PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043905

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043905

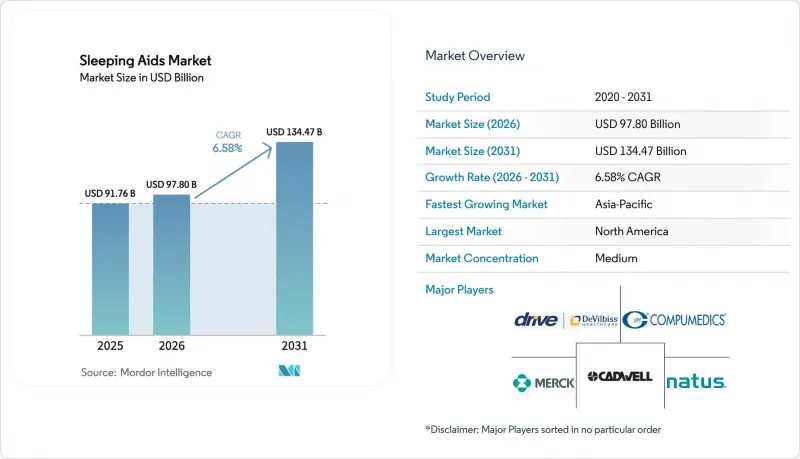

Sleeping Aids - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Sleeping Aids Market size is expected to increase from USD 91.76 billion in 2025 to USD 97.80 billion in 2026 and reach USD 134.47 billion by 2031, growing at a CAGR of 6.58% over 2026-2031.

Demand accelerates as global insomnia and sleep-breathing conditions affect nearly 2.5 billion people, especially among seniors whose insomnia rates are 40% higher than younger cohorts, prompting both pharmaceutical innovation and data-driven non-drug interventions. Corporate wellness programs, insurance reimbursement for PAP and oral devices, and an exploding smart-device ecosystem reinforce structural growth opportunities while venture investment fuels next-generation AI mattresses and wearables. Parallel restraint factors include safety concerns over prescription hypnotics, counterfeit supplements on e-commerce sites, and price sensitivity in emerging economies, yet these headwinds only partially offset strong demand catalysts.

Global Sleeping Aids Market Trends and Insights

Rising Incidence of Insomnia Among Aging Populations

An expanding cohort of adults aged 65 plus-set to double by 2030-elevates long-run demand in the sleeping aids market. Clinical data link poor sleep to 23% higher cardiovascular risk and 31% greater diabetes complications, pushing healthcare systems to fund preventive sleep programs. Pharmaceutical pipelines shift toward orexin-receptor antagonists that block wakefulness instead of inducing broad sedation, ensuring safer profiles for seniors. Parallel hardware innovation embeds temperature and posture sensors in smart mattresses to counter thermoregulation changes that disturb 78% of seniors. These converging medical and technology responses secure durable revenue streams for companies serving the sleeping aids market.

Growing Availability of OTC Melatonin & Natural Supplements

Melatonin supplement revenues are forecast to quintuple between 2022-2032, yet assays show deviations up to 478% between labeled and actual dosages, sparking regulatory alerts. Premium, third-party-tested formulations now command 40-60% price premiums, while herbal alternatives such as valerian and L-theanine gain traction among consumers seeking hormone-free options. In India, rising adoption of botanical sleep aids lifted prescription-volume for sleep-related products by 8% after COVID-19. This demand diversification adds incremental sales but also intensifies competition, compelling brands to emphasize transparency and clinical validation within the sleeping aids market.

Reported Side-Effects & Dependency Fears Over Prescription Drugs

Generic zolpidem variants now dominate scripts but face heightened scrutiny after reports of memory impairment and complex sleep behaviors. Physicians pivot to behavioral therapies such as CBT-I, while health insurers increasingly require non-drug trials before invasive procedures. Public awareness that melatonin offers limited help for chronic insomnia further erodes confidence in pharmacological fixes, nudging consumers toward tech-enabled solutions and fueling substitution effects inside the sleeping aids market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Smart-Sleep Technology Adoption (IoT Beds & Trackers)

- Corporate Wellness Programs Adding Sleep Solutions

- Patent Cliffs for Blockbuster Hypnotics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The mattresses & pillows segment retained 32.62% of the sleeping aids market share in 2025, driven by consumer loyalty to trusted comfort brands and aggressive omni-channel strategies. However, rising demand for AI-embedded beds propels average selling prices to USD 2,000-5,000, enhancing revenue despite slower unit growth. The smart sleep monitoring devices segment is projected to outpace all others at a 7.05% CAGR, underpinned by medical acceptance of remote-patient monitoring and seamless integration with mobile apps. Within the sleeping aids market size for connected devices, CPAP systems increasingly feature Bluetooth modules that upload compliance data to clinicians, boosting therapeutic outcomes and payer reimbursement rates. Hybrid innovations blur category lines-for example, mattress toppers that combine sleep tracking, thermal regulation, and massage-expanding addressable spend per household.

Traditional medications experience margin compression from generic rivalry, while supplements yield mixed results as efficacy scrutiny intensifies. The "other devices & accessories" niche benefits from this shift, with smart pillows and scent diffusers pairing with AI analytics to craft personalized sleep environments. Collectively, convergence across categories positions the sleeping aids market for multiproduct ecosystem sales that lift lifetime customer value and reduce churn.

The Sleeping Aids Market Report is Segmented by Product Type (Mattresses & Pillows, Sleep Apnea Devices, Medications, Supplements, Smart Sleep Monitoring Devices, Other Devices & Accessories), Sleep Disorder (Insomnia, Sleep Apnea, Restless Legs Syndrome, Narcolepsy, Others), End User (Residential, Medical, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America captured 41.85% of 2025 value thanks to advanced reimbursement systems, high disposable income, and a vibrant R&D ecosystem. The United States anchors growth through prolific smart-bed marketing and over 650 Sleep Number showrooms that maintain direct engagement. Canada leverages universal healthcare that reimburses sleep studies and CPAP devices, while Mexico's middle class spurs demand for entry-level foam mattresses. Market maturation, however, nudges leading brands to seek incremental growth overseas while upping service revenues at home.

Asia-Pacific posts the quickest 9.02% CAGR and is expected to overtake Europe before 2030. India illustrates unmet need: 93% of adults feel sleep-deprived and average 6.55 hours nightly, propelling sales of both herbal aids and connected devices. China's government health initiatives support large-scale screening, while Japan's aging society adopts tech-assisted bedding to counter insomnia linked to long work hours. South Korea's sleeping aids market size, estimated at KRW 1-1.5 trillion, exemplifies regional willingness to pay for premium foam pillows and anti-microbial bedding. Europe remains a steady contributor, buttressed by strict safety regulations that encourage clinically validated innovation. Northern European nations adopt smart beds fastest, whereas Southern Europe leans toward botanical supplements aligned with wellness lifestyles. South America and the Middle East & Africa show nascent potential; distributors partner with micro-finance providers to overcome price barriers and widen access to essential sleep products.

- Koninklijke Philips

- Resmed

- Tempur Sealy International Inc.

- GlaxoSmithKline

- Perrigo Company

- Merck

- Sanofi

- Sommetrics Inc.

- Itamar Medical Ltd.

- Drive DeVilbiss Healthcare

- Teva Pharmaceutical Industries

- Cadwell

- Natrol LLC

- Procter & Gamble

- Bayer

- Fitbit LLC (Google)

- Eight Sleep Inc.

- Casper Sleep Inc.

- Simba Sleep Ltd.

- Hollander Sleep Products LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising incidence of insomnia among aging populations

- 4.2.2 Growing availability of OTC melatonin & natural supplements

- 4.2.3 Surge in smart-sleep technology adoption (IoT beds & trackers)

- 4.2.4 Corporate wellness programs adding sleep solutions

- 4.2.5 Insurance reimbursement expansion for PAP & oral devices

- 4.2.6 Hotel "sleep-tourism" packages boosting premium bedding demand

- 4.3 Market Restraints

- 4.3.1 Reported side-effects & dependency fears over prescription drugs

- 4.3.2 Patent cliffs for blockbuster hypnotics

- 4.3.3 Price sensitivity in emerging economies

- 4.3.4 Counterfeit supplements on e-commerce channels

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Product Type (Value)

- 5.1.1 Mattresses & Pillows

- 5.1.2 Sleep Apnea Devices

- 5.1.3 Medications

- 5.1.4 Supplements

- 5.1.5 Smart Sleep Monitoring Devices

- 5.1.6 Other Devices & Accessories

- 5.2 By Sleep Disorder (Value)

- 5.2.1 Insomnia

- 5.2.2 Sleep Apnea

- 5.2.3 Restless Legs Syndrome

- 5.2.4 Narcolepsy

- 5.2.5 Others

- 5.3 By End User (Value)

- 5.3.1 Residential

- 5.3.2 Medical (Hospitals & Sleep Labs)

- 5.3.3 Hotel & Hospitality

- 5.3.4 Others

- 5.4 By Geography (Value)

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Spain

- 5.4.2.6 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 Australia

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 GCC

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Koninklijke Philips N.V.

- 6.3.2 ResMed Inc.

- 6.3.3 Tempur Sealy International Inc.

- 6.3.4 GlaxoSmithKline plc

- 6.3.5 Perrigo Company plc

- 6.3.6 Merck & Co. Inc.

- 6.3.7 Sanofi S.A.

- 6.3.8 Sommetrics Inc.

- 6.3.9 Itamar Medical Ltd.

- 6.3.10 Drive DeVilbiss Healthcare

- 6.3.11 Teva Pharmaceutical Industries Ltd.

- 6.3.12 Cadwell Industries Inc.

- 6.3.13 Natrol LLC

- 6.3.14 Procter & Gamble Co.

- 6.3.15 Bayer AG

- 6.3.16 Fitbit LLC (Google)

- 6.3.17 Eight Sleep Inc.

- 6.3.18 Casper Sleep Inc.

- 6.3.19 Simba Sleep Ltd.

- 6.3.20 Hollander Sleep Products LLC

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment