PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043930

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043930

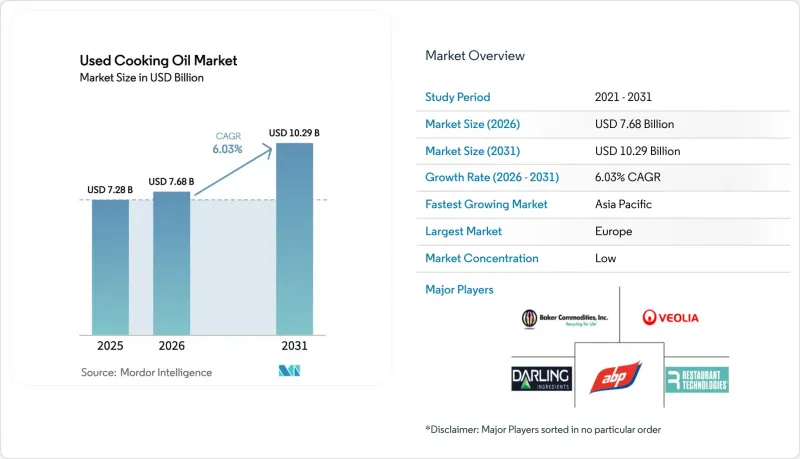

Used Cooking Oil - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Used Cooking Oil Market size was valued at USD 7.28 billion in 2025 and is estimated to grow from USD 7.68 billion in 2026 to reach USD 10.29 billion by 2031, at a CAGR of 6.03% during the forecast period (2026-2031).

Increasing mandates for sustainable aviation fuel (SAF), rising biodiesel quotas in road transport, and circular-economy regulations are shifting waste oils from being a disposal cost to becoming a valuable strategic feedstock. Airlines and refiners are entering multi-year offtake agreements in preparation for the 2030 blending deadlines. This trend is tightening supply and benefiting collectors who implement digital traceability solutions. While HoReCa chains remain the primary source of volume, municipalities are expanding curbside household collections to address the 30-40% recovery gap. Technology-driven aggregators, employing IoT sensors, blockchain for custody, and advanced multi-stage filtration, are improving yields and audit readiness, thereby capturing higher margins. Furthermore, refiners are drawn to the used cooking oil market due to feedstock arbitrage opportunities against volatile palm and soy oil prices, helping them maintain margins under credit schemes such as RFS, LCFS, and RED II.

Global Used Cooking Oil Market Trends and Insights

Growing aviation-sector demand for sustainable aviation fuel

Regulatory changes in aviation are transforming the demand for Used Cooking Oil (UCO), influencing the entire waste-fat value chain. The ReFuelEU Aviation initiative mandates a 6% blending of Sustainable Aviation Fuel (SAF) by 2030, increasing to 70% by 2050. Singapore's SAF requirements will begin at 1% in January 2026 and rise to 3-5% by 2030, while Thailand has introduced a similar 1% mandate for 2026. These strict timelines are narrowing the feedstock sourcing windows, prompting airlines and fuel producers to finalize multi-year UCO offtake agreements, often ahead of the development of adequate collection infrastructure. According to the World Economic Forum, global production capacity for HEFA sustainable aviation fuels (SAF) reached 4.2 million metric tons in 2025. In Thailand, PTTGC plans to expand its SAF capacity from 6 million liters to 24 million liters annually by 2027. Emirates and Etihad have signed offtake agreements with MENA Biofuels' Fujairah plant, which aims to produce 125 million liters of SAF annually using UCO and other waste fats. Japan's Cosmo Energy began supplying 30,000 kiloliters of UCO-derived SAF to Japan Airlines and All Nippon Airways in 2025, highlighting how markets with limited domestic UCO production are increasingly relying on imports to meet airline commitments. On the regulatory side, the European Union Aviation Safety Agency (EASA) and the International Civil Aviation Organization (ICAO), under the CORSIA framework, are standardizing sustainability criteria. This alignment has established ISCC PLUS certification as the leading standard for international UCO trade, while penalizing suppliers unable to verify waste-origin traceability.

Circular-economy and zero-waste regulations

Regulatory mandates are redefining Used Cooking Oil (UCO) from a disposal issue to a regulated and valuable commodity. The EU's Waste Framework Directive prioritizes reuse and recycling over incineration. Reflecting this, countries such as the UK and Germany have introduced extended producer-responsibility schemes. These initiatives require food-service operators to document UCO collection and recycling processes. In 2024, Japan's Ministry of the Environment updated its waste-management guidelines to incentivize municipal UCO collection. Similarly, South Korea incorporated cooking oils into its Extended Producer Responsibility (EPR) framework, aligning them with packaging-waste targets and supporting household-collection programs. In India, the Ministry of New and Renewable Energy (MNRE) launched the Repurpose Used Cooking Oil (RUCO) program to formalize UCO collection from hotels, restaurants, and households, directing it to biodiesel producers under the National Biofuel Policy's 5% blending target. In 2023, China's National Energy Administration (NEA) identified UCO as a priority feedstock in its biodiesel pilot notice, marking a shift from export-driven collection to domestic consumption. These regulatory frameworks are driving food processors and quick-service restaurant chains to establish reverse-logistics networks. While this increases collection costs, it also creates entry barriers for informal aggregators lacking certification infrastructure.

Collection and consumption gaps across supply chain

In emerging markets, approximately 30-40% of used cooking oil (UCO) remains uncollected due to informal disposal practices and inadequate aggregation infrastructure. This limits feedstock availability despite the rising demand for sustainable aviation fuel (SAF) driven by increasing mandates. In India, the RUCO program highlighted collection gaps in tier-2 and tier-3 cities, where restaurants and households lack access to certified collectors. To address this, the Ministry of New and Renewable Energy is piloting municipal partnerships to establish drop-off points. In China, the collection system is fragmented, with small-scale aggregators dominating the landscape. These aggregators often sell to informal biodiesel producers or animal-feed mills, making traceability challenging. The 2024 export tariff increase was partially introduced to promote domestic formalization. In Southeast Asia, household UCO generation remains largely untapped. While Japan and South Korea have launched curbside collection trials, participation rates remain below 20% due to consumer inconvenience and limited awareness. In Europe, mature HoReCa networks often obscure household-collection deficiencies. For example, the UK's Department for Environment, Food and Rural Affairs (Defra) estimates that only 15-20% of household UCO is formally collected, with the rest disposed of through sewers or municipal waste. Bridging these collection gaps requires substantial investments in logistics, including dedicated collection vehicles, storage tanks, and digital tracking systems. However, many municipalities and small collectors cannot afford these investments without subsidies or extended producer-responsibility mandates.

Other drivers and restraints analyzed in the detailed report include:

- Price competitiveness compared to virgin vegetable oils

- Technological advancements in collection, filtration, and refining

- Quality variability and certification challenges

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, centralized kitchens and predictable volumes allowed HoReCa sites to lead the used cooking oil market, contributing 63.92% of the market size. These sites also proved to be the most cost-efficient feedstock for collectors. Quick-service restaurant chains have implemented standardized disposal procedures. By entering into multi-year contracts, they have effectively restricted auditor access to the supply chain, ensuring consistent certification. Additionally, industrial caterers at airports and hospitals support baseline flows, while food processors are incorporating oil recovery lines to reduce waste. Despite these developments, HoReCa networks in the Asia-Pacific region remain fragmented. However, state pilot programs in China and India are working to consolidate these volumes into formalized systems.

Household kitchens, expected to grow at a CAGR of 6.89% from 2026 to 2031, are set to become the next significant area for volume growth. Municipalities in Japan, South Korea, and the UK are actively engaging residents by providing sealable containers for used cooking oil and scheduling curbside pickups alongside glass and paper collections. Although this dispersed feedstock has lower FFA, making it suitable for oleo-chemical intermediates, its collection cost per liter is 2-3 times higher than that of HoReCa. Blockchain applications now enable residents to scan QR codes to log their deposits, offering collectors a verifiable chain of custody essential for ISCC PLUS eligibility. Food-processing plants, occupying a stable middle ground, sometimes direct their used cooking oil to their own biodiesel units, helping to stabilize seasonal variations in collector volumes.

The Used Cooking Oil Market Report is Segmented by Source (HoReCa, Household Kitchens, Food Processing Plants), End Use (Biodiesel and HVO, Oleo-Chemicals, Animal Feed, Others), and Geography (North America, South America, Europe, Asia-Pacific, Middle East and Africa). Market Forecasts are Provided in Terms of Value (USD) and Volume (Liters).

Geography Analysis

In 2025, Europe accounted for 38.09% of global revenue, driven by key regulatory frameworks and infrastructure. The UK's Renewable Transport Fuel Obligation (RTFO), Germany's Greenhouse Gas (GHG) quota, and the Netherlands' role as a trans-shipment hub were significant contributors to this performance. In 2024, the RTFO's double crediting mechanism incentivized the production of 1 billion liters of fuels derived from used cooking oil (UCO). Additionally, the ReFuelEU Aviation initiative redirected future UCO supplies towards jet fuel applications, thereby reducing the availability of UCO for road-diesel blending. Efforts to improve residential UCO recovery rates, currently at 15-20%, are underway through household pilot programs in Sweden, Denmark, and the UK. However, the scalability of these initiatives depends heavily on the availability of municipal funding.

Asia-Pacific is positioned as the primary growth driver in the market, with a compound annual growth rate (CAGR) of 7.13% projected through 2031. Singapore's introduction of a 1% Sustainable Aviation Fuel (SAF) mandate starting in 2026, Thailand's significant capacity expansion, and China's strategic shift towards domestic blending are reshaping the region's market dynamics. In India, the Repurpose Used Cooking Oil (RUCO) initiative is formalizing contracts with the HoReCa (Hotels, Restaurants, and Catering) sector to streamline UCO collection. Japan's Cosmo Energy is demonstrating a model for import-driven SAF supply. RUCO agencies in Karnataka, India, reported the collection of 32,68,990 liters of used cooking oil during the financial years 2024-25 and 2025-26. Meanwhile, Indonesia and Australia are leveraging the growing regional demand for SAF by establishing partnerships with Southeast Asian UCO collectors.

North America continues to rely on the Renewable Fuel Standard (RFS) and Low Carbon Fuel Standard (LCFS) incentives, which reward low-carbon fuel pathways. In Canada, the Clean Fuel Regulations add an additional layer of provincial credits to support the adoption of sustainable fuels. In Brazil, the B14 biodiesel mandate, combined with stringent fraud-control protocols, has resulted in a reduced export supply of UCO to Europe. In the Middle East, the UAE and Saudi Arabia are developing SAF production hubs, with a collective target of producing 475 million liters by 2029. These hubs depend on the import of UCO from regions such as Africa and South Asia. In South Africa, municipal UCO collection pilot programs are being tested, but the lack of robust policy support remains a significant challenge to their success.

- Darling Ingredients Inc.

- Baker Commodities Inc.

- Veolia Environnement SA

- Olleco (ABP Food Group)

- Restaurant Technologies Inc.

- Neste Oyj

- Argent Energy

- GreaseCycle

- Brocklesby Ltd.

- MBP Solutions

- Bunge Ltd.

- Eni SpA

- Arrow Oils Ltd.

- Agri Trading Inc.

- Saria Group (Rendac)

- Quatra BV

- Muenzer Bioindustrie GmbH

- Greenlife Oil Holdings Pty Ltd

- Green Planet Bio-Fuels Inc.

- Renewable Energy Group ( Chevron )

- Greenergy Ltd.

- Mahoney Environmental

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for biodiesel and other biofuels

- 4.2.2 Growing aviation-sector demand for sustainable aviation fuel

- 4.2.3 Price competitiveness compared to virgin vegetable oils

- 4.2.4 Circular-Economy and Zero-Waste Regulations

- 4.2.5 Technological advancements in collection, filtration, and refining

- 4.2.6 Digitalization of collection and logistics

- 4.3 Market Restraints

- 4.3.1 Collection and consumption gaps across supply chain

- 4.3.2 Quality variability and certification challenges

- 4.3.3 Export-tariff hikes amid SAF feed-stock competition

- 4.3.4 Dependence of UCO economics on policy incentives

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 By Source

- 5.1.1 HoReCa (Hotels, Restaurants, Catering)

- 5.1.2 Household Kitchens

- 5.1.3 Food Processing Plants

- 5.2 By End Use

- 5.2.1 Biodiesel and HVO

- 5.2.2 Oleo-chemicals

- 5.2.3 Animal Feed

- 5.2.4 Others (Cosmetics, etc.)

- 5.3 By Geography

- 5.3.1 North America

- 5.3.1.1 United States

- 5.3.1.2 Canada

- 5.3.1.3 Mexico

- 5.3.1.4 Rest of North America

- 5.3.2 South America

- 5.3.2.1 Brazil

- 5.3.2.2 Argentina

- 5.3.2.3 Colombia

- 5.3.2.4 Chile

- 5.3.2.5 Rest of South America

- 5.3.3 Europe

- 5.3.3.1 United Kingdom

- 5.3.3.2 Germany

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 Sweden

- 5.3.3.8 Belgium

- 5.3.3.9 Poland

- 5.3.3.10 Netherlands

- 5.3.3.11 Rest of Europe

- 5.3.4 Asia-Pacific

- 5.3.4.1 China

- 5.3.4.2 Japan

- 5.3.4.3 India

- 5.3.4.4 Thailand

- 5.3.4.5 Singapore

- 5.3.4.6 Indonesia

- 5.3.4.7 South Korea

- 5.3.4.8 Australia

- 5.3.4.9 New Zealand

- 5.3.4.10 Rest of Asia-Pacific

- 5.3.5 Middle East and Africa

- 5.3.5.1 United Arab Emirates

- 5.3.5.2 South Africa

- 5.3.5.3 Saudi Arabia

- 5.3.5.4 Nigeria

- 5.3.5.5 Egypt

- 5.3.5.6 Morocco

- 5.3.5.7 Turkey

- 5.3.5.8 Rest of Middle East and Africa

- 5.3.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Darling Ingredients Inc.

- 6.4.2 Baker Commodities Inc.

- 6.4.3 Veolia Environnement SA

- 6.4.4 Olleco (ABP Food Group)

- 6.4.5 Restaurant Technologies Inc.

- 6.4.6 Neste Oyj

- 6.4.7 Argent Energy

- 6.4.8 GreaseCycle

- 6.4.9 Brocklesby Ltd.

- 6.4.10 MBP Solutions

- 6.4.11 Bunge Ltd.

- 6.4.12 Eni SpA

- 6.4.13 Arrow Oils Ltd.

- 6.4.14 Agri Trading Inc.

- 6.4.15 Saria Group (Rendac)

- 6.4.16 Quatra BV

- 6.4.17 Muenzer Bioindustrie GmbH

- 6.4.18 Greenlife Oil Holdings Pty Ltd

- 6.4.19 Green Planet Bio-Fuels Inc.

- 6.4.20 Renewable Energy Group ( Chevron )

- 6.4.21 Greenergy Ltd.

- 6.4.22 Mahoney Environmental

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK