PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043946

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043946

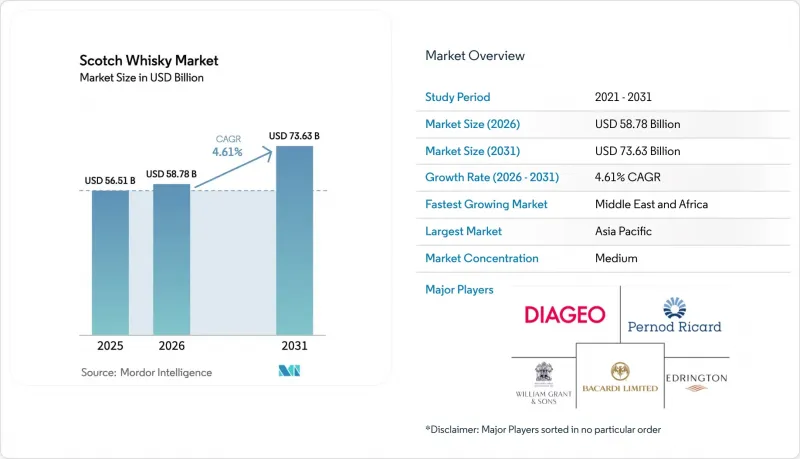

Scotch Whisky - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The scotch whisky market size was valued at USD 56.51 billion in 2025 and is estimated to grow from USD 58.78 billion in 2026 to reach USD 73.63 billion by 2031, at a CAGR of 4.61% during the forecast period (2026-2031).

The global demand for Scotch whisky has increased due to growing consumer preference for premium and luxury spirits. Consumers are choosing high-quality, authentic spirits with established heritage, making Scotch whisky a prominent choice in the premium alcoholic beverages market. This trend is notable in emerging markets, where increased disposable incomes enable consumers to purchase premium spirits. The popularity of whisky-based cocktails has created new consumption opportunities and attracted younger consumers, especially millennials seeking distinctive drinking experiences. Growth in 2026 reflects consistent premium adoption, stronger digital sales models, and resilient brand equity that supports pricing power across channels.

Global Scotch Whisky Market Trends and Insights

Premiumization and luxury positioning

Premium assortments gain traction as consumers seek provenance, aged statements, and limited releases that carry stronger pricing power and brand storytelling. This tilt supports higher average tickets in travel retail and flagship venues, where curated ranges and giftable formats lift value outcomes for the Scotch whisky market. Diageo exemplified this approach by establishing the Diageo Luxury Group in November 2024, consolidating spirits priced above USD 100 under one strategic unit. This restructuring allows targeted investment in ultra-premium offerings, including Johnnie Walker's Vault, which provides custom blending services starting at GBP 50,000. The luxury market has expanded beyond traditional consumption into investment opportunities, particularly through whisky cask ownership. The premium spirits segment's potential is demonstrated by American whisky market data, where high-end and premium brands recorded 274% revenue growth since 2003, while super-premium brands grew by 2,150% . This shift toward premium offerings helps companies offset regulatory costs while building long-term value in wealthy consumer segments.

Rising demand for single malt and craft expressions

Single malts are set to grow faster than the category baseline as consumers favor clear provenance, distillery identity, and cask nuance over price-led propositions. The Scotch whisky market channels that demand through tasting flights, bartender guidance, and specialist retail that reduces choice overload and guides shoppers toward signature malts. Younger legal drinking age adults in 2026 are expected to show stronger engagement with beverage alcohol than in 2023, which broadens the addressable base for entry to premium malts and builds confidence to explore cask finishes over time. As education improves and online content deepens category knowledge, buyers move more fluidly between accessible malts and higher-end releases, which sustains the mix upgrade within the Scotch whisky market. This reinforces a portfolio strategy that balances volume blends with targeted single malt expansion where urban demand is concentrated.

Volatile excise duties and trade tariffs

The Scotch whisky market faces significant regulatory challenges, primarily through tax policy changes that affect consumer pricing and demand. The United Kingdom's recent double-digit tax increase on Scotch whisky led to decreased sales volumes and resulted in daily revenue losses of over GBP 500,000 for the United Kingdom Exchequer . The potential reimposition of 25% United States tariffs on Scotch whisky within 18 months creates additional uncertainty for the industry's primary export market. However, the UK-India Free Trade Agreement presents growth opportunities by reducing import duties from 150% to 75% initially, followed by a further reduction to 40% over ten years. Companies are responding to these regulatory uncertainties by implementing adaptable pricing strategies and expanding their market presence across multiple regions. Travel retail and on-premise discovery help maintain premium momentum despite policy noise, since occasion-based buying supports willingness to trade up in curated environments in 2026.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of e-commerce and DTC logistics

- Product innovation and flavors

- Competition from other spirits

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Blended Scotch commanded 58.23% of the Scotch whisky market share in 2025, reflecting the breadth of distribution, affordability, and brand familiarity across large retail and on-trade networks. The category's strength lies in its ability to offer consistent quality across various price points, from entry-level to premium expressions, making it accessible to a diverse consumer base across global markets. Single malt Scotch whisky is projected to grow at a 5.55% CAGR during 2026-2031, driven by increasing consumer sophistication and willingness to explore premium offerings. This growth is supported by substantial investments in production capacity, aging facilities, and specialized distillation processes, enabling distilleries to meet the rising demand for high-quality single malt expressions.

Single grain Scotch whisky holds a distinctive position in the spirits industry, primarily serving as a crucial component in blended whisky expressions. There's a growing consumer awareness and appreciation for the craftsmanship involved in whisky production, leading to increased interest in various whisky categories, including Single Grain Scotch. The market is also benefiting from the premiumization trend, where consumers demonstrate a willingness to invest in authentic, high-quality spirits. The segment's growth is further supported by its versatility in blending, making it an essential ingredient for master blenders creating premium blended Scotch whiskies.

The 12-15 years band held 40.07% of 2025 consumption, a middle ground that travels well across channels and serves as a familiar entry point in the Scotch whisky market. This category maintains a stable supply through established production cycles and effective inventory management, enabling consistent market availability to meet consumer demand. The below 12 Years category functions as an entry point for new consumers and price-sensitive buyers, while the 16-20 Years segment targets dedicated enthusiasts seeking extended maturation profiles. The 21-30 Years category focuses on collectors and special occasion purchases, with limited availability supporting premium pricing.

Whiskies aged below 24 years are forecast to expand at 5.21% CAGR through 2031, helped by cocktail adoption and bartender recommendations that favor flavor profiles built for mixing and flights. The growth in this segment demonstrates whisky's emergence as an alternative investment asset, though investors face potential risks due to regulatory uncertainties in cask ownership. The age segmentation distribution reflects historical production limitations, prompting companies to increase production capacity to address future demand for aged expressions.

The Scotch Whisky Market is Segmented by Category (Single Malt, Single Grain, Blended Malt, and More), Age (Below 12 Years, 12-15 Years, 16-20 Years, 21-30 Years, Over 30 Years), Price (Mass and Premium), Distribution Channel (Off-Trade, On-Trade), and Geography (North America, Europe, Asia-Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Tons).

Geography Analysis

Asia-Pacific holds the largest market share at 32.04% in 2025, primarily due to China's expanding whisky market. The region's market position stems from increasing disposable incomes, rapid urbanization, and evolving consumer preferences toward Western spirits. Japan's mature whisky market creates a natural pathway for Scotch whisky adoption, while India presents substantial growth opportunities despite existing tariff restrictions. Australia and South Korea maintain consistent demand, and emerging economies such as Indonesia and Thailand demonstrate growth potential as their markets develop.

The Middle East and Africa region is projected to grow at 5.29% CAGR during 2026-2031, supported by middle-class population growth and enhanced distribution networks. The region's expansion reflects economic progress and evolving attitudes toward alcohol consumption in markets where it is permitted. South Africa dominates regional consumption, while the United Arab Emirates functions as the primary distribution center for the Middle East. In addition, South America demonstrates consistent growth prospects, with Brazil's large consumer base and strengthening economy driving the market, while Argentina and Chile develop premium market segments.

Europe remains a key market for Scotch whisky due to its historical significance, established consumer base, and cultural affinity for aged spirits. The region's traditional appreciation for Scotch whisky is evident through its extensive distribution networks, premium positioning in retail outlets, and strong presence in both on-trade and off-trade channels. European consumers demonstrate sophisticated preferences for single malts and aged blends, supported by well-established tasting clubs and whisky societies. However, the region faces regulatory challenges, including changes in labeling requirements, taxation policies, and trade agreements that impact market dynamics.

- Diageo plc

- Pernod Ricard S.A.

- Bacardi Limited

- William Grant & Sons Ltd.

- Edrington Group

- Suntory Holdings Limited

- Emperador Inc.

- Brown-Forman Corporation

- La Martiniquaise-Bardinet

- Loch Lomond Group

- Thai Beverage Plc

- Ian Macleod Distillers Limited

- Gordon & MacPhail

- Douglas Laing & Co.

- Angus Dundee Distillers Plc

- Arbikie Distilling Limited

- Isle of Arran Distillers Ltd

- R&B Distillers Limited (Isle of Raasay Distillery)

- The GlenAllachie Distillers Company Limited

- Wemyss Family Spirits Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Premiumization and luxury positioning

- 4.2.2 Rising demand for single malt and craft expressions

- 4.2.3 Expansion of e-commerce and DTC logistics

- 4.2.4 Product innovation and flavors

- 4.2.5 Whisky tourism and experiential offerings

- 4.2.6 Influence of cocktail culture and on-premise trends

- 4.3 Market Restraints

- 4.3.1 Volatile excise duties and trade tariffs

- 4.3.2 Competition from other spirits

- 4.3.3 Counterfeiting and illicit trade

- 4.3.4 Environmental and sustainability pressures

- 4.4 Consumer Behaviour Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitute Products

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE and VOLUME)

- 5.1 By Category

- 5.1.1 Single malt

- 5.1.2 Single grain

- 5.1.3 Blended malt

- 5.1.4 Blended grain

- 5.1.5 Blended

- 5.2 By Age

- 5.2.1 Below 12 years

- 5.2.2 12-15 years

- 5.2.3 16-20 years

- 5.2.4 21-30 years

- 5.2.5 Over 30 years

- 5.3 By Price

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 By Distribution Channel

- 5.4.1 Off-trade

- 5.4.2 On-trade

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 Italy

- 5.5.2.4 France

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Poland

- 5.5.2.8 Belgium

- 5.5.2.9 Sweden

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 Indonesia

- 5.5.3.6 South Korea

- 5.5.3.7 Thailand

- 5.5.3.8 Singapore

- 5.5.3.9 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 South Africa

- 5.5.4.2 United Arab Emirates

- 5.5.4.3 Nigeria

- 5.5.4.4 Egypt

- 5.5.4.5 Morocco

- 5.5.4.6 Turkey

- 5.5.4.7 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Colombia

- 5.5.5.4 Chile

- 5.5.5.5 Peru

- 5.5.5.6 Rest of South America

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Diageo plc

- 6.4.2 Pernod Ricard S.A.

- 6.4.3 Bacardi Limited

- 6.4.4 William Grant & Sons Ltd.

- 6.4.5 Edrington Group

- 6.4.6 Suntory Holdings Limited

- 6.4.7 Emperador Inc.

- 6.4.8 Brown-Forman Corporation

- 6.4.9 La Martiniquaise-Bardinet

- 6.4.10 Loch Lomond Group

- 6.4.11 Thai Beverage Plc

- 6.4.12 Ian Macleod Distillers Limited

- 6.4.13 Gordon & MacPhail

- 6.4.14 Douglas Laing & Co.

- 6.4.15 Angus Dundee Distillers Plc

- 6.4.16 Arbikie Distilling Limited

- 6.4.17 Isle of Arran Distillers Ltd

- 6.4.18 R&B Distillers Limited (Isle of Raasay Distillery)

- 6.4.19 The GlenAllachie Distillers Company Limited

- 6.4.20 Wemyss Family Spirits Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK