PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043919

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043919

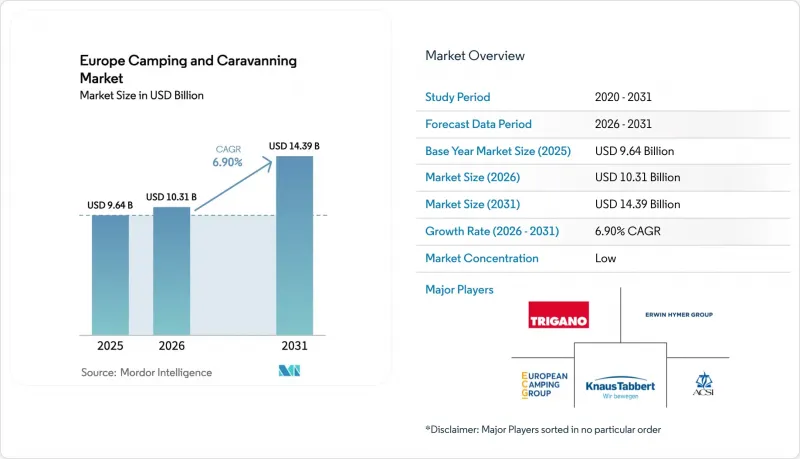

Europe Camping And Caravanning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe camping and caravanning market size is expected to grow from USD 9.64 billion in 2025 to USD 10.31 billion in 2026 and is projected to reach USD 14.39 billion by 2031, reflecting a 6.90% CAGR over 2026-2031.

EU tourist accommodation recorded 413 million campsite nights in 2025, accounting for 13% of the region's 3.08 billion total tourism nights, which reinforces the resilience of outdoor stays as a mainstream travel choice. Growth is supported by sustained domestic travel preferences that favor short-haul road trips, the early adoption of electrified recreational vehicles that pull forward premium demand, and the scaling of online booking platforms that compress distribution friction and expand inventory reach. Operators are countering peak-season concentration through investments in all-weather amenities and year-round infrastructure, a strategy validated by winter-oriented portfolio additions in the Nordics and selective municipal partnerships that extend capacity through standardized motorhome stopovers. Technology-enabled yield management and certification-led differentiation remain important levers for operators seeking to protect pricing power and sustain margins as energy and labor costs rise.

Europe Camping And Caravanning Market Trends and Insights

Domestic tourism sees a surge in nights booked, rebounding from COVID-19 setbacks

Domestic guests remained the anchor of Europe's travel recovery, and 2025 campsite nights equaled 13% of all EU tourism nights, which indicates that outdoor accommodation has continued to benefit from short-haul travel and near-home itineraries. The Europe camping and caravanning market gains from travelers who value space, nature access, and affordability relative to hotels during periods of price pressure in air travel and urban stays. Germany's broad-based tourism strength in 2025 supported incremental demand for camping nights as drive-to trips stayed popular for families and retirees alike, reinforcing steady occupancy in high-capacity regions. Operators increasingly design amenities that fit blended travel, such as quiet work areas and robust Wi-Fi, which supports longer stays by guests mixing workdays with outdoor leisure. The Europe camping and caravanning market continues to consolidate domestic loyalty by highlighting value-for-money and showcasing eco-certified sites that match preferences in Northern and Western Europe.

Recreational vehicles undergo a green transformation with electrification (eRVs)

Innovation in eRVs is catalyzing a higher-value segment that benefits the Europe camping and caravanning market over the long term through upgrades to vehicles and on-site power infrastructure. Recent product showcases, including electrified drivetrains and high-capacity lithium battery systems in compact all-wheel-drive models, signal a push toward vehicles that can reach remote pitches while powering modern amenities. Lightweight caravan concepts optimized for EV towing aim to broaden access among urban consumers, which may increase off-peak travel and diversify site usage. Northern operators are adding EV charging and renewable energy features, which positions certified sites to attract early adopters and sustainability-minded guests. The Europe camping and caravanning market benefits as infrastructure-readiness becomes a booking filter for higher-spend travelers selecting sites that can support electric tow vehicles and silent, battery-based onboard systems.

Campgrounds face challenges with seasonal fluctuations and under-utilized capacity

Seasonality limits year-round utilization and strains cash flows outside peak months, with official data showing a concentration of stays in Q3 for the EU. Even strong summer performance can waver due to weather or geopolitical sensitivities, and several Mediterranean hubs have highlighted occupancy volatility during peak weeks. In August 2025, Croatia reported a high number of camping nights but also revealed a dip in occupancy compared with the prior year, which highlights exposure to short-term shocks despite seasonal peaks. Financing new amenities becomes more complex when revenue is concentrated in one quarter, as lenders price higher risk into terms and operators weigh returns over a shorter operating window. The Europe camping and caravanning market therefore places a premium on season-extension levers and municipal collaborations that transform idle winter space into shoulder-season stays.

Other drivers and restraints analyzed in the detailed report include:

- Online platforms for campsite bookings witness significant expansion

- Investments pour in for season-extension, introducing all-weather amenities

- RVs grapple with strict regulations on emissions and size

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Privately owned campgrounds captured 35.74% of the 2025 market value, reflecting consistent investments in amenities and branding that sustain price premiums, and this concentration shows how quality and service breadth support share within the Europe camping and caravanning market size in 2025. State and national park campgrounds appeal to guests focused on trails and nature access, yet they often face constraints on dynamic pricing and amenity expansion. Parking lots and standardized stopovers have grown as a convenience layer for itinerant RV users, supported by networks that deliver reliable, year-round pitches near towns and public attractions. Public or privately owned land outside formal campgrounds remains a niche defined by local zoning and conservation rules, which drives uncertainty for operators and travelers. The Europe camping and caravanning market continues to reward professional management where facilities, compliance, and digital distribution converge to keep occupancy steady across variable conditions.

Backcountry, national forest, and wilderness areas are forecast to expand at a 9.12% CAGR to 2031, led by younger travelers who value immersive nature stays and minimal infrastructure, which positions this segment as a fast-growth counterweight to legacy campground formats. Nordic markets exemplify this shift with strong summer camping nights in nature-rich regions and a cultural emphasis on responsible outdoor life, which supports longer itineraries and diversified stay types that blend cabins, tents, and minimalist pitches. As local restrictions tighten in sensitive areas, operators respond with "nature-near" sites that preserve wilderness appeal while delivering basic sanitation and safety aligned to certification frameworks. These formats help municipalities balance environmental stewardship with visitor flows, a trade-off that becomes more important as peak-season crowds concentrate in headline destinations. The Europe camping and caravanning industry adapts by curating low-impact options that meet standards while maintaining the authenticity sought by backcountry-oriented guests.

The Europe Camping and Caravanning Market Report is Segmented by Destination Type (State or National Park Campgrounds, Privately Owned Campgrounds, Public or Privately Owned Land Other Than A Campground, Backcountry/National Forest/Wilderness Areas, Parking Lots, and Others), Type of Camper (Car Camping, and Other), and Geography (United Kingdom, Germany, and Others). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- European Camping Group

- ACSI

- Erwin Hymer Group

- Trigano

- Knaus Tabbert

- Adria Mobil

- Hobby Wohnwagenwerk

- Dethleffs

- Bailey of Bristol

- Swift Group

- Sun Communities (UK & EU parks)

- Camping & Caravanning Club

- Pitchup.com

- Eurocampings

- Vacanceselect

- Yelloh! Village

- Huttopia

- Vacansoleil

- Cool Camping

- Campercontact (NKC)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising domestic tourism nights post-COVID-19

- 4.2.2 Recreational vehicles undergo a green transformation with electrification (eRVs)

- 4.2.3 Online platforms for campsite bookings witness significant expansion

- 4.2.4 Investments pour in for season-extension, introducing all-weather amenities

- 4.2.5 High-spending campers drawn in by eco-certifications

- 4.2.6 Rural tourism redevelopment gets a boost from government incentives

- 4.3 Market Restraints

- 4.3.1 Campgrounds face challenges with seasonal fluctuations and under-utilized capacity

- 4.3.2 RVs grapple with strict regulations on emissions and size.

- 4.3.3 Land-use conflicts & local zoning restrictions

- 4.3.4 Rising operating costs (energy, labour, insurance)

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Destination Type

- 5.1.1 State or National Park Campgrounds

- 5.1.2 Privately Owned Campgrounds

- 5.1.3 Public or Privately Owned Land Other Than a Campground

- 5.1.4 Backcountry, National Forest or Wilderness Areas

- 5.1.5 Parking Lots

- 5.1.6 Others

- 5.2 By Type of Camper

- 5.2.1 Car Camping

- 5.2.2 RV Camping

- 5.2.3 Backpacking

- 5.2.4 Others

- 5.3 By Distribution Channel

- 5.3.1 Direct Sales

- 5.3.2 Online Travel Agencies

- 5.3.3 Traditional Travel Agencies

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Spain

- 5.4.5 Italy

- 5.4.6 BENELUX (Belgium, Netherlands, Luxembourg)

- 5.4.7 NORDICS (Denmark, Finland, Iceland, Norway, Sweden)

- 5.4.8 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 European Camping Group

- 6.4.2 ACSI

- 6.4.3 Erwin Hymer Group

- 6.4.4 Trigano

- 6.4.5 Knaus Tabbert

- 6.4.6 Adria Mobil

- 6.4.7 Hobby Wohnwagenwerk

- 6.4.8 Dethleffs

- 6.4.9 Bailey of Bristol

- 6.4.10 Swift Group

- 6.4.11 Sun Communities (UK & EU parks)

- 6.4.12 Camping & Caravanning Club

- 6.4.13 Pitchup.com

- 6.4.14 Eurocampings

- 6.4.15 Vacanceselect

- 6.4.16 Yelloh! Village

- 6.4.17 Huttopia

- 6.4.18 Vacansoleil

- 6.4.19 Cool Camping

- 6.4.20 Campercontact (NKC)

7 Market Opportunities & Future Outlook

- 7.1 Development of net-zero, off-grid campsite models

- 7.2 AI-driven dynamic pricing & yield-management solutions