PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043886

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043886

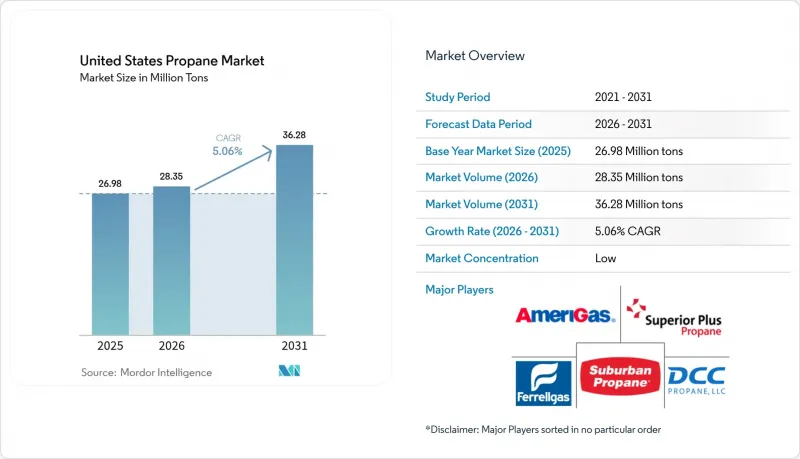

United States Propane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The United States Propane Market size is projected to expand from 26.98 million tons in 2025 and 28.35 million tons in 2026 to 36.28 million tons by 2031, registering a CAGR of 5.06% between 2026 to 2031.

Fleet conversions are gaining momentum, driven by expanding propane dehydrogenation (PDH) capacities and robust standby-power deployments. These developments are shifting volumes away from a traditionally weather-dependent residential base and toward transportation and petrochemical applications. By 2025, natural-gas processing accounted for the majority of the total volume. However, renewable propane has been making significant progress. This growth is largely attributed to California's Low Carbon Fuel Standard (LCFS) credits, which have transformed the economics of sourcing. The demand for motor fuel has been rising, driven by conversions in school buses and last-mile deliveries. These transitions are resulting in notable savings in fuel costs compared to diesel, all while adhering to stricter NOx emissions limits. Investments in PDH facilities along the Gulf Coast have created a structural pull for feedstock, providing insulation from seasonal heating fluctuations. On another front, IoT-enabled "Propane-as-a-Service" models are revolutionizing the distribution landscape. By reducing distributor truck rolls and boosting customer retention, these models are empowering large retailers to maintain their foothold in an otherwise fragmented market.

United States Propane Market Trends and Insights

Autogas Fleet Conversions Accelerate as Diesel Rules Tighten

School districts are utilizing Clean School Bus Program grants to replace diesel units. By securing propane at a cost lower than diesel, they achieve paybacks in just a few years. Propane direct-injection engines, with their impressive horsepower, not only replicate diesel torque but also significantly reduce NOx emissions. Blue Bird's 7.3-liter platform and Cummins' B6.7 Propane are advancing this technology into Class 6-7 delivery fleets, targeting a market of hundreds of thousands of vehicles. Fleet operators are experiencing substantial fuel savings, and telematics confirm steady performance with annual duty cycles achieving impressive mileage. As more metropolitan areas adopt low-emission zones, the lower capital requirement of propane - compared to battery-electric systems - is accelerating conversions, a trend projected to persist during the forecast period of 2026-2031

Petrochemical PDH Capacity Additions Lock In Feedstock Demand

Enterprise Products Partners' PDH 2, which processes a substantial daily volume of propane, produces polymer-grade propylene. By 2028, LyondellBasell's Channelview expansion will add to this capacity. With PDH units now commanding a significant portion of petrochemical propane consumption, their demand has become decoupled from refinery operating rates. Meanwhile, newer fluid catalytic dehydrogenation (FCDh) designs, which come with lower capital costs, are driving capacity expansions, despite hurdles in ESG financing. Looking ahead, robust petrochemical demand during the forecast period of 2026-2031 is expected to bolster the United States propane market.

Price Volatility Compresses Distributor Margins

In 2024, warm weather and record NGL output caused a significant drop in Mont Belvieu spot prices, posing challenges for holders of fixed-price contracts. Throughout the year, exports surged, with barrels being redirected offshore due to attractive premiums in Asia. The basis risk between the Gulf and regional hubs often resulted in imperfect hedges. As a result, Suburban Propane experienced a decline in its fiscal-year gross margin per gallon, even with increased volumes.

Other drivers and restraints analyzed in the detailed report include:

- Stand-by Generator Installations Rise with Grid-Reliability Investments

- Propane-as-a-Service Subscription Models Boost Margins

- Rail and Pipeline Bottlenecks Elevate Logistics Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, natural-gas processing dominated the supply landscape, commanding a substantial 78.72% share. This was largely driven by fractionation activities at Mont Belvieu and robust outputs from the Permian's associated gas. Such processing dynamics fortify the U.S. propane market, even as contributions from refinery coproducts diminish. Although renewable propane currently holds a modest slice of the supply pie, it is on an impressive growth trajectory, boasting a 9.95% CAGR during the forecast period of 2026-2031. This surge is largely attributed to LCFS credits, carving out a lucrative niche that has piqued the interest of early adopters in the California-Oregon region. In this evolving U.S. propane landscape, traditional NGL extraction aligns with commodity demands, while pioneering low-carbon initiatives draw in credit-centric buyers.

Mergers and acquisitions underscore the escalating value of infrastructure: ONEOK's takeover of Magellan unified two powerhouses with substantial fractionation capabilities. In a bid to bolster export flexibility, Enterprise is methodically expanding its storage caverns. Even amidst ESG scrutiny, producers maintain an optimistic outlook on processing projects, buoyed by consistent demand from PDH and export markets. Renewable trailblazers, Neste and Oberon, are establishing compact facilities. By harnessing existing renewable-diesel or DME trains, they are exemplifying a strategic, modular approach to scaling low-carbon supplies.

The United States Propane Market Report is Segmented by Source (Natural Gas Processing, Crude Oil Refining, and Renewable), Application (Space and Water Heating, Cooking, Motor Fuel, Chemical Feedstock, Power Generation, and Other Applications), and End-User Industry (Residential, Commercial, Industrial, Transportation, Power Generation, and Other End-User Industries). The Market Forecasts are Provided in Terms of Volume (Tons).

List of Companies Covered in this Report:

- AmeriGas Propane, Inc.

- Blossman Gas

- CHS Inc.

- DCC Propane

- Energy Transfer LP

- Ferrellgas

- GROWMARK Inc.

- MFA Oil Company

- NGL Energy Partners LP

- Paraco

- Pinnacle

- Suburban Propane

- Superior Plus Propane

- ThompsonGas

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Autogas fleet conversions (school buses/delivery/municipal)

- 4.2.2 Petrochemical PDH capacity additions

- 4.2.3 Stand-by generator installations for grid resiliency

- 4.2.4 Propane-as-a-Service subscription models (IoT tank monitoring)

- 4.2.5 Off-grid microgrids for rural broadband towers

- 4.3 Market Restraints

- 4.3.1 Price volatility tied to NGL and crude markets

- 4.3.2 Rail/pipeline bottlenecks in key PADDs

- 4.3.3 ESG-driven divestment limiting upstream capex

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitute Products

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Volume)

- 5.1 By Source

- 5.1.1 Natural Gas Processing

- 5.1.2 Crude Oil Refining

- 5.1.3 Renewable Propane (Bio-Propane)

- 5.2 By Application

- 5.2.1 Space and Water Heating

- 5.2.2 Cooking

- 5.2.3 Motor Fuel

- 5.2.4 Chemical Feedstock

- 5.2.5 Power Generation

- 5.2.6 Other Applications

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Commercial

- 5.3.3 Industrial

- 5.3.4 Transportation

- 5.3.5 Power Generation

- 5.3.6 Other End-user Industries

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AmeriGas Propane, Inc.

- 6.4.2 Blossman Gas

- 6.4.3 CHS Inc.

- 6.4.4 DCC Propane

- 6.4.5 Energy Transfer LP

- 6.4.6 Ferrellgas

- 6.4.7 GROWMARK Inc.

- 6.4.8 MFA Oil Company

- 6.4.9 NGL Energy Partners LP

- 6.4.10 Paraco

- 6.4.11 Pinnacle

- 6.4.12 Suburban Propane

- 6.4.13 Superior Plus Propane

- 6.4.14 ThompsonGas

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment