PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043911

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043911

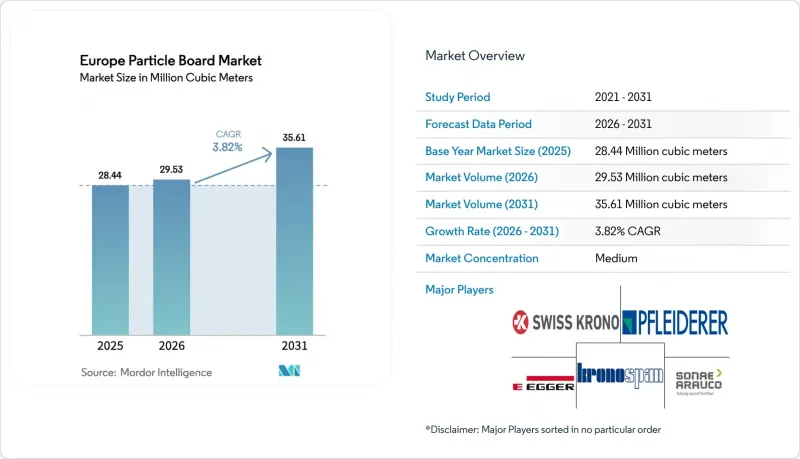

Europe Particle Board - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe Particle Board Market size is projected to expand from 28.44 million cubic meters in 2025 and 29.53 million cubic meters in 2026 to 35.61 million cubic meters by 2031, registering a CAGR of 3.82% between 2026 to 2031.

Mandatory low-VOC (Volatile Organic Compound) rules, recycled-wood mandates, and carbon-pricing of urea adhesives are redefining cost structures, prompting vertically integrated leaders to accelerate recycling hubs and bio-based binder pilots. Germany anchors demand with serial timber-housing programs, while Nordic mills leverage forest ownership and combined-heat-and-power plants to cushion feedstock and energy risk. AI-optimized press lines from Siempelkamp and Dieffenbacher deliver double-digit efficiency gains, but mills lacking EUR 10-15 million automation budgets face widening operating-cost gaps. Tight sawdust supply, exacerbated by pellet-mill demand and CLT (Cross-Laminated Timber) off-cut diversion, continues to lift Austria's spot price above EUR 120/ton, spurring experiments with agricultural residues as substitute fibers.

Europe Particle Board Market Trends and Insights

Tightening EU Formaldehyde Limits Driving Ultra-Low-VOC Boards

EU Regulation 2023/1464 fixes a 0.062 mg/m3 ceiling for emissions from wood-based panels effective August 6, 2026, compelling adhesive reformulations or market exit. Germany adopted DIN EN 16516 back in 2020, giving domestic mills a six-year validation lead time, whereas many Southern and Eastern counterparts now rush to install test chambers and attain EN 717-1 certification. ECHA (European Chemicals Agency) guidelines published in May 2025 mandate chamber testing over supplier declarations, adding EUR 50,000-80,000 to SME (Small and Medium Enterprises) compliance per product line. Lignin-modified resins piloted at Metsa Fibre's Aanekoski demo plant remain 15-20% costlier than urea-formaldehyde, yet the promise of formaldehyde-free boards continues to attract R&D (research and development) budgets.

Capacity Expansions Using Recycled-Wood Feedstock

Sonae Arauco valorised 809,000 tons of recycled wood in 2024, achieving 33% incorporation, and targets 75% in selected mills by end-2025. EGGER's EUR 200 million Markt Bibart hub, supplied by Timberpak's urban-collection network, started recycling operations in summer 2025, while Kronospan Luxembourg produced the first 100% recycled-wood board in June 2024. Municipal tenders for demolition wood across Germany and Austria intensify competition; mills without contracts risk shortages as beetle damage and drought curb virgin spruce supply.

Energy-Price Volatility Squeezing Press-Line Margins

German pellet prices climbed 19% month-on-month to EUR 363.21 t in February 2025, raising press energy cost on boards that already consume 150-200 kWh/m3. Energy now accounts for up to 18% of production cost, trimming EBITDA by two to three points for mills unable to hedge contracts.

Other drivers and restraints analyzed in the detailed report include:

- Prefabricated Timber Housing and Off-Site Construction Uptake

- EU CBAM Credits Favouring Low-Embodied-Carbon Panels

- CLT/LVL Demand Diverting Wood Residues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Wood-based feedstock retained 57.83% of volume in 2025, but the Europe Particle Board market is pivoting toward recycled streams. Sonae Arauco's 33% recycled share in 2024 and EGGER's Markt Bibart hub demonstrate scaling momentum. Bagasse occupies a niche yet is forecast at 4.23% CAGR during the forecast period (2026-2031), as Mediterranean mills trial sugarcane residue blends at press temperatures below 150°C. Brewer's spent grain volumes near 6.4 million tons/year offer further optionality, although high moisture and logistics hurdles persist. Virgin spruce scarcity, exacerbated by bark-beetle outbreaks, keeps Austria's sawdust above EUR 120 per ton, underpinning recycled-wood premiums.

Producers capturing post-consumer wood streams gain hedge value as Europe Particle Board market size expansion tightens residue supply. Fraunhofer IAP's ReSpan project proved binder-free, 100% waste-wood boards feasible, hinting at a future in which mills decouple from virgin fiber and urea entirely. Operators that secure municipal demolition-wood tenders or commercialize agri-fiber recipes will lock in a margin advantage as circular-economy quotas tighten.

The Europe Particle Board Market Report is Segmented by Raw Material (Wood, Bagasse, and Other Raw Materials), Application (Furniture, Construction, Infrastructure, Packaging, and Others), and Geography (Germany, United Kingdom, France, Italy, Spain, Russia, NORDIC Countries, and Rest of Europe). The Market Forecasts are Provided in Terms of Volume (Cubic Meters).

List of Companies Covered in this Report:

- Action TESA Europe

- arauco

- Boise Cascade

- CFP

- EGGER Group

- FALCO

- Finsa

- Kastamonu Entegre

- Kronospan Ltd.

- Norbord Europe Ltd.

- Orlimex UK Ltd.

- Peter Benson (Plywood) Ltd.

- Pfleiderer

- SAUERLAND Spanplatte

- Sonae Arauco (UK) Ltd

- SWISS KRONO Group

- Swiss Krono Holding AG

- Unilin Division Panels

- Wanhua Ecoboard Co. Ltd.

- West Fraser

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Tightening European Union formaldehyde limits (EN 16516) driving ultra-low-VOC boards

- 4.2.2 Capacity expansions using recycled-wood feedstock

- 4.2.3 Prefabricated timber housing and off-site construction uptake

- 4.2.4 EU CBAM credits favouring low-embodied-carbon panels

- 4.2.5 AI-optimised press lines cutting energy 20 % and boosting capacity

- 4.3 Market Restraints

- 4.3.1 Energy-price volatility squeezing press-line margins

- 4.3.2 CLT/LVL demand diverting wood residues from PB

- 4.3.3 Mandatory EPD disclosure raising SME compliance cost

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitute Products & Services

- 4.7.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Raw Material

- 5.1.1 Wood

- 5.1.2 Bagasse

- 5.1.3 Other Raw Materials

- 5.2 By Application

- 5.2.1 Furniture

- 5.2.2 Construction

- 5.2.3 Infrastructure

- 5.2.4 Packaging

- 5.2.5 Others

- 5.3 By Geography

- 5.3.1 Germany

- 5.3.2 United Kingdom

- 5.3.3 France

- 5.3.4 Italy

- 5.3.5 Spain

- 5.3.6 Russia

- 5.3.7 NORDIC Countries

- 5.3.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Action TESA Europe

- 6.4.2 arauco

- 6.4.3 Boise Cascade

- 6.4.4 CFP

- 6.4.5 EGGER Group

- 6.4.6 FALCO

- 6.4.7 Finsa

- 6.4.8 Kastamonu Entegre

- 6.4.9 Kronospan Ltd.

- 6.4.10 Norbord Europe Ltd.

- 6.4.11 Orlimex UK Ltd.

- 6.4.12 Peter Benson (Plywood) Ltd.

- 6.4.13 Pfleiderer

- 6.4.14 SAUERLAND Spanplatte

- 6.4.15 Sonae Arauco (UK) Ltd

- 6.4.16 SWISS KRONO Group

- 6.4.17 Swiss Krono Holding AG

- 6.4.18 Unilin Division Panels

- 6.4.19 Wanhua Ecoboard Co. Ltd.

- 6.4.20 West Fraser

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment