PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043908

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043908

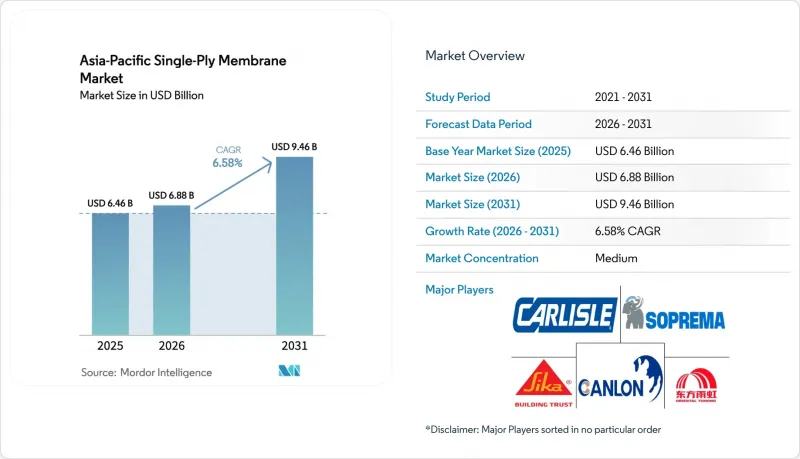

Asia-Pacific Single-Ply Membrane - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Asia-Pacific Single-Ply Membrane Market size is projected to expand from USD 6.46 billion in 2025 and USD 6.88 billion in 2026 to USD 9.46 billion by 2031, registering a CAGR of 6.58% between 2026 to 2031.

Infrastructure investments in China, Vietnam, and Indonesia continue to drive demand for bridges, tunnels, and landfills. Meanwhile, net-zero building codes in India and Japan are accelerating the adoption of cool roofs, directing spending toward white thermoplastic polyolefin (TPO) and ethylene-propylene-diene monomer (EPDM) roofing materials. Data center operators in Singapore, Mumbai, and Jakarta are increasingly specifying membrane systems with four-hour cure windows to minimize cooling downtime. TPO's heat-welded seams meet these requirements more effectively than torch-applied modified bitumen sheets. The shift toward factory-welded products is gaining momentum as modular construction standards expand. For example, Hong Kong's public housing Modular Integrated Construction (MiC) program and China's 30% prefabrication mandate have reduced on-site labor by 30% and lowered defect rates to below 2%. However, a volatile polyolefin feedstock cycle, projected to increase by 22% between January 2024 and December 2025, is putting pressure on gross margins. Despite this, vertical integration strategies by companies such as Sika, Oriental Yuhong, and Dow are helping these market leaders mitigate cost pressures and maintain a competitive edge over smaller extruders.

Asia-Pacific Single-Ply Membrane Market Trends and Insights

Tightening Building-Energy Codes Driving Cool-Roof Adoption

Mandatory cool-roof thresholds are turning energy-efficiency objectives into enforceable procurement criteria, favoring high-albedo TPO and PVC membranes. India's Energy Conservation Building Code 2024 specifies an SRI >= 78 for low-slope roofs across nine climate zones, effectively excluding dark modified bitumen from new projects in cities such as Chennai, Hyderabad, and Kolkata. Japan's revised Building Energy Efficiency Act, effective April 2025, mandates non-residential buildings larger than 300 m2 to meet passive-cooling standards, driving EPDM upgrades in office buildings across Tokyo and Osaka. In China, the GB 50189 update links green-building tax incentives to reflective roofs, accelerating TPO adoption in cities like Shenzhen and Guangzhou. Singapore's Green Mark 2024 provides bonus points for roofs with an aged SRI >= 63, aligning its standards with California Title 24 benchmarks. Collectively, these regulations are projected to reduce the market share of non-reflective membranes by an estimated 18-22% in major Asia-Pacific metropolitan areas by 2028.

Accelerating Re-Roofing Cycle in Commercial Real Estate

Aging building inventories in Japan, South Korea, and India are shortening re-roofing cycles from 25-30 years to 18-22 years, as property owners prioritize energy savings over lifecycle extensions. India's commercial renovation market reached INR 45,000 crore (USD 5.3 billion) in 2025, with 45% of leases involving refurbished properties. Japanese developers have expedited retrofits to comply with the April 2025 efficiency law, despite a 7.1% decline in new construction starts as of October 2024. In South Korea, property owners in Seoul and Busan accessed KRW 2.5 trillion (USD 1.9 billion) in low-interest loans for housing upgrades, focusing on reflective roofs. In Singapore, landlords are proactively re-roofing Grade-A properties, such as the Marina Bay Financial Centre, up to eight years ahead of schedule to maintain Green Mark Platinum certifications. Re-roofing is transitioning from a reactive measure to a proactive environmental, social, and governance (ESG) investment, yielding rental increases of 12-15% in sustainability-focused markets.

Volatile Polyolefin and Plasticizer Prices

Crude oil-driven polypropylene price swings of 22% between January 2024 and December 2025 reduced the gross margins of non-integrated TPO extruders by 3-5 percentage points. Plasticizer costs for PVC membrane production increased by 18% in Q2 2025 following China's addition of four phthalates to its RoHS restricted list. Dow's silicone expansion in Zhangjiagang aims to address non-phthalate alternatives; however, the 18-24 months required for field validation delays broader commercial adoption. Smaller producers in Vietnam and Indonesia, lacking hedging mechanisms, implemented downstream price increases of 12-15%, leading to project delays in cost-sensitive infrastructure tenders. These market dynamics have accelerated vertical integration strategies, such as Sika's resin acquisition and Oriental Yuhong's entry into bitumen refining. These approaches help mitigate input cost volatility and strengthen market positions in the Asia-Pacific single-ply membrane segment.

Other drivers and restraints analyzed in the detailed report include:

- Government Net-Zero Mandates Boosting Reflective Membranes

- Modular Construction Boosting Demand for Factory-Welded Rolls

- PVC and Phthalate Regulatory Scrutiny

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Modified bitumen accounted for 32.38% of the Asia-Pacific single-ply membrane market share in 2025, while TPO is projected to grow at a CAGR of 8.41% through 2031. Infrastructure buyers continue to prefer torch-applied bitumen for freeze-thaw bridges under China's Belt and Road procurement standards. On the other hand, data-center clients increasingly adopt heat-welded TPO, which meets <= 0.5% seam-failure targets and four-hour cure windows, driving its adoption in Singapore, Jakarta, and Mumbai campuses. EPDM holds a mid-teens market share, favored by Tokyo renovators for its closed-cell resilience against typhoon-driven rain. PVC's growth is hindered by China's phthalate ban, although high-rise condo developers in Singapore value its weldability in areas where torch flames are prohibited.

Modified bitumen's dominance in bridges and tunnels is expected to decline gradually, with a 4-6 percentage point reduction by 2029 as India's SRI threshold is fully implemented. EPDM's market presence is strengthening due to Japan's stimulus for retrofit energy savings, while PVC suppliers are racing to qualify non-phthalate plasticizers ahead of China's January 2026 deadline.

The Asia-Pacific Single-Ply Membrane Market Report Segments the Industry Into by Type (Ethylene Propylene Diene Monomer (EPDM), Thermoplastic Polyolefin (TPO), Polyvinyl Chloride (PVC), Modified Bitumen, Other Types), by Application (Residential, Commercial, Industrial and Institutional, Infrastructure), and by Geography (India, China, Japan, South Korea, ASEAN Countries, Rest of Asia-Pacific).

List of Companies Covered in this Report:

- BMI Group

- Carlisle Companies Inc.

- CKS Roofing

- Dow Inc.

- GAF Materials

- H.B. Fuller

- Holcim

- Hongyuan waterproof technology group co.,ltd

- Jiangsu Canlon Building Materials Co.,Ltd.

- Joaboa Technology

- Johns Manville

- Oriental Yuhong

- Polygomma

- Protan AS

- Renolit SE

- Sika AG

- Soprema Group

- Tremco Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening building-energy codes driving cool-roof adoption

- 4.2.2 Accelerating re-roofing cycle in commercial real-estate

- 4.2.3 Government net-zero mandates boosting reflective membranes

- 4.2.4 Modular construction boosting demand for factory-welded rolls

- 4.2.5 Data-centre capacity boom requiring low-downtime roof systems

- 4.3 Market Restraints

- 4.3.1 Volatile polyolefin and plasticizer prices

- 4.3.2 PVC and phthalate regulatory scrutiny

- 4.3.3 Skilled-installer shortage in Tier-2 Asia-Pacific cities

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Modified Bitumen

- 5.1.2 Ethylene Propylene Diene Monomer (EPDM)

- 5.1.3 Thermoplastic Polyolefin (TPO)

- 5.1.4 Polyvinyl Chloride (PVC)

- 5.1.5 Other Types

- 5.2 By Application

- 5.2.1 Infrastructure (Bridges, Tunnels, Landfills)

- 5.2.2 Residential

- 5.2.3 Commercial

- 5.2.4 Industrial and Institutional

- 5.3 By Construction Type

- 5.3.1 New Construction

- 5.3.2 Refurbished/Renovation

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Indonesia

- 5.4.6 Vietnam

- 5.4.7 Thailand

- 5.4.8 Malaysia

- 5.4.9 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 BMI Group

- 6.4.2 Carlisle Companies Inc.

- 6.4.3 CKS Roofing

- 6.4.4 Dow Inc.

- 6.4.5 GAF Materials

- 6.4.6 H.B. Fuller

- 6.4.7 Holcim

- 6.4.8 Hongyuan waterproof technology group co.,ltd

- 6.4.9 Jiangsu Canlon Building Materials Co.,Ltd.

- 6.4.10 Joaboa Technology

- 6.4.11 Johns Manville

- 6.4.12 Oriental Yuhong

- 6.4.13 Polygomma

- 6.4.14 Protan AS

- 6.4.15 Renolit SE

- 6.4.16 Sika AG

- 6.4.17 Soprema Group

- 6.4.18 Tremco Inc.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment