PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043869

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043869

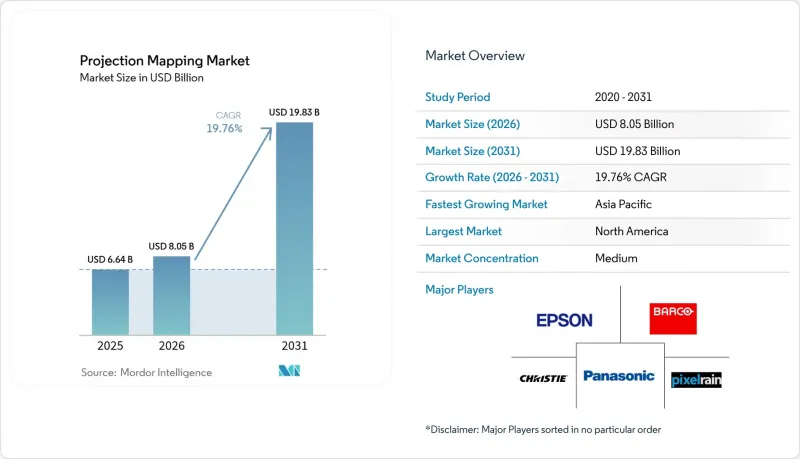

Projection Mapping - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The projection mapping market size is projected to expand from USD 6.64 billion in 2025 and USD 8.05 billion in 2026 to USD 19.83 billion by 2031, registering a CAGR of 19.76% between 2026 to 2031.

Widespread adoption of high-brightness laser projectors, falling cost-per-lumen metrics, and real-time generative-AI content workflows are accelerating deployments across civic landmarks, theme parks, and retail flagships. Municipal smart-city programs in Japan, Saudi Arabia, and the UAE are reclassifying projection mapping as permanent infrastructure, assured of predictable tourism dividends and lower on-site labor enabled by camera-based auto-calibration. Brands are reallocating advertising budgets toward immersive facade takeovers that deliver social-media amplification ratios exceeding 15:1, outpacing static LED in narrative depth and memorability. Hardware vendors now bundle cloud content platforms that monitor uptime and energy consumption, creating recurring service revenue and reducing projector downtime by up to 50%.

Global Projection Mapping Market Trends and Insights

Immersive Advertising And Live-Event Experiences

Brands are shifting spend from static billboards to facade takeovers that generate superior engagement metrics and large volumes of user-generated social content. Coca-Cola's Piccadilly Lights activation and Adidas's Oxford Street wrap proved that storytelling across complex surfaces matches LED cost-per-impression while delivering cinematic depth. Theme parks duplicate the approach; Universal Orlando Resort's CineSational show extended average guest dwell time by 22 minutes, directly lifting food-and-beverage sales. Stadium corridors now feature interactive projections that convert circulation space into sponsorable media, while free-admission festivals in Japan demonstrate sponsorship-led monetization models. Permanent installations benefit from lower per-event setup costs, improving ROI over multiyear cycles.

High-Brightness Laser Projectors Adoption

RGB laser engines exceeding 25,000 lumens provide 20,000-hour lifespans, slashing maintenance visits and enabling unmanned rooftop arrays. Panasonic's PT-RQ50K series covers 13,905 square meters on the Tokyo Metropolitan Government Building and operates nightly without on-site staff. Christie Digital deploys 45,000-lumen models in arenas where daylight readability was once impossible with lamp-based units. The laser price premium has narrowed to 1.8X, and total cost of ownership now favors laser in five-year models. Middle East megaprojects specify laser-only procurement to contain ten-year service budgets.

High Up-Front Installation And Content Costs

A permanent civic installation on a 2,500-square-meter facade demands USD 0.8-1.5 million, restricting adoption to municipalities, Fortune 500 brands, and tier-1 museums. Rental deployments cost less but suffer 70-80% idle time, eroding fleet margins. Content creation stays labor-intensive; a 10-minute show can incur USD 40,000-80,000 in creative fees each year. Financing models such as equipment-as-a-service and tourism-tax bonds remain confined to North America and Western Europe. Lack of standardized ROI benchmarks further slows budget approvals in price-sensitive regions.

Other drivers and restraints analyzed in the detailed report include:

- Smart-City Landmark Illumination Programs

- Real-Time Generative-AI Content Workflows

- Complex Site-Specific Calibration Delays

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware accounted for 61.83% of 2025 revenue, reflecting the capital-intensive nature of projectors, lenses, and media servers. Software, however, is rising at a 21.11% CAGR because cloud platforms cut on-site labor and enable real-time playlist updates. Subscription licensing converts one-time sales into predictable annuities while remote diagnostics slash downtime. Disguise, Dataton, and Panasonic's AcroSign now ship bundled analytics dashboards that monitor brightness drift and power draw, helping venues meet ISO 50001 reporting requirements. Competing cloud suites integrate audience heat-mapping, offering venues monetizable data packages for sponsors. As most projector OEMs now preload calibration tools, software lock-in is shifting pricing power toward platform owners.

Over the forecast window, many mid-sized museums will forgo outright projector ownership, instead renting hardware while investing in perpetual cloud software seats. That pivot will raise software's share of the projection mapping market to levels last seen in digital signage, mirroring the SaaS transition previously observed in broadcast graphics. Platforms embedding generative AI are expected to command premium fees, further widening the revenue gap between code and metal.

3D installations held 55.72% of 2025 spending, yet audiences now seek multisensory immersion that smartphones cannot replicate. Venues bundling haptics, fragrance diffusion, and synchronized drones with projection mapping routinely charge night-time visitor premiums of USD 30-50. Such 4D formats, growing at a 20.82% CAGR, bolster guest stay times and ancillary spend on retail and food. Museums leverage 2D overlays for cost-sensitive educational exhibits, but AI depth-estimation plugins are turning legacy 2D libraries into quasi-3D content, extending the life of assets.

Because immersive attractions discourage casual recording, operators protect intellectual property and minimize free online leaks. That exclusivity sustains higher average ticket values, ensuring 4D will capture incremental share of the projection mapping market size by 2031. Although safety regulations in heritage districts limit pyrotechnics, most 4D effects, such as wind jets and scent, comply when properly documented, easingan permitting.

The Projection Mapping Market Report is Segmented by Offering (Hardware, and Software), Dimension (2D, 3D, and More), Brightness Class (Less Than 10, 000 Lm and More), Projection Technology (DLP, LCD, and More), Mapping Surface (Building Facades, Indoor Walls and Floors, and More), Application (Large Venues and Facades, Events and Festivals, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific leads growth with a 21.66% CAGR as Japan institutionalizes projection mapping within urban policy, and the Middle East funds mega-installations through sovereign programs that bundle fiber backhaul and GPU edge nodes. North America, while still the largest revenue contributor in 2025, is transitioning from new hardware rollouts toward content refresh cycles, stabilizing growth at mid-single-digit rates.

Europe maintains steady adoption anchored in heritage tourism, yet EU Directive 2024/1619 imposes brightness caps and operating-hour limits that lengthen permitting timelines. Municipal pilots in Barcelona and Amsterdam nonetheless demonstrate that adaptive-dimming algorithms can comply with regulations while maintaining visitor flow.

Emerging opportunities arise in India, South Korea, and Southeast Asia, where declining projector prices intersect with heritage-tourism initiatives. South America and Africa lag due to budget constraints and a scarcity of integrators, though World Cup legacy infrastructure in Brazil and archaeological showcases in Egypt hint at future uptake once financing tools mature.

- Panasonic Corporation

- Seiko Epson Corporation

- Barco NV

- Christie Digital Systems USA, Inc.

- BenQ Corporation (Qisda)

- ViewSonic Corporation

- Vivitek (Delta Electronics)

- NEC Display Solutions (Sharp)

- Disguise Technologies Limited

- Dataton AB

- HeavyM (Digital Essence SAS)

- Green Hippo Ltd

- Resolume BV

- Blackmagic Design Pty Ltd

- Avolites Ltd

- GarageCube SA (MadMapper)

- Pixel Rain Digital

- Digital Projection Ltd

- Optoma Europe Limited (Coretronic)

- Sony Corporation

- LG Electronics Inc.

- Lightform Inc.

- Lumitrix s.r.o.

- Vioso GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Immersive Advertising and Live-Event Experiences

- 4.2.2 High-Brightness Laser Projectors Adoption

- 4.2.3 Smart-City Landmark Illumination Programs

- 4.2.4 Declining Cost-Per-Lumen from RGB Laser Engines

- 4.2.5 Real-Time Generative-AI Content Workflows

- 4.2.6 XR Stage Demand for Complementary Mapping

- 4.3 Market Restraints

- 4.3.1 High Up-Front Installation and Content Costs

- 4.3.2 Complex Site-Specific Calibration Delays

- 4.3.3 Light-Pollution / Heritage-Facade Regulation

- 4.3.4 Laser-Diode Supply-Chain Volatility

- 4.4 Value Chain Analysis

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitutes

- 4.6.5 Degree of Competition

- 4.7 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Offering

- 5.1.1 Hardware

- 5.1.2 Software

- 5.2 By Dimension

- 5.2.1 2D

- 5.2.2 3D

- 5.2.3 4D / Immersive

- 5.3 By Brightness Class (ANSI lm)

- 5.3.1 Less Than 10,000 lm

- 5.3.2 10,000 - 25,000 lm

- 5.3.3 Greater Than 25,000 lm

- 5.4 By Projection Technology

- 5.4.1 DLP

- 5.4.2 LCD

- 5.4.3 LCoS and Others

- 5.5 By Mapping Surface

- 5.5.1 Building Facades

- 5.5.2 Indoor Walls and Floors

- 5.5.3 Objects and Products

- 5.5.4 Water Screens and Natural Terrain

- 5.6 By Application

- 5.6.1 Large Venues and Facades

- 5.6.2 Events and Festivals

- 5.6.3 Theme Parks and Attractions

- 5.6.4 Sports Arenas and Stadiums

- 5.6.5 Cultural and Heritage Sites

- 5.6.6 Commercial Spaces (Retail, Corporate, Education)

- 5.6.7 Other Application

- 5.7 By Geography

- 5.7.1 North America

- 5.7.1.1 United States

- 5.7.1.2 Canada

- 5.7.1.3 Mexico

- 5.7.2 South America

- 5.7.2.1 Brazil

- 5.7.2.2 Argentina

- 5.7.2.3 Rest of South America

- 5.7.3 Europe

- 5.7.3.1 Germany

- 5.7.3.2 France

- 5.7.3.3 United Kingdom

- 5.7.3.4 Italy

- 5.7.3.5 Rest of Europe

- 5.7.4 Asia-Pacific

- 5.7.4.1 China

- 5.7.4.2 Japan

- 5.7.4.3 South Korea

- 5.7.4.4 India

- 5.7.4.5 Rest of Asia-Pacific

- 5.7.5 Middle East

- 5.7.5.1 Saudi Arabia

- 5.7.5.2 United Arab Emirates

- 5.7.5.3 Rest of Middle East

- 5.7.6 Africa

- 5.7.6.1 South Africa

- 5.7.6.2 Egypt

- 5.7.6.3 Rest of Africa

- 5.7.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-Level Overview, Market-Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Panasonic Corporation

- 6.4.2 Seiko Epson Corporation

- 6.4.3 Barco NV

- 6.4.4 Christie Digital Systems USA, Inc.

- 6.4.5 BenQ Corporation (Qisda)

- 6.4.6 ViewSonic Corporation

- 6.4.7 Vivitek (Delta Electronics)

- 6.4.8 NEC Display Solutions (Sharp)

- 6.4.9 Disguise Technologies Limited

- 6.4.10 Dataton AB

- 6.4.11 HeavyM (Digital Essence SAS)

- 6.4.12 Green Hippo Ltd

- 6.4.13 Resolume BV

- 6.4.14 Blackmagic Design Pty Ltd

- 6.4.15 Avolites Ltd

- 6.4.16 GarageCube SA (MadMapper)

- 6.4.17 Pixel Rain Digital

- 6.4.18 Digital Projection Ltd

- 6.4.19 Optoma Europe Limited (Coretronic)

- 6.4.20 Sony Corporation

- 6.4.21 LG Electronics Inc.

- 6.4.22 Lightform Inc.

- 6.4.23 Lumitrix s.r.o.

- 6.4.24 Vioso GmbH

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment