PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043873

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043873

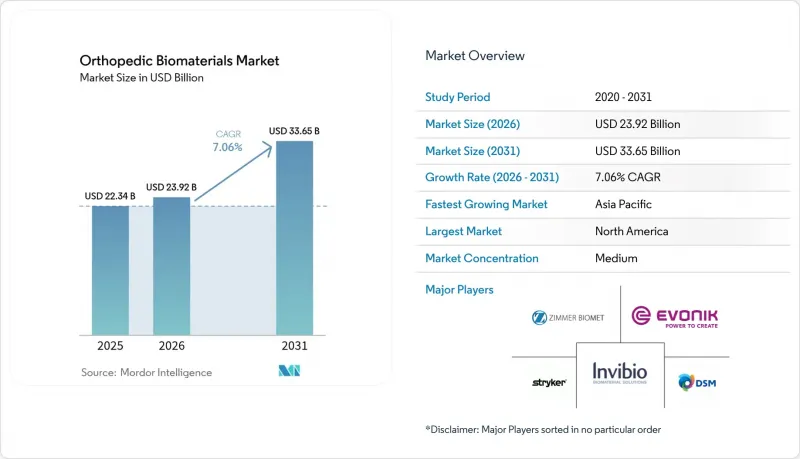

Orthopedic Biomaterials - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

Orthopedic Biomaterials market size in 2026 is estimated at USD 23.92 billion, growing from 2025 value of USD 22.34 billion with 2031 projections showing USD 33.65 billion, growing at 7.06% CAGR over 2026-2031.

Growth stems from a confluence of demographic aging, surging osteoarthritis prevalence, steady sports- and traffic-injury incidence, and rapid technological progress in patient-specific and bioactive implants. Regulatory catalysts such as the U.S. FDA's breakthrough device program shorten launch timelines for novel biomimetic materials , while hospital demand for post-pandemic backlog reduction sustains procedural volumes. Companies leverage additive manufacturing to deliver fit-for-purpose components that reduce revision risk, and sustainability mandates push the supply base toward biodegradable formulations. Persistent supply chain stresses and tighter reimbursement scrutiny temper, but do not derail, the forward trajectory of the orthopedic biomaterials market.

Global Orthopedic Biomaterials Market Trends and Insights

Ageing-Linked Osteoarthritis Burden

Global life expectancy gains intersect with lifestyle factors to lift osteoarthritis prevalence, creating enduring demand for joint reconstruction solutions. Nearly 50% of post-menopausal women are expected to develop the condition by 2045, and knee osteoarthritis cases could rise 75% by 2050 . Parallel growth in revision hip and knee arthroplasty volumes amplifies requirements for durable, wear-resistant biomaterials. Elevated body-mass index contributes to more than 20% of global cases, coupling metabolic stress with mechanical wear and accelerating formulation of high-strength, low-debris polymers that extend implant longevity.

Sports & Road-Injury Up-Trend in Emerging Markets

Urbanization and motorization raise musculoskeletal trauma incidence across many lower-income regions. In Kenyan hospitals, road accidents account for 59.4% of orthopedic admissions, with 85% of victims in the 15-64 age bracket . Comparable patterns in Ghana show vehicular crashes comprising 42% of injuries. Rising elective sports participation also expands reconstruction volumes among younger patients, prompting suppliers to tailor polymer-ceramic composites that balance mechanical resilience with accelerated bone in-growth.

Procedure Down-Coding & Reimbursement Erosion

Payers tighten documentation demands, forcing hospitals to justify every orthopedic indication. Medicare now requires proof of failed conservative care before authorizing total knees, extending pre-operative timelines. Payment bands fluctuate widely; complex trauma reimbursements range from USD 9,496 to USD 50,639 under MS-DRG codes, adding budgeting uncertainty for providers. Device firms must therefore demonstrate cost-offset claims and supply evidence dossiers to maintain coder compliance.

Other drivers and restraints analyzed in the detailed report include:

- 3-D Printed Patient-Specific Implants Adoption

- Rapid FDA Breakthrough Device Designations for Biomimetic Materials

- Post-Implant Infection Litigations Increasing Insurer Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-performance polymers generated the largest revenue slice in 2025, reflecting 46.58% share, anchored by strong uptake in acetabular cups and spinal cages. Evonik's VESTAKEEP Fusion illustrates how adding biphasic calcium phosphate turns PEEK bioactive without sacrificing mechanical strength. The orthopedic biomaterials market size for polymers is projected to expand steadily as surface-enhanced variants tackle historical osseointegration limits. Ceramics and bioactive glasses, while smaller today, post a brisk 7.82% CAGR through 2031 as surgeons capitalize on innate osteoconductivity and radiolucency. Hybrid designs that bond polymer cores to ceramic coatings blend load tolerance with bone affinity, marking a shift toward materials that participate in healing rather than merely occupy space.

The metals category faces renewed scrutiny tied to stress shielding and nickel hypersensitivity. Zimmer Biomet's Tivanium alloy targets allergy mitigation with low-nickel chemistry. Niche disruptors such as silicon nitride pursue antibacterial surfaces and thermal stability, with Sintx claiming sole FDA-cleared status for the compound. Calcium-phosphate cements retain hospital favor for moldable bone void fillers, yet ongoing research into controlled-resorption magnesium alloys foreshadows future movement toward fully degradable load-sharing constructs.

Joint reconstruction retained 38.25% revenue in 2025 as hip and knee arthroplasty volumes remained high among aging populations. Nonetheless, orthobiologics outpace all other uses with an 8.03% CAGR, propelled by evidence that bioinductive patches such as Smith+Nephew's REGENETEN cut rotator-cuff re-tear rates 68% versus conventional repair. The orthopedic biomaterials market size attributed to biologics is set to widen as payers warm to regeneration that delays or avoids replacement surgery.

Spinal and trauma fixation implants continue reliable growth thanks to rising high-energy impacts in emerging economies. Viscosupplementation, once confined to mild osteoarthritis, is being repositioned as an adjunct to postpone arthroplasty among active seniors. Convergence arises as hardware manufacturers embed growth factors within plates or nails, creating integrated constructs that stabilize fractures while stimulating callus formation.

The Orthopedic Biomaterials Market Report is Segmented by Material Type (High-Performance Polymers, Ceramics and Bioactive Glasses, and More), Application (Orthobiologics, Joint Reconstruction, and More), Biodegradability (Non-Biodegradable Biomaterials, Biodegradable Biomaterials), Condition (Osteoarthritis, Osteoporosis, and More), and Geography (North America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 39.90% of 2025 revenue, anchored by advanced surgical robotics and comprehensive insurance cover. The orthopedic biomaterials market benefits from technology showcases such as the VELYS robotic knee and KINCISE 2 automated hip system that refine component alignment. Yet payer documentation tightening and raw-material supply warnings issued by the FDA underscore profit-margin pressure. Hospital groups increasingly weigh device selection on lifetime value metrics, encouraging vendors to present cost-in-use evidence alongside clinical data.

Asia-Pacific posters an 7.98% CAGR to 2031 on the back of rapid aging and expanding middle-class insurance coverage. Domestic manufacturers scale additive manufacturing labs to cut import reliance, while governments streamline approval pathways for 3-D printed implants. Markets such as India roll out price ceilings to widen access, pushing multinationals to localize production and adjust channel strategies. Country-level diversity remains high, with Japan's mature regulatory oversight contrasting with evolving frameworks in fast-growing Southeast Asian nations.

Europe grows steadily through 2030 as the EU Medical Device Regulation tightens traceability and accelerates eco-design mandates. Hospitals pilot cradle-to-grave tracking of orthopedic components, paving the way for higher biodegradable uptake. Middle East & Africa endorse public-private collaborations to raise theater capacity; the GCC alone spends USD 43.9 billion annually on medical devices. Latin America fosters clinical-trial tourism; Chile hosted 33 orthopedic device studies in 2023, up from 20 in 2021. Local manufacturing incentives in Brazil aim to narrow price gaps between imported and domestic knee implants, supporting regional supplier emergence.

List of Companies Covered in this Report:

- Stryker

- Zimmer Biomet

- Johnson & Johnson

- Smiths Group

- Medtronic

- Globus Medical

- Exactech

- Invibio (Victrex)

- Evonik Industries

- Mitsubishi Chemical Advanced Materials

- Cam Bioceramics

- Kyocera Medical

- BASF Biomaterials

- Heraeus Medical

- Orthofix

- Conmed

- Wright Medical (Stryker)

- NuVasive

- LimaCorporate

- CeramTec

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Ageing?Linked Osteoarthritis Burden

- 4.2.2 Sports & Road-Injury Up-Trend in Emerging Markets

- 4.2.3 3-D Printed Patient-Specific Implants Adoption

- 4.2.4 Rapid FDA Breakthrough Device Designations for Biomimetic Materials

- 4.2.5 Hospital PPP Tenders in LATAM & MENA Favouring Local Biomaterials Sourcing

- 4.2.6 Circular-Economy Push for Bio-Resorbable Materials

- 4.3 Market Restraints

- 4.3.1 Procedure Down-Coding & Reimbursement Erosion

- 4.3.2 Post-Implant Infection Litigations Increasing Insurer Scrutiny

- 4.3.3 Raw-Material Supply Volatility

- 4.3.4 Talent Shortage in Orthobiologic R&D Labs

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porters Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Material Type

- 5.1.1 High-Performance Polymers

- 5.1.2 Ceramics and Bioactive Glasses

- 5.1.3 Calcium-Phosphate Cements

- 5.1.4 Metals and Metal Alloys

- 5.1.5 Others

- 5.2 By Application

- 5.2.1 Orthobiologics

- 5.2.2 Joint Reconstruction

- 5.2.3 Viscosupplementation

- 5.2.4 Spinal and Trauma Fixation Implants

- 5.2.5 Others

- 5.3 By Biodegradability

- 5.3.1 Non-Biodregradable Biomaterials

- 5.3.2 Biodegradable Biomaterials

- 5.4 By Condition

- 5.4.1 Osteoarthritis

- 5.4.2 Osteoporosis

- 5.4.3 Bone Tumors

- 5.4.4 Rheumatoid Arthritis

- 5.4.5 Trauma Management

- 5.4.6 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, Recent Developments)

- 6.3.1 Stryker

- 6.3.2 Zimmer Biomet

- 6.3.3 Johnson and Johnson

- 6.3.4 Smith & Nephew

- 6.3.5 Medtronic

- 6.3.6 Globus Medical

- 6.3.7 Exactech

- 6.3.8 Invibio (Victrex)

- 6.3.9 Evonik Industries

- 6.3.10 Mitsubishi Chemical Advanced Materials

- 6.3.11 Cam Bioceramics

- 6.3.12 Kyocera Medical

- 6.3.13 BASF Biomaterials

- 6.3.14 Heraeus Medical

- 6.3.15 Orthofix

- 6.3.16 ConMed

- 6.3.17 Wright Medical (Stryker)

- 6.3.18 NuVasive

- 6.3.19 LimaCorporate

- 6.3.20 CeramTec

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment