PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043948

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043948

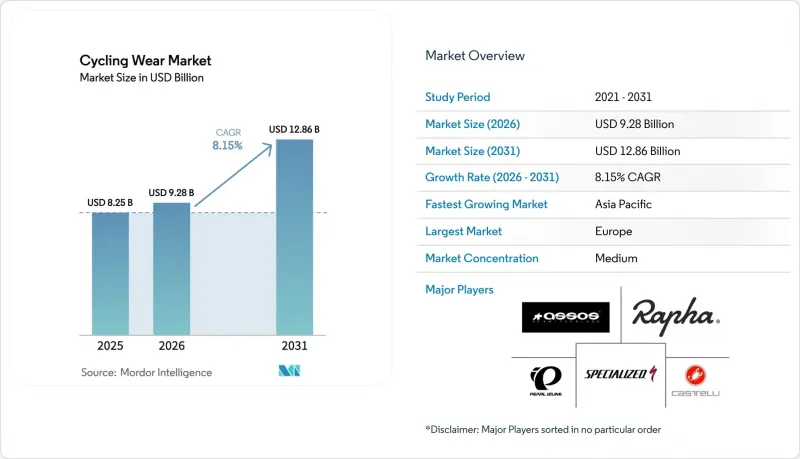

Cycling Wear - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The cycling wear market size is projected to be USD 8.25 billion in 2025, USD 9.28 billion in 2026, and reach USD 12.86 billion by 2031, growing at a CAGR of 8.15% from 2026 to 2031.

Functional demand is widening as governments fund commuter-friendly infrastructure, shifting purchases toward weather-resistant apparel that blends performance and everyday utility. Premiumization is accelerating because smart fabrics and lifestyle positioning justify higher prices even while mass-market volumes dominate. Accessories outpace core garments as riders build modular wardrobes around packable, visibility-focused items. Digital channels grow fastest as festival-driven promotions and direct-to-consumer (DTC) models compress decision cycles into brief, high-traffic events. Challenger brands leverage niche cultural marketing to erode incumbent share, especially in women's and premium lines.

Global Cycling Wear Market Trends and Insights

Rising Health and Fitness Awareness

As cycling increasingly becomes a badge of identity rather than just a pastime, its appeal is broadening from traditional enthusiasts to wellness oriented consumers. A 2025 McKinsey survey highlighted that 51 to 54% of active consumers, especially millennials and Gen Z, see fitness as integral to their identity. This shift in perception is benefiting cycling wear brands that market their products as essential lifestyle items rather than just functional gear. While the World Health Organization warns of a rise in adult physical inactivity from 31% in 2022 to 35% by 2030, translating to 1.8 billion globally, it is also a golden opportunity for brands. By innovating products and engaging at the grassroots level, they can tap into this vast, currently inactive demographic. Shimano's Trail Born initiative, which allocated USD 10 million over a decade to trail development and made inroads into South America and Asia in 2026, underscores the trend. It is a testament to how component manufacturers are bolstering participation infrastructure, inadvertently boosting apparel demand. To entice these previously inactive consumers, brands need to focus on comfort and versatility in their apparel, rather than just race day performance, especially given the 75.42% mass market share noted in 2025.

Growing Popularity of Cycling for Commuting and Recreation Amid Urban Congestion

Urban mobility policies are shifting cycling from a leisure pursuit to a staple mode of transport, fueling a consistent demand for durable, weather-resistant apparel. In 2024, the European Commission's Declaration on Cycling, endorsed by Member States, emphasizes the establishment of safe cycling networks, the integration of bikes with public transport, and the development of e-bike charging infrastructure. This initiative is bolstered by a substantial commitment of EUR 4.5 billion in EU funds, allocated for the 2021 2027 period. A preliminary study by the EU has pinpointed over 900,000 kilometers of existing cycle paths throughout Europe. However, significant regional disparities highlight an uneven maturity in demand. The United Kingdom's Third Cycling and Walking Investment Strategy (CWIS3) aims to boost the number of cycling stages per individual while simultaneously working to reduce cyclist casualties. Active Travel England is set to bolster its technical support starting in 2026. As commuter cycling gains traction, there is a rising preference for versatile apparel that seamlessly transitions from bike rides to office settings. In a notable surge, China's outdoor clothing sales on Douyin skyrocketed by 75.5% year on year from January to October 2024, hitting a remarkable USD 2.4 billion. This uptick underscores the growing allure of functional outdoor wear, particularly cycling commuter apparel, among the digitally savvy consumer base.

High Costs of Advanced Materials Like Carbon Fiber Limit Affordability

Premium material costs create a ceiling on mass-market penetration, particularly in price-sensitive geographies where cycling is transitioning from recreation to transport. While carbon fiber is primarily associated with bicycle frames, advanced technical fabrics incorporating graphene, silver-plated yarns, and specialty polymers face similar cost pressures. The reduced graphene oxide yarns described in peer-reviewed sweat lactate monitoring research cost approximately USD 0.03 per meter at lab scale, but commercial-scale production with consistent quality remains unproven. KPMG's China consumer report noted that mid- and high-end outdoor brands saw faster online growth, with one high-end brand achieving CNY 1.228 billion (approximately USD 170 million) turnover in January-October 2024, up 220% year-on-year, suggesting that affluent consumers will pay premiums for performance.

Other drivers and restraints analyzed in the detailed report include:

- Technological Innovations in Materials for Breathability, Lightness, and Smart Features

- Expanded Cycling Infrastructure and Government Initiatives Supporting Bike Lanes

- Supply Chain Disruptions and Inventory Issues Hinder Reliability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Accessories are forecast to expand at 9.32% CAGR during 2026-2031, outstripping the growth of jerseys and tops despite the latter's 41.28% share in 2025. This divergence reflects the modular purchasing behavior of commuter cyclists, who invest incrementally in visibility gear, packable rain shells, and thermal layers rather than replacing entire wardrobes. Jerseys and tops remain the largest segment because they are the entry point for new cyclists and require frequent replacement due to wear and perspiration exposure. Bottoms and bib-shorts represent a smaller share but command higher per-unit prices due to chamois padding and compression fabrics, making them a margin-accretive category for brands. Jackets and outerwear serve seasonal and weather-specific needs, with demand concentrated in temperate climates where year-round cycling requires layering systems.

The accessories surge is tied to urban cycling's rise, where riders prioritize packability and multi-functionality over race-day aerodynamics. Shimano's February 2026 launch of RIDESCAPE lens options for road, gravel, and trail riders, featuring darkened lenses to reveal surface texture like potholes and seams, illustrates how accessories are evolving into performance-enhancing tools rather than afterthoughts. Although eyewear falls outside apparel, the design philosophy applies to accessories like gloves with touchscreen-compatible fingertips and caps with integrated LED strips. China's Double 11 festival in 2024 saw cycling goggles sales surge 210% year-on-year on Tmall, confirming that accessories benefit disproportionately from promotional events.

Women's cycling wear is projected to grow at 9.27% CAGR through 2031, narrowing the gap with men's 58.33% share recorded in 2025. This acceleration stems from rising female participation in cycling, driven by inclusive infrastructure policies and targeted marketing by brands recognizing women as an underserved demographic. The EU's Declaration on Cycling emphasizes inclusivity and accessibility, with Member States launching tailored programs for women, older adults, and families European Commission, 2025. KPMG's China report noted that women comprised 55.41% of fitness consumers in 2023, indicating that female engagement in active lifestyles is translating into cycling participation. Brands that offer gender-specific fits, extended size ranges, and design aesthetics beyond traditional racing palettes are capturing this growth.

Men's segment retains majority share due to historical participation rates and higher average spending on performance gear, but growth is moderating as the market matures. Children's cycling wear remains a smaller segment, yet it serves as a funnel for long-term brand loyalty if parents introduce cycling early. The UK's CWIS3 targets an increased percentage of children aged 5-10 who usually walk to school, with cycling training programs like Bikeability expanding reach. Children's apparel must balance durability with rapid sizing changes, favoring adjustable designs and value pricing.

The Cycling Wear Market Report is Segmented by Product Type (Jerseys and Tops, Bottoms and Bib-Shorts, Jackets and Outerwear, and Accessories), End User (Men, Women, and Children), Category (Mass and Premium), Distribution Channels (Sports and Athletic Goods Store, Online Retail Channels, Supermarkets/Hypermarkets, and Others), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Europe commanded 40.21% market share in 2025, underpinned by entrenched cycling cultures in the Netherlands, Belgium, Germany, and the UK, where cycling is embedded in daily transport and recreational routines. The European Commission's Declaration on Cycling and the €4.5 billion investment for 2021-2027 are expanding infrastructure beyond core markets into Southern and Eastern Europe, where cycling adoption lags. Lithuania's adoption of its first national cycling strategy in 2024 signals that emerging European markets are entering growth phases, creating opportunities for brands to establish a presence before competition intensifies. The UK's £616 million CWIS3 allocation for 2026-2030 targets measurable increases in cycling stages per person, directly stimulating apparel demand as new cyclists require starter kits and existing riders upgrade seasonal wardrobes. Germany, the Netherlands, and Sweden benefit from high per-capita cycling rates and premium brand concentration, sustaining Europe's leadership despite slower growth relative to Asia-Pacific.

Asia-Pacific is forecast to expand at 9.98% CAGR during 2026-2031, the fastest regional rate, driven by urbanization, infrastructure investment, and rising middle-class incomes in China, India, and Southeast Asia. China's government issued consumption vouchers and sports-promotion policies in 2024, including financial support for sports consumption via China UnionPay and e-CNY use, creating fiscal tailwinds for cycling participation. India's cycling infrastructure remains underdeveloped compared to China, but urban congestion and environmental awareness are driving two-wheeler adoption, with cycling wear benefiting as a secondary effect. Vietnam and Indonesia represent emerging markets where rising incomes and youth populations favor active lifestyles, yet distribution infrastructure and brand awareness remain barriers.

North America, South America, and the Middle East and Africa collectively represent smaller shares but exhibit heterogeneous growth patterns. North America benefits from established recreational cycling and gravel biking trends, with Shimano's February 2026 partnership with the Canyon x DT Swiss All-Terrain Racing team highlighting the gravel segment's momentum Shimano, 2026. The United States and Canada have fragmented cycling infrastructure, with urban centers like Portland and Vancouver leading adoption while suburban and rural areas lag. South America's cycling wear market is nascent, constrained by economic volatility and limited infrastructure, though Shimano's Trail Born expansion into Brazil and Mexico in 2026 signals growing interest. The Middle East and Africa face infrastructure and climate challenges, with cycling concentrated in cooler months and affluent urban enclaves. The UAE and South Africa lead regional adoption, but market scale remains limited compared to Europe and Asia-Pacific.

- Rapha Racing Ltd

- Assos of Switzerland

- Castelli (Manifattura Valcismon)

- Pearl Izumi

- W. L. Gore & Associates (Gore Wear)

- Pentland Brands (Endura)

- POC Sports

- Le Col

- Santini Cycling

- Giordana Cycling

- Ale Cycling

- Jelenew

- Altura

- Proviz Sports

- Fung Sports Ltd

- SRAM (Velocio Apparel)

- Lululemon Athletica (7Mesh)

- Fox Racing

- Adidas AG (Cycling Apparel)

- Decathlon S.A.

- Shimano Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Health And Fitness Awareness

- 4.2.2 Growing Popularity Of Cycling For Commuting And Recreation Amid Urban Congestion

- 4.2.3 Technological Innovations In Materials For Breathability, Lightness, And Smart Features

- 4.2.4 Expanded Cycling Infrastructure And Government Initiatives Supporting Bike Lanes

- 4.2.5 Increased Sports Participation In Road, Mountain, And Gravel Biking

- 4.2.6 Environmental Concerns Promote Sustainable, Eco-Friendly Cycling Products

- 4.3 Market Restraints

- 4.3.1 High Costs Of Advanced Materials Like Carbon Fiber Limit Affordability

- 4.3.2 Supply Chain Disruptions And Inventory Issues Hinder Reliability

- 4.3.3 Presence of Counterfiet Products

- 4.3.4 Stricter micro-fibre shedding regulations

- 4.4 Consumer Behavior Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Jerseys and Tops

- 5.1.2 Bottoms and Bib-shorts

- 5.1.3 Jackets and Outerwear

- 5.1.4 Accessories

- 5.2 By End User

- 5.2.1 Men

- 5.2.2 Women

- 5.2.3 Children

- 5.3 By Category

- 5.3.1 Mass

- 5.3.2 Premium

- 5.4 By Distribution Channels

- 5.4.1 Sports and Athletic Goods Store

- 5.4.2 Online Retail Channels

- 5.4.3 Supermarkets/Hypermarkets

- 5.4.4 Others

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.1.4 Rest of North America

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Netherlands

- 5.5.2.7 Sweden

- 5.5.2.8 Poland

- 5.5.2.9 Belgium

- 5.5.2.10 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 Australia

- 5.5.3.5 South Korea

- 5.5.3.6 Vietnam

- 5.5.3.7 Indonesia

- 5.5.3.8 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Chile

- 5.5.4.4 Peru

- 5.5.4.5 Colombia

- 5.5.4.6 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Ranking Analysis

- 6.4 Company Profiles (Includes Global-level Overview, Market-level Overview, Core Segments, Financials, Strategic Info, Market Rank/Share, Products & Services, Recent Developments)

- 6.4.1 Rapha Racing Ltd

- 6.4.2 Assos of Switzerland

- 6.4.3 Castelli (Manifattura Valcismon)

- 6.4.4 Pearl Izumi

- 6.4.5 W. L. Gore & Associates (Gore Wear)

- 6.4.6 Pentland Brands (Endura)

- 6.4.7 POC Sports

- 6.4.8 Le Col

- 6.4.9 Santini Cycling

- 6.4.10 Giordana Cycling

- 6.4.11 Ale Cycling

- 6.4.12 Jelenew

- 6.4.13 Altura

- 6.4.14 Proviz Sports

- 6.4.15 Fung Sports Ltd

- 6.4.16 SRAM (Velocio Apparel)

- 6.4.17 Lululemon Athletica (7Mesh)

- 6.4.18 Fox Racing

- 6.4.19 Adidas AG (Cycling Apparel)

- 6.4.20 Decathlon S.A.

- 6.4.21 Shimano Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK