PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043940

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043940

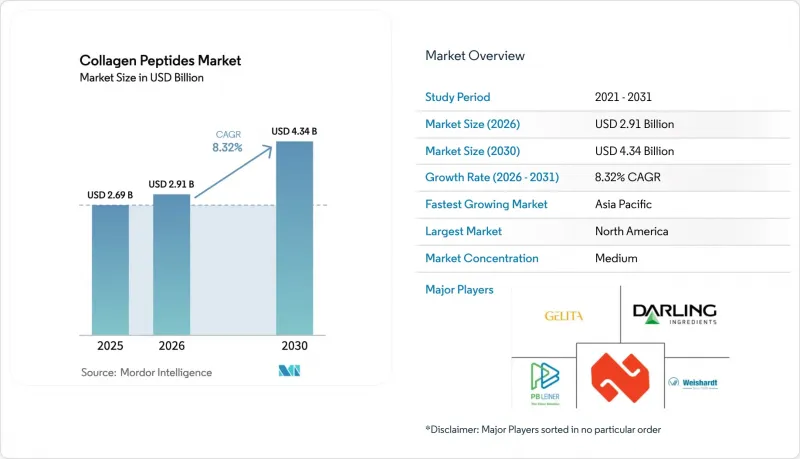

Collagen Peptides - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The collagen peptides market size is expected to grow from USD 2.69 billion in 2025 to USD 2.91 billion in 2026 and is forecast to reach USD 4.34 billion by 2031 at 8.32% CAGR over 2026-2031.

Aging populations, a heightened emphasis on preventive healthcare, and a growing consumer interest in beauty-enhancing supplements drive this growth. The market demonstrates its strength through diverse applications, expanding beyond traditional pharmaceutical uses into sports nutrition and cosmeceuticals, both of which command higher price points. Older consumers increasingly seek products for joint health, skin elasticity, and bone strength, making the aging demographic trend a key driver of market growth. Health-conscious consumers have incorporated collagen supplements into their daily wellness routines, propelled by the preventive healthcare movement. Additionally, the rising "beauty-from-within" trend has fueled demand for collagen-infused products across various categories, including beverages, supplements, and functional foods.

Global Collagen Peptides Market Trends and Insights

Rising consumer awareness of skin health, and beauty-from-within products

Increasing consumer awareness around skin health and the growing popularity of "beauty-from-within" solutions are significantly supporting the expansion of the collagen peptides market. Consumers are shifting toward ingestible products that promote skin hydration, elasticity, and overall appearance from within, rather than relying solely on topical applications. This trend is particularly strong among younger and middle-aged demographics seeking preventative and long-term skincare benefits. Collagen peptides are widely recognized for their role in improving skin structure, which has boosted their incorporation into supplements, functional foods, and beverages. Social media influence, wellness trends, and increased access to product information are further amplifying consumer interest in these solutions. Brands are capitalizing on this momentum by launching innovative, beauty-focused collagen formulations enriched with vitamins and antioxidants. The convergence of nutrition and personal care is reshaping consumer preferences toward holistic wellness approaches.

Surging demand for functional foods and nutraceuticals

The increasing demand for functional foods and nutraceuticals is playing a pivotal role in expanding the collagen peptides market, as consumers seek products that offer added health benefits beyond basic nutrition. There is a growing preference for foods and beverages that support specific functions such as joint health, skin vitality, muscle recovery, and overall wellness. Collagen peptides are widely incorporated into protein bars, fortified drinks, dietary supplements, and ready-to-consume products due to their versatility and proven health benefits. This trend is strongly supported by rising health consciousness, aging populations, and an increased focus on preventive healthcare. Manufacturers are continuously innovating with new formulations, flavors, and delivery formats to enhance consumer appeal and convenience. The integration of collagen into everyday consumables has made it easier for consumers to incorporate it into their daily routines.

High production cost and raw-material price swings

High production costs and fluctuations in raw material prices pose a significant challenge to the growth of the collagen peptides market. The production process involves multiple stages, including sourcing animal-based raw materials such as bovine hides, fish skins, and bones, followed by complex extraction and hydrolysis processes, all of which contribute to elevated manufacturing expenses. Price volatility in raw materials, often influenced by supply chain disruptions, livestock availability, and environmental factors, further adds uncertainty to production planning and cost structures. These fluctuations can impact profit margins for manufacturers and lead to inconsistent pricing for end consumers. Smaller and mid-sized players are particularly affected, as they may lack the scale to absorb cost variations effectively. Additionally, maintaining quality and regulatory compliance increases operational costs, especially for premium and certified products. As a result, higher prices may limit consumer accessibility in price-sensitive markets.

Other drivers and restraints analyzed in the detailed report include:

- Growing aging population driving joint and bone health supplementation

- Increasing use in food and beverage applications (beverages, bars, dairy)

- Concerns over animal sourcing and sustainability issues

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Bovine collagen held the largest share of the collagen peptides market in 2025, accounting for 42.18% of total revenue, due to its widespread availability, cost-effectiveness, and established presence in the health and wellness industry. It is commonly used in dietary supplements, functional foods, beverages, and nutraceuticals, making it a versatile and highly adopted source. Consumers increasingly choose bovine collagen for its proven benefits in supporting skin elasticity, joint health, and bone strength. The high protein content and compatibility with various product formats, including powders, capsules, and fortified drinks, further reinforce its market dominance. Additionally, extensive research and clinical evidence have strengthened consumer confidence in bovine collagen products. Established brands continue to leverage these advantages by expanding product portfolios and emphasizing the efficacy of bovine-derived collagen.

In contrast, marine collagen is projected to be the fastest-growing source segment, with a robust CAGR of 9.14% through 2031, driven by increasing demand for premium, high-bioavailability collagen products. Derived from fish and other marine organisms, it is perceived to offer superior absorption and enhanced efficacy compared to other sources. Marine collagen is particularly popular in the beauty and skincare sector, where it is marketed for its ability to improve skin hydration, elasticity, and overall appearance. Sustainability and eco-friendly sourcing practices also contribute to its rising appeal among environmentally conscious consumers. The segment is witnessing innovation through specialized formulations, flavored powders, and ready-to-drink beverages, expanding its reach to younger and health-focused demographics.

The Collagen Peptides Market Report is Segmented by Source (Bovine, Porcine, Marine, Poultry, Others), Form (Dry and Liquid), Application (Food and Beverages, Supplements, Cosmetics and Personal Care, Pharmaceuticals and Medical, Animal Nutrition and Pet Food), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America led the collagen peptides market in 2025, capturing 37.69% of total revenue, driven by strong consumer awareness of health, wellness, and anti-aging benefits. The region benefits from high disposable income, well-established dietary supplement markets, and a strong presence of leading global collagen brands. Consumers in the U.S. and Canada increasingly incorporate collagen into functional foods, beverages, and personal care products, reflecting the growing emphasis on preventive health and beauty. The FDA's guidelines on new dietary ingredients provide a clear regulatory environment that facilitates product development and market growth. Additionally, strong marketing campaigns highlighting the efficacy of collagen for skin, joint, and bone health have helped boost adoption.

In contrast, Asia-Pacific is projected to be the fastest-growing region, expected to expand at a CAGR of 9.48% through 2031, driven by rising disposable incomes, urbanization, and increasing health consciousness. Growing awareness of collagen's benefits for skin, hair, and joint health is particularly influencing demand among younger, urban populations. The expansion of e-commerce and modern retail channels has improved accessibility to collagen peptides across countries like China, Japan, South Korea, and India. Additionally, the rise of beauty-from-within trends, along with the growing popularity of functional foods and beverages, is fueling adoption. International and local brands are actively launching region-specific formulations and flavors to appeal to diverse consumer preferences.

Other regions, including Europe, South America, and the Middle East and Africa, also contribute significantly to the collagen peptides market, albeit at a more moderate pace. Europe shows steady growth, supported by a mature health and wellness culture, rising demand for functional foods, and premium collagen-based cosmetics. The European Food Safety Authority's updated novel food guidance provides clarity for emerging collagen applications. South America is gradually expanding as urbanization and consumer awareness of nutrition and beauty supplements increase, with countries like Brazil and Argentina showing notable adoption. The Middle East and Africa region is emerging, driven by rising disposable income, increased health awareness, and growing retail and e-commerce penetration. Across these regions, brands are focusing on product diversification, localized formulations, and marketing campaigns to boost penetration.

- Darling Ingredients

- Gelita AG

- Nitta Gelatin Inc.

- PB Gelatins GmbH

- Weishardt Group

- Tessenderlo Group NV

- Lapi Gelatine S.p.A.

- Gelnex Industria e Comercio Ltda.

- Junca Gelatines S.L.

- Trobas Gelatine B.V.

- Ewald-Gelatine GmbH

- Nippi, Inc.

- Foodmate Co., Ltd.

- Baotou Dongbao Bio-Tech Co., Ltd.

- Hangzhou Nutrition Biotechnology Co., Ltd.

- Jilin Aodong Pharmaceutical Group Co., Ltd.

- Great Lakes Gelatin Company

- Titan Biotech Limited

- Amicogen, Inc.

- Norland Products Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising consumer awareness of skin health, and beauty-from-within products

- 4.2.2 Surging demand for functional foods and nutraceuticals

- 4.2.3 Growing aging population driving joint and bone health supplementation

- 4.2.4 Increasing use in food and beverage applications (beverages, bars, dairy)

- 4.2.5 Growth in dietary supplements and ingestible beauty products

- 4.2.6 Expanding applications in pharmaceuticals and medical nutrition

- 4.3 Market Restraints

- 4.3.1 High production cost and raw-material price swings

- 4.3.2 Concerns over animal sourcing and sustainability issues

- 4.3.3 Regulatory challenges across regions for health claims

- 4.3.4 Fluctuations in raw material supply

- 4.4 Supply Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Source

- 5.1.1 Bovine

- 5.1.2 Porcine

- 5.1.3 Marine

- 5.1.4 Poultry

- 5.1.5 Others

- 5.2 By Form

- 5.2.1 Dry

- 5.2.2 Liquid

- 5.3 By Application

- 5.3.1 Food and Beverages

- 5.3.2 Supplements

- 5.3.3 Cosmetics and Personal Care

- 5.3.4 Pharmaceuticals and Medical

- 5.3.5 Animal Nutrition and Pet Food

- 5.4 Segmentation by Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.1.4 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 Italy

- 5.4.2.4 France

- 5.4.2.5 Spain

- 5.4.2.6 Netherlands

- 5.4.2.7 Poland

- 5.4.2.8 Belgium

- 5.4.2.9 Sweden

- 5.4.2.10 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 Indonesia

- 5.4.3.6 South Korea

- 5.4.3.7 Thailand

- 5.4.3.8 Singapore

- 5.4.3.9 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Chile

- 5.4.4.5 Peru

- 5.4.4.6 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 South Africa

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 United Arab Emirates

- 5.4.5.4 Nigeria

- 5.4.5.5 Egypt

- 5.4.5.6 Morocco

- 5.4.5.7 Turkey

- 5.4.5.8 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials (if available), Strategic Information, Market Rank/Share, Products, Recent Developments)

- 6.4.1 Darling Ingredients

- 6.4.2 Gelita AG

- 6.4.3 Nitta Gelatin Inc.

- 6.4.4 PB Gelatins GmbH

- 6.4.5 Weishardt Group

- 6.4.6 Tessenderlo Group NV

- 6.4.7 Lapi Gelatine S.p.A.

- 6.4.8 Gelnex Industria e Comercio Ltda.

- 6.4.9 Junca Gelatines S.L.

- 6.4.10 Trobas Gelatine B.V.

- 6.4.11 Ewald-Gelatine GmbH

- 6.4.12 Nippi, Inc.

- 6.4.13 Foodmate Co., Ltd.

- 6.4.14 Baotou Dongbao Bio-Tech Co., Ltd.

- 6.4.15 Hangzhou Nutrition Biotechnology Co., Ltd.

- 6.4.16 Jilin Aodong Pharmaceutical Group Co., Ltd.

- 6.4.17 Great Lakes Gelatin Company

- 6.4.18 Titan Biotech Limited

- 6.4.19 Amicogen, Inc.

- 6.4.20 Norland Products Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK