation from the middle class. Decathlon's EUR 100 million investment in India over five years aims to establish 63 new stores and achieve 85% local sourcing by 2026. This reflects confidence in demand from tier-2 and tier-3 cities, where sports retail infrastructure remains underdeveloped. However, rising smartphone penetration and the adoption of digital payments are enabling rapid e-commerce growth. In China, multi-club ownership models are gaining traction, with private equity firms like 777 Partners and City Football Group leading the way. These models standardize equipment procurement across clubs, creating centralized buying power that benefits suppliers offering volume discounts and consistent quality. Japan and South Korea, while mature markets with slower growth, present opportunities for premium pricing due to consumers' willingness to pay for technology-enhanced products.

The Middle East and Africa offer varied opportunities influenced by sovereign investments and infrastructure challenges. Saudi Arabia's National Gaming and Esports Sector Strategy aims to contribute USD 13.3 billion to GDP by 2030. Interestingly, this strategy includes physical football development, blending digital and physical participation to diversify the sports ecosystem. Sub-Saharan Africa faces affordability and infrastructure barriers, but FIFA's Forward Programme provides a funding baseline for equipment procurement, partially offsetting low consumer purchasing power. North America and South America are experiencing moderate growth. The United States is preparing to host the 2026 World Cup, while Brazil's SAF model is unlocking commercialization opportunities through private club investments. However, Argentina's resistance to privatization, as courts blocked President Milei's decree, creates regulatory uncertainty that could delay institutional investments.

- Adidas AG

- Nike Inc.

- Puma SE

- Wilson Sporting Goods Co.

- Select Sport A/S

- Decathlon S.A.

- Mitre Sports International

- Baden Sports Inc.

- Molten Corporation

- Umbro (Iconix Brand Group)

- Under Armour Inc.

- Mizuno Corporation

- Uhlsport GmbH

- ASICS Corporation

- Joma Sport S.A.

- Anta Sports Products Ltd.

- Diadora S.p.A.

- Spalding (Russell Brands)

- New Balance Athletics Inc.

- BasicNet S.p.A. (Kappa)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising popularity of football as a global sport

- 4.2.2 Growth of professional leagues and competitions

- 4.2.3 Technological advancements in football manufacturing

- 4.2.4 Rising sponsorships and partnerships from brands

- 4.2.5 Expansion of football merchandise and licensing

- 4.2.6 Development of youth and grassroots football programs

- 4.3 Market Restraints

- 4.3.1 Growing popularity of online gaming

- 4.3.2 High equipment and infrastructure costs limit accessibility

- 4.3.3 Availability of counterfeit products

- 4.3.4 Economic volatility and inflation impact sponsorship budgets

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Size

- 5.1.1 Size 1 and 2

- 5.1.2 Size 3

- 5.1.3 Size 4

- 5.1.4 Size 5

- 5.2 By Category

- 5.2.1 Mass

- 5.2.2 Premium

- 5.3 By End Use

- 5.3.1 Personal

- 5.3.2 Commercial

- 5.4 By Distribution Channel

- 5.4.1 Online Stores

- 5.4.2 Offline Stores

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Colombia

- 5.5.2.4 Chile

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Sweden

- 5.5.3.8 Belgium

- 5.5.3.9 Poland

- 5.5.3.10 Netherlands

- 5.5.3.11 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 Thailand

- 5.5.4.5 Singapore

- 5.5.4.6 Indonesia

- 5.5.4.7 South Korea

- 5.5.4.8 Australia

- 5.5.4.9 New Zealand

- 5.5.4.10 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Adidas AG

- 6.4.2 Nike Inc.

- 6.4.3 Puma SE

- 6.4.4 Wilson Sporting Goods Co.

- 6.4.5 Select Sport A/S

- 6.4.6 Decathlon S.A.

- 6.4.7 Mitre Sports International

- 6.4.8 Baden Sports Inc.

- 6.4.9 Molten Corporation

- 6.4.10 Umbro (Iconix Brand Group)

- 6.4.11 Under Armour Inc.

- 6.4.12 Mizuno Corporation

- 6.4.13 Uhlsport GmbH

- 6.4.14 ASICS Corporation

- 6.4.15 Joma Sport S.A.

- 6.4.16 Anta Sports Products Ltd.

- 6.4.17 Diadora S.p.A.

- 6.4.18 Spalding (Russell Brands)

- 6.4.19 New Balance Athletics Inc.

- 6.4.20 BasicNet S.p.A. (Kappa)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK