PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043870

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043870

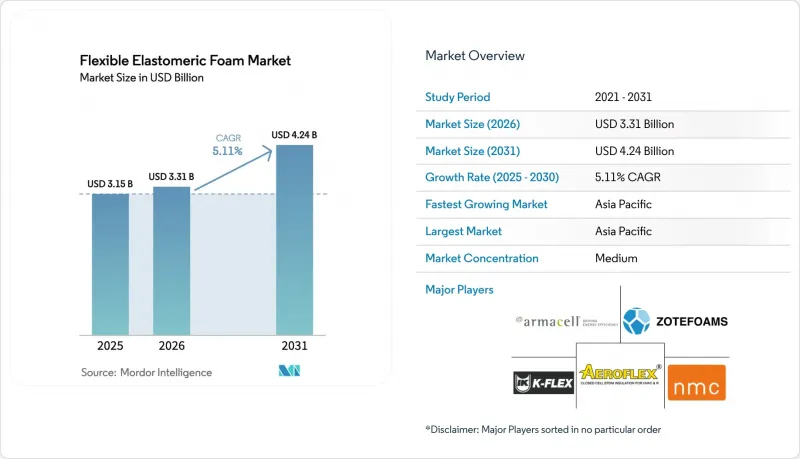

Flexible Elastomeric Foam - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Flexible Elastomeric Foam Market size was valued at USD 3.15 billion in 2025 and is estimated to grow from USD 3.31 billion in 2026 to reach USD 4.24 billion by 2031, at a CAGR of 5.11% during the forecast period (2026-2031).

In the Asia-Pacific region, a surge in building-energy regulations, ongoing retrofits in HVAC and refrigeration, and a swift expansion of cold-chain projects are collectively driving up baseline demand. As regulators phase down high-GWP refrigerants, equipment replacements are occurring sooner than anticipated. Each transition from R-410A to the higher-pressure R-32 or R-454B chillers requires thicker, lower-permeability pipe insulation. This shift is significantly expanding the market for flexible elastomeric foam. Additionally, with supply-chain pressures on butadiene and neoprene, converters are increasingly turning to EPDM. This shift not only diversifies the material mix but also drives innovation in fire-safe, halogen-free, and low-carbon foams. Suppliers that integrate back into aerogel, biomass-balance, and super-critical CO2 foaming are gaining a competitive edge, especially as customers demand evidence of embodied-carbon reduction.

Global Flexible Elastomeric Foam Market Trends and Insights

Increasing Retrofitting Activities in HVAC and Refrigeration Systems

Owners of commercial HVAC equipment, facing mandatory deadlines for leak repairs or phase-outs, are opting to replace entire systems sooner than anticipated. As the industry transitions from R-410A to R-32 and R-454B, discharge pressures have surged. Closed-cell elastomeric foam stands out as one of the few insulation materials capable of managing this increased condensation risk. The demand for this insulation is further bolstered by provincial subsidies in China promoting R-290 conversions, along with incentives for such transitions in public-sector buildings across Europe. Armacell's Advanced Insulation division, which underscores this trend, reported robust revenue growth, highlighting the impact of retrofit-driven demand. Supermarkets making the switch to CO2 transcritical racks are now procuring foam rated for temperatures as low as -40°C, broadening their product selection from NBR/PVC to also encompass EPDM and chloroprene.

Implementation of F-Gas Phase-Down Compliance Deadlines

By 2030, the European Union is set to reduce its HFC quotas, with key checkpoints in 2027 and 2029. This move is hastening chiller-replacement cycles. Building owners face a choice: retrofit with drop-ins that still necessitate new insulation or transition to natural-refrigerant systems, which require a thicker wrap. Both options are driving a surge in near-term procurement. Similarly, Japan's expedited Kigali timeline and South Korea's enforced refrigerant reclamation are echoing this trend, pulling demand forward at least until 2027. Distributors throughout the EU are noting that orders for products in the flexible elastomeric foam market are booked out for six months, signaling a likely tight supply in 2026.

Butadiene and Neoprene Feedstock Volatility

By early 2025, steam-cracker outages and rising naphtha costs significantly increased butadiene spot prices in the Asia-Pacific, directly influencing NBR cost curves. At the same time, a shutdown at DuPont's LaPlace facility tightened the global neoprene supply, leading to a surge in North American prices. As margins narrowed, many converters shifted to EPDM, benefiting from its more stable ethylene and propylene streams. While this transition helps avoid price surges, it requires qualification testing with end users, temporarily delaying shipment cycles.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Building Energy-Efficiency Regulations

- Rapid Growth of Cold-Chain Infrastructure for Last-Mile Grocery Delivery

- Fire-Safety Bans on Halogenated Additives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, thermal insulation accounted for 75.22% of the demand and is projected to grow at a CAGR of 5.29% during the forecast period of 2026-2031. This growth is primarily driven by the increasing demand for electric-vehicle battery housings and rail rolling stock, which require vibration dampening in the 500 Hz to 2 kHz range. The market share of flexible elastomeric foam in thermal applications is supported by a mandatory wrap requirement, as stipulated by U.S. and European energy codes. In contrast, its use in acoustic applications is influenced more by voluntary Leadership in Energy and Environmental Design (LEED) credits and tenant expectations.

Thermal applications are also benefiting from refrigerant transitions that necessitate thicker insulation. Meanwhile, the acoustic segment gains an advantage as companies emphasize sound transmission loss without compromising flexibility. With the expansion of electric vehicle platforms and emerging vibration challenges from data-center pumps, acoustic foam is poised for growth. However, thermal insulation is expected to maintain its lead in absolute revenues through 2031.

The Flexible Elastomeric Foam Market Report is Segmented by Function (Thermal Insulation, and Acoustic Insulation), Type (Natural Rubber/Latex, Nitrile Butadiene Rubber/Polyvinyl Chloride, Ethylene Propylene Diene Monomer, and More), Application (HVAC, Automotive, Transportation, and More), and Geography (Asia-Pacific, North America, Europe, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region accounted for 45.25% of total revenue. With India doubling its cold-storage capacity and China rolling out an extensive HVAC retrofit pipeline, the region is poised for a robust 7.09% CAGR during the forecast period of 2026-2031. Armacell has set up a new aerogel facility in Pune, while local players such as Huamei are optimizing their operations by leveraging localized supplies and aligning with industry codes.

In North America, leak-repair regulations that came into effect in January 2026, coupled with stringent envelope codes in California and New York, are driving the market. Consequently, distributors have bolstered their order books into late 2026, capitalizing on pre-buying opportunities. Europe's market growth is spurred by the F-Gas phase-down, which is accelerating the replacement of chillers and heat pumps. In response to high labor costs, markets are increasingly adopting pre-formed pipe sections to reduce installation time, a trend addressed by companies such as Hira Industries and K-Flex.

Although South America and the Middle-East and Africa hold a smaller share of global revenue, they are experiencing double-digit growth. This surge is largely fueled by the demands of pharmaceutical logistics and grocery deliveries in regions grappling with sweltering temperatures surpassing 45 degrees Celsius. Additionally, policy moves in Japan and South Korea are set to reshape the landscape by aiming to reclaim refrigerants and banning the import of virgin R-410A by 2027. Such initiatives position Northeast Asia on a rapid growth trajectory, mirroring Europe's ascent, ensuring the region remains buoyant even as the construction sector cools.

- Aeroflex USA, Inc.

- Armacell International S.A.

- BASF

- DuPont

- Era Polymers Pty Ltd

- Hira Industries LLC

- Huamei Energy-saving Technology Group Co., Ltd.

- Intec Foams Ltd

- Jinan Retek Industries Inc.

- Johns Manville (Berkshire Hathaway)

- Kingwell World Industries Inc.

- L'Isolante K-FLEX S.p.A.

- NMC SA

- Owens Corning

- Rogers Corporation

- Rubberlite, Inc.

- Saint-Gobain

- Sekisui Chemical Co., Ltd.

- Trelleborg AB

- Zotefoams plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing retrofitting activities in HVAC and refrigeration systems

- 4.2.2 Implementation of F-Gas phase-down compliance deadlines

- 4.2.3 Tightening building energy-efficiency regulations

- 4.2.4 Rapid growth of cold-chain infrastructure for last-mile grocery delivery

- 4.2.5 Rising adoption of high-temperature foam in solar-thermal collectors

- 4.3 Market Restraints

- 4.3.1 Butadiene and neoprene feedstock volatility

- 4.3.2 Fire-safety bans on halogenated additives

- 4.3.3 PFAS-linked blowing-agent supply risk

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Function

- 5.1.1 Thermal Insulation

- 5.1.2 Acoustic Insulation

- 5.2 By Type

- 5.2.1 Natural Rubber/Latex

- 5.2.2 Nitrile Butadiene Rubber/Polyvinyl Chloride

- 5.2.3 Ethylene Propylene Diene Monomer

- 5.2.4 Chloroprene

- 5.2.5 Other Types (ECO, SBR, etc.)

- 5.3 By Application

- 5.3.1 HVAC

- 5.3.2 Automotive

- 5.3.3 Transportation

- 5.3.4 Solar Installations

- 5.3.5 Refrigeration Systems

- 5.3.6 Other Applications (Medical and Healthcare Devices, etc.)

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 Aeroflex USA, Inc.

- 6.4.2 Armacell International S.A.

- 6.4.3 BASF

- 6.4.4 DuPont

- 6.4.5 Era Polymers Pty Ltd

- 6.4.6 Hira Industries LLC

- 6.4.7 Huamei Energy-saving Technology Group Co., Ltd.

- 6.4.8 Intec Foams Ltd

- 6.4.9 Jinan Retek Industries Inc.

- 6.4.10 Johns Manville (Berkshire Hathaway)

- 6.4.11 Kingwell World Industries Inc.

- 6.4.12 L'Isolante K-FLEX S.p.A.

- 6.4.13 NMC SA

- 6.4.14 Owens Corning

- 6.4.15 Rogers Corporation

- 6.4.16 Rubberlite, Inc.

- 6.4.17 Saint-Gobain

- 6.4.18 Sekisui Chemical Co., Ltd.

- 6.4.19 Trelleborg AB

- 6.4.20 Zotefoams plc

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

- 7.2 Flexible elastomeric foam adoption in hyperscale data-centres