PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043921

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043921

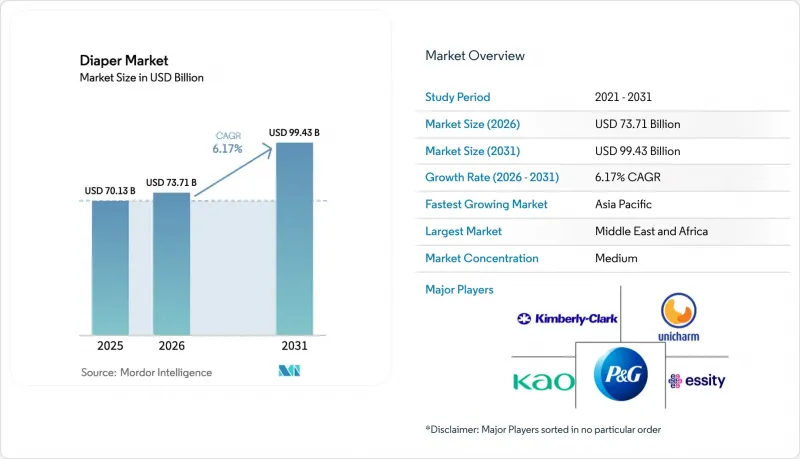

Diaper - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The diaper market size is expected to increase from USD 70.13 billion in 2025 to USD 73.71 billion in 2026 and reach USD 99.43 billion by 2031, growing at a CAGR of 6.17% over 2026-2031.Demand is shifting from infant care products to adult incontinence solutions due to aging global populations and declining birth rates, particularly in China and Japan.

Manufacturers are allocating research and development budgets toward high-performance super-absorbent polymers and breathable nonwovens to maintain premium pricing, despite fluctuations in raw material costs. Sustainability regulations in Europe and several United States states are accelerating the adoption of bio-based materials. Additionally, e-commerce subscription models are strengthening brand loyalty and minimizing the risk of stock shortages. While competitive intensity remains moderate, with the top five suppliers dominating shelf space, direct-to-consumer brands are challenging this position through targeted online marketing and quicker product innovation cycles.

Global Diaper Market Trends and Insights

Rising prevalence of adult incontinence due to aging populations and longer life expectancy

Adult incontinence has shifted from being a niche issue to a significant concern in the broader market, influencing product development strategies. In the United States, millions of adults are affected by bladder conditions, with prevalence rates higher among women compared to men. In Germany, the overall incontinence rate has shown an increase, with a higher prevalence among females than males. In China, the elderly population shows even more pronounced trends, with a significant percentage of women and men over the age of 65 experiencing incontinence. The population aged 60 and above in China represents a substantial portion of the total population. In Japan, a significant milestone was reached when adult diaper demand surpassed that of baby diapers, leading at least one major manufacturer to discontinue infant diaper production and shift focus to elderly care products. In the coming decades, the United States is projected to have a growing population of adults aged 65 and older. With increasing life expectancy, these individuals are expected to spend more years managing chronic conditions. This demographic shift is driving manufacturers to develop discreet, high-capacity products with odor-control features, catering to active seniors who prioritize mobility and independence.

Increasing awareness of infant hygiene and skin health among parents

Parental concerns about diaper rash and skin irritation have increased, driven by the influence of digital platforms that amplify peer reviews and dermatological research. Diapers containing shea butter-based emollients have shown measurable reductions in erythema, highlighting the effectiveness of plant-derived barrier creams integrated into nonwoven layers. In September, Sam's Club introduced its Member's Mark Premium Diaper, emphasizing a hypoallergenic construction free from lotions, parabens, and fragrances, along with sustainably sourced pulp. This product appeals to millennial and Generation Z parents who carefully examine ingredient lists. In India, where urbanization has been steadily increasing and middle-class households are expected to grow significantly in the coming years, parents are increasingly shifting from cloth to disposable diapers and from economy to premium options as disposable incomes rise. Digital commerce platforms such as Meesho, which reported a large number of annual transacting users in fiscal year 2025, with a significant portion of these users from non-metropolitan regions, are expanding access to branded hygiene products in Tier 2 and Tier 3 cities, where traditional retail penetration remains limited. This transition from unbranded to branded consumption represents a structural shift rather than a cyclical trend, ensuring sustained volume growth even as birth rates stabilize or decline in urban areas.

Environmental concerns over non-biodegradable plastic waste in landfills

Disposable diapers make up a small but notable portion of municipal solid waste in developed economies. Their long decomposition periods have become a significant concern for environmental advocacy groups and municipal waste management authorities. The European Union's Single-Use Plastics Directive specifically addresses sanitary items, prompting member states to explore extended producer responsibility (EPR) schemes that transfer disposal costs to manufacturers. For example, France introduced extended producer responsibility for single-use sanitary textiles in January 2025, requiring brands to finance collection and recycling infrastructure. In coastal cities across the Asia-Pacific region, where landfill capacity is limited and incineration raises air quality concerns, municipal governments are implementing landfill taxes and waste-reduction mandates. These policies increase the overall cost of ownership for disposable products. At the same time, consumer attitudes are changing. Surveys conducted in North America and Europe show that many parents, particularly millennials and Generation Z, feel guilt over diaper waste and are actively exploring biodegradable or cloth alternatives. This shift in sentiment is leading to market share declines for conventional disposable diapers, especially in premium segments where environmentally conscious consumers are more prevalent. Brands that do not implement credible sustainability initiatives, supported by third-party certifications such as the Cradle to Cradle standard or the United States Department of Agriculture BioPreferred label, risk losing market share. Niche competitors and private-label products marketed as environmentally sustainable are gaining traction among consumers who prioritize environmentally friendly options. For instance, the United States Department of Agriculture (USDA) BioPreferred label is increasingly recognized as a marker of sustainability, influencing purchasing decisions in favor of certified products.

Other drivers and restraints analyzed in the detailed report include:

- Technological advancements in superabsorbent polymers for better leakage protection

- Growing demand for eco-friendly and biodegradable diaper options

- Stringent regulations on material safety and waste disposal

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Disposable diapers accounted for 67.21% of the market in 2025, highlighting their strong presence in urban households where convenience and performance take precedence over environmental concerns. Cloth and hybrid diapers, although starting from a smaller market base, are projected to grow at an annual rate of 7.52% through 2031, marking the fastest growth among product types. This growth is driven by environmentally conscious parents and institutional childcare centers seeking alternatives to petroleum-based superabsorbent polymers. In February 2025, BASF introduced HySorb B 6610 ZeroPCF, a zero-carbon-footprint superabsorbent polymer made using renewable electricity and bio-based acrylic acid, indicating that established players are investing in sustainable formulations to maintain their share in the disposable diaper market.

Similarly, Ontex's bio-based superabsorbent polymer (bioSAP), which offers a 15% to 25% reduction in carbon footprint, demonstrates that incorporating partial bio-based content can help bridge the performance gap between conventional and fully biodegradable options. The key challenge remains whether disposable diapers can adapt quickly enough to meet regulatory requirements and consumer expectations or if hybrid diapers will secure a lasting position among affluent, environmentally conscious consumers.

In the United States, approximately 100 million adults are affected by bladder conditions, with a prevalence of 14% among men and 51% among women, according to the National Association for Continence. In Germany, the overall incontinence rate was reported at 14.7% in 2025, increasing to 17.8% among females, as noted in a peer-reviewed epidemiology study. These statistics highlight that adult incontinence has transitioned from being a niche issue to a widespread concern, influencing product development strategies.

Manufacturers are addressing this shift by focusing on discreet, high-capacity designs and odor-control technologies that cater to active seniors who prioritize mobility. Procter and Gamble's Pampers Preemie Extra Extra Small (XXS), introduced in November 2025, is designed for premature infants weighing less than 500 grams. This product not only meets a specific medical need but also reflects the brand's strategy to further segment the baby care market.

The Diaper Market Report is Segmented by Product Type (Disposable Diapers, Cloth and Hybrid Diapers), Age Group (Baby Diapers, Adult Diapers), Category (Premium, Mass), Distribution Channel (Supermarkets and Hypermarkets, Pharmacies and Drugstores, and More), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia-Pacific region led the market, accounting for 40.12% of the total share. This dominance was driven by Unicharm's strong presence in India, where the company operates three factories and holds a significant market share, second only to Procter & Gamble. Unicharm's third factory in Gujarat, a Japanese Yen (JPY) 20 billion investment announced in February 2025, is expected to boost production capacity by 30% and create approximately 1,000 jobs. In China, despite a decline in births from 14.7 million in 2019 to 7.92 million in 2025, the market remains critical due to premiumization. Procter & Gamble's Pampers Prestige line, featuring silk fibers, achieved double-digit growth and a three-percentage-point market share increase, with Greater China organic sales rising by 20% in the latest quarter. In Japan, a demographic shift in 2024, where adult diaper demand surpassed baby diaper volumes, led at least one major manufacturer to cease infant diaper production and refocus on elderly care products.

The Middle East and Africa region is projected to grow at the fastest rate globally, with a compound annual growth rate (CAGR) of 7.08% through 2031. This growth is fueled by accelerating urbanization in countries such as Nigeria, Egypt, and Saudi Arabia, along with improvements in healthcare infrastructure. Unicharm's joint venture with Toyota Tsusho in Kenya, announced in June 2025 and named Sofy East Africa Limited, aims to produce baby care and feminine care products. This move reflects the company's confidence in the region's long-term potential.

Other regions, such as North America and Europe, face challenges from stagnant birth rates but benefit from premiumization trends. Kimberly-Clark's USD 2 billion investment over five years in North American manufacturing, including an approximately USD 800 million facility in Warren, Ohio, focuses on producing next-generation Huggies with automated waistbands and quilted protection, emphasizing a shift toward higher-margin products. In South America, the market remains fragmented, with local players competing on price and incumbents facing challenges from currency volatility and import dependency. For instance, Brazil's Cost, Insurance, and Freight (CIF) Santos superabsorbent polymer prices rose to USD 1,450 to USD 1,470 per metric ton in the third quarter of 2025, an 11.46% increase, highlighting the region's susceptibility to global supply chain disruptions. However, urbanization and rising disposable incomes in countries like Colombia, Chile, and Peru are creating opportunities for premium products. Global brands face the strategic challenge of balancing the need for local manufacturing to mitigate currency risks against the high capital requirements of establishing greenfield facilities in markets with uncertain regulatory environments and infrastructure limitations.

- Procter & Gamble Co.

- Kimberly-Clark Corp.

- Unicharm Corp.

- Essity AB

- Kao Corp.

- Ontex Group NV

- First Quality Enterprises Inc.

- Attindas Hygiene Partners

- Drylock Technologies NV

- Hengan International Group

- Chiaus (Fujian Quanzhou)

- Pigeon Corp.

- Abena A/S

- DSG International (Thailand) Plc

- Nobel Hygiene Pvt Ltd

- The Honest Company Inc.

- Seventh Generation Inc.

- Paul Hartmann AG

- Medline Industries LP

- TZMO SA

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising prevalence of adult incontinence due to aging populations and longer life expectanc

- 4.2.2 Increasing awareness of infant hygiene and skin health among parents

- 4.2.3 Technological advancements in superabsorbent polymers for better leakage protection

- 4.2.4 Growing demand for eco-friendly and biodegradable diaper options

- 4.2.5 Expansion of e-commerce and subscription services for easy access

- 4.2.6 Innovations in skin-friendly, hypoallergenic materials to prevent rashes

- 4.3 Market Restraints

- 4.3.1 Environmental concerns over non-biodegradable plastic waste in landfills

- 4.3.2 Stringent regulations on material safety and waste disposal

- 4.3.3 Low awareness of diaper benefits in rural or traditional areas

- 4.3.4 Dependency on imported raw materials affecting supply reliability

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Bargaining Power of Suppliers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Disposable Diapers

- 5.1.2 Cloth and Hybrid Diapers

- 5.2 By Age Group

- 5.2.1 Baby Diaper

- 5.2.2 Adult Diaper

- 5.3 By Category

- 5.3.1 Premium

- 5.3.2 Mass

- 5.4 By Distribution Channel

- 5.4.1 Supermarkets and Hypermarkets

- 5.4.2 Pharmacies and Drugstores

- 5.4.3 Online Retail/E-commerce

- 5.4.4 Other Distribution Channels

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Peru

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 South Africa

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 United Arab Emirates

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level Overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Procter & Gamble Co.

- 6.4.2 Kimberly-Clark Corp.

- 6.4.3 Unicharm Corp.

- 6.4.4 Essity AB

- 6.4.5 Kao Corp.

- 6.4.6 Ontex Group NV

- 6.4.7 First Quality Enterprises Inc.

- 6.4.8 Attindas Hygiene Partners

- 6.4.9 Drylock Technologies NV

- 6.4.10 Hengan International Group

- 6.4.11 Chiaus (Fujian Quanzhou)

- 6.4.12 Pigeon Corp.

- 6.4.13 Abena A/S

- 6.4.14 DSG International (Thailand) Plc

- 6.4.15 Nobel Hygiene Pvt Ltd

- 6.4.16 The Honest Company Inc.

- 6.4.17 Seventh Generation Inc.

- 6.4.18 Paul Hartmann AG

- 6.4.19 Medline Industries LP

- 6.4.20 TZMO SA

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK