PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043931

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043931

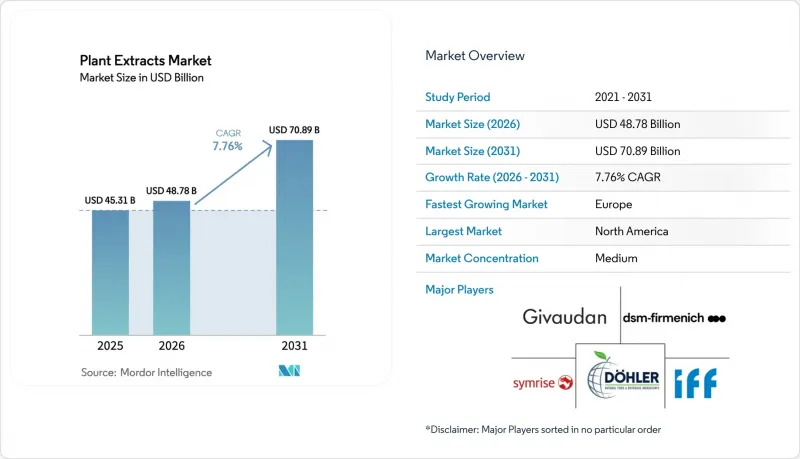

Plant Extracts - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Plant Extracts Market size was valued at USD 45.31 billion in 2025 and is estimated to grow from USD 48.78 billion in 2026 to reach USD 70.89 billion by 2031, at a CAGR of 7.76% during the forecast period (2026-2031).

This expansion is fueled by clean-label reformulations, AI-driven phytochemical discoveries, and regulatory advancements clarifying new dietary ingredient pathways in the U.S. and Novel Foods authorizations in Europe. Multinational flavor companies are utilizing vertically integrated supply chains, supported by blockchain-enabled traceability to reduce adulteration risks. Biorefinery projects are converting agricultural waste into valuable botanical actives, supporting circular economy objectives. Advanced extraction technologies, such as supercritical CO2, enzyme-assisted, and ultrasonic-assisted methods, are minimizing solvent use and energy consumption. Simultaneously, food security policies are encouraging manufacturers to replace synthetic additives with botanical alternatives, driving their adoption in functional foods, dietary supplements, cosmetics, and animal nutrition.

Global Plant Extracts Market Trends and Insights

Surge in clean-label demand

Consumer rejection of synthetic additives is driving faster reformulation timelines across packaged foods, beverages, and personal care products. In North America, clean-label claims are increasingly featured in new food and beverage launches. Retailers are enforcing ingredient transparency, and brands face the risk of delisting if they fail to disclose the origins or processing methods of botanical extracts. This trend is particularly prominent in the European Union, where the "Farm to Fork" strategy and the proposed "Front-of-Pack Nutrition Labelling" regulation require manufacturers to validate "natural" claims through third-party certifications. This has increased demand for organic-certified and non-GMO botanical extracts. The clean-label movement is also transforming the demand for color extracts. As synthetic dyes are banned in various regions, formulators are opting for alternatives such as anthocyanins from purple carrots, spirulina-derived phycocyanin, and turmeric-based curcumin. However, these natural options present challenges, including higher costs and stability issues in acidic or high-temperature environments.

Expansion of nutraceutical regulations

Regulatory clarity is enhancing market access for botanical supplements, but compliance complexities continue to challenge smaller players. In September 2024, the FDA released updated guidance on new dietary ingredients, specifying pre-market notification requirements for botanical extracts not previously marketed in the U.S. This update reduces uncertainty for formulators introducing novel phytochemicals. In Europe, the European Food Safety Authority revised its Novel Foods Compendium in April 2025, creating a centralized database of botanical safety assessments to simplify authorization pathways for extracts. For example, yellow tomato extract received approval in November 2025 for use in food supplements at doses up to 30 milligrams per day. Similarly, in 2024, India's Food Safety and Standards Authority introduced updated labeling standards for nutraceuticals, requiring batch-specific testing for heavy metals, pesticide residues, and microbial contaminants. While these standards raise quality benchmarks, they also increase compliance costs for domestic manufacturers. These regulatory changes validate botanical extracts in mainstream health channels but impose significant testing and documentation costs, which tend to benefit vertically integrated multinationals over regional suppliers.

Raw-material price volatility

In 2024, Madagascar's vanilla plantations suffered significant damage due to a cyclone, which, combined with speculative hoarding by intermediaries, caused a sharp increase in vanilla prices. This price surge compelled flavor houses to adapt by either utilizing synthetic vanillin as a substitute or exploring alternative sourcing options in regions such as Uganda and Papua New Guinea. At the same time, climate change is altering the geographic viability of coffee-cherry cultivation, leading to supply constraints for this increasingly popular ingredient used in energy drinks and nootropic supplements. Projections indicate a decline in arabica coffee yields in Brazil, further exacerbating these challenges. In response to such disruptions, companies like Dohler and Martin Bauer are adopting vertical integration strategies. They are investing in contract farming and establishing agroforestry partnerships to ensure a stable and predictable supply over the long term. However, smaller formulators, constrained by limited financial resources, are unable to implement similar strategies and remain highly susceptible to the volatility of spot-market pricing.

Other drivers and restraints analyzed in the detailed report include:

- Growth of vegan and plant-based diets

- Advances in green extraction technologies

- Adulteration and quality concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, herbal and botanical extracts accounted for 36.02% of the plant extract market share. Turmeric, standardized to 95% curcuminoids, and ashwagandha, containing 5% withanolides, dominate the segment for stress and inflammation products. Increased raw material production strengthens the supply chain. For instance, India's turmeric production rose from 1.02 million metric tons in 2024 to 1.20 million metric tons in 2025, according to the Ministry of Agriculture and Farmers Welfare. Meanwhile, essential oils are projected to register the fastest growth in the plant extract market, with an 8.10% CAGR. This growth is driven by antimicrobial oregano and thyme oils replacing sodium benzoate in clean-label meats and rising demand for lavender and peppermint due to their integration into functional beverages.

As consumer preference shifts away from synthetic flavors, oleoresins are increasingly used in snack coatings. Additionally, phytochemical isolates like resveratrol are securing a premium position in clinical nutrition. Natural color extracts from spirulina, paprika, and beetroot are gaining momentum following regulatory bans on Allura Red AC in the EU. However, supply chain vulnerabilities persist due to the geographic concentration of sandalwood, frankincense, and vanilla.

Herbs and spices accounted for 51.89% of the 2025 volumes, underscoring their deep-rooted significance in Ayurveda and Traditional Chinese Medicine (TCM). Yet, fruits and vegetables are set to surge ahead, boasting an impressive 8.36% CAGR. This uptick is bolstered by a steady supply of raw materials, highlighted by Brazil's USDA Foreign Agricultural Service reporting the country's orange production at a notable 13.5 million metric tons. Meanwhile, extracts from anthocyanin-rich blueberries and elderberries are being integrated into formulations targeting cardiovascular and cognitive health. Additionally, citrus waste streams are now being transformed into valuable products like hesperidin, d-limonene, and pectin, turning what was once a landfill cost into a profitable venture.

Tomato pomace, a by-product of tomato processing, is being effectively converted into lycopene, which is widely recognized for its benefits in sun-care and prostate health applications. This innovation is significantly contributing to the expansion of the market for fruit-derived plant extracts. To mitigate the challenges posed by seasonality, companies are increasingly investing in advanced technologies such as freeze-drying tunnels and cold-chain logistics. These investments are critical in ensuring a stable and uninterrupted supply of raw materials, thereby supporting the sustained growth of the market.

The Plant Extract Market Report is Segmented by Product Type (Essential Oils, Oleoresins, and More), Source (Herbs and Spices, Fruits and Vegetables, Flowers, and More), Form (Powder, and More), Application (Food and Beverages, Dietary Supplements and Functional Foods, and More), and Geography (North America, Europe, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Geography Analysis

In 2025, North America contributed 36.03% of global revenue, driven by the U.S.'s USD 60 billion dietary-supplement market. Canada's natural-health-products sector further supported the demand for standardized botanical extracts, emphasizing transparent supply chains and third-party certifications. The FDA introduced an updated botanical-guidance framework in September 2024, clarifying new-dietary-ingredient notification requirements. This update reduced regulatory uncertainties for formulators introducing novel botanicals like CBD, lion's mane mushroom, and sea moss. Private-equity activity surged in 2025 and 2026, highlighted by The Riverside Company's acquisition of Western Botanicals in February 2026 and Monterey Bay Herb Co.'s purchase of NP Nutra. These developments reflected investor confidence in consolidation-driven margin expansion and cross-selling opportunities. Although Mexico's botanical-extract sector is smaller, its proximity to U.S. markets and lower labor costs provide advantages. Companies such as Canurta Naturals are deploying mobile extraction labs to process cannabis and hemp biomass on-site, cutting transportation costs and preserving volatile terpenes.

Europe is projected to grow at 8.78% through 2031, marking the fastest regional growth rate. This growth is supported by the European Food Safety Authority's (EFSA) Novel Foods authorizations and increasing consumer demand for organic-certified, traceable ingredients. In April 2025, the EFSA updated its Compendium of Botanicals, listing over 1,600 plant species with safety assessments. This update aims to streamline authorization pathways and reduce time-to-market for novel extracts. For example, yellow tomato extract was authorized in November 2025 for use in food supplements at doses of up to 30 milligrams per day. Its regulatory approval required toxicological studies, allergenicity assessments, and nutritional-impact analyses. Germany, the largest market in Europe, leads in herbal medicinal products. Botanical extracts such as St. John's wort, valerian, and ginkgo biloba are reimbursed under statutory health insurance for specific indications, creating a pharmaceutical-grade supply chain distinct from dietary supplements. The UK, in its post-Brexit phase, continues to align with EU Novel Foods regulations while exploring faster approval pathways for botanicals with established safety records in Commonwealth nations. Meanwhile, France and Italy are prioritizing organic and biodynamic certifications. Consumers in these countries are willing to pay 20-30% premiums for Ecocert and Demeter-certified botanical extracts, driving demand for regenerative-agriculture sourcing models.

Asia-Pacific, South America, and the Middle East and Africa are emerging as key growth regions in the botanical extract market. China and India are playing dual roles as major producers and expanding consumer markets. China's Traditional Chinese Medicine sector, valued at over USD 150 billion, is shifting from raw-herb dispensing to standardized extract formulations. This transition is supported by modernization initiatives from the National Medical Products Administration and the enforcement of Good Manufacturing Practices. In India, the botanical-extract industry, concentrated in Gujarat, Maharashtra, and Tamil Nadu, supplies global markets with turmeric, ashwagandha, and Bacopa monnieri extracts. However, the industry faces challenges related to quality control and adulteration, which impact export competitiveness. Thailand and Indonesia are positioning themselves as cost-effective sourcing hubs for tropical botanicals such as mangosteen, moringa, and kratom, leveraging favorable climates and government export-promotion programs. Brazil's biodiversity, encompassing the Amazon rainforest and Cerrado savanna, offers significant potential for novel botanical extracts like acai, guarana, and copaiba oil. However, the lack of sustainable-sourcing certifications and underdeveloped indigenous-rights frameworks poses reputational risks for multinational buyers sourcing from Brazil.

- Givaudan SA

- DSM-Firmenich AG

- Symrise AG

- International Flavors and Fragrances Inc.

- Dohler GmbH

- Kalsec Inc.

- Indena SpA

- Archer Daniels Midland Company

- Martin Bauer Group

- Sensient Technologies Corp.

- Ransom Naturals Ltd.

- Frutarom Industries Ltd.

- Arjuna Natural Pvt. Ltd.

- Blue Sky Botanics Ltd.

- Botanica GmbH

- Vidya Herbs Pvt. Ltd.

- Nutra Green Biotechnology Co., Ltd.

- Shaanxi Jiahe Phytochem

- Nexira SAS

- PT Indesso Aroma

- Sabinsa Corporation

- Layn Natural Ingredients Corp.

- OmniActive Health Technologies

- PureCircle (by Ingredion)

- Xi'an Shengtian Bio-chemical Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in clean-label demand

- 4.2.2 Expansion of nutraceutical regulations

- 4.2.3 Growth of vegan and plant-based diets

- 4.2.4 Advances in green extraction technologies

- 4.2.5 Commercial biorefinery-driven agri-waste valorization

- 4.2.6 Integration of AI-led phytochemical discovery pipelines

- 4.3 Market Restraints

- 4.3.1 Raw-material price volatility

- 4.3.2 Adulteration and quality concerns

- 4.3.3 Regulatory inconsistencies worldwide

- 4.3.4 Limited clinical-efficacy data

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE AND VOLUME)

- 5.1 Product Type

- 5.1.1 Essential Oils

- 5.1.2 Oleoresins

- 5.1.3 Herbal and Botanical Extracts

- 5.1.4 Phytochemical Isolates

- 5.1.5 Natural Color Extracts

- 5.1.6 Flavour and Fragrance Extracts

- 5.2 By Source

- 5.2.1 Herbs and spices

- 5.2.2 Fruits and vegetables

- 5.2.3 Flowers

- 5.2.4 Roots and Rhizomes

- 5.2.5 Seeds and Grains

- 5.3 By Form

- 5.3.1 Powder

- 5.3.2 Liquid

- 5.3.3 Crystals and Granules

- 5.4 By Application

- 5.4.1 Food and Beverages

- 5.4.2 Dietary Supplements and Functional Foods

- 5.4.3 Pharmaceuticals

- 5.4.4 Cosmetics and Personal Care

- 5.4.5 Animal Nutrition

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 United Kingdom

- 5.5.2.2 Germany

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Russia

- 5.5.2.7 Sweden

- 5.5.2.8 Belgium

- 5.5.2.9 Poland

- 5.5.2.10 Netherlands

- 5.5.2.11 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 Thailand

- 5.5.3.5 Singapore

- 5.5.3.6 Indonesia

- 5.5.3.7 South Korea

- 5.5.3.8 Australia

- 5.5.3.9 New Zealand

- 5.5.3.10 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Colombia

- 5.5.4.4 Chile

- 5.5.4.5 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 South Africa

- 5.5.5.3 Saudi Arabia

- 5.5.5.4 Nigeria

- 5.5.5.5 Egypt

- 5.5.5.6 Morocco

- 5.5.5.7 Turkey

- 5.5.5.8 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Givaudan SA

- 6.4.2 DSM-Firmenich AG

- 6.4.3 Symrise AG

- 6.4.4 International Flavors and Fragrances Inc.

- 6.4.5 Dohler GmbH

- 6.4.6 Kalsec Inc.

- 6.4.7 Indena SpA

- 6.4.8 Archer Daniels Midland Company

- 6.4.9 Martin Bauer Group

- 6.4.10 Sensient Technologies Corp.

- 6.4.11 Ransom Naturals Ltd.

- 6.4.12 Frutarom Industries Ltd.

- 6.4.13 Arjuna Natural Pvt. Ltd.

- 6.4.14 Blue Sky Botanics Ltd.

- 6.4.15 Botanica GmbH

- 6.4.16 Vidya Herbs Pvt. Ltd.

- 6.4.17 Nutra Green Biotechnology Co., Ltd.

- 6.4.18 Shaanxi Jiahe Phytochem

- 6.4.19 Nexira SAS

- 6.4.20 PT Indesso Aroma

- 6.4.21 Sabinsa Corporation

- 6.4.22 Layn Natural Ingredients Corp.

- 6.4.23 OmniActive Health Technologies

- 6.4.24 PureCircle (by Ingredion)

- 6.4.25 Xi'an Shengtian Bio-chemical Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK