PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043953

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043953

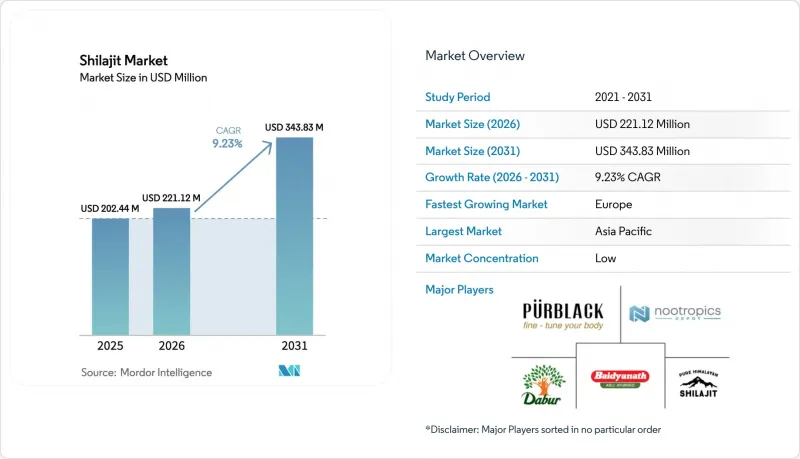

Shilajit - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Shilajit Market is projected to grow significantly, increasing from USD 202.44 million in 2025 to USD 221.12 million in 2026 and reaching USD 343.83 million by 2031, with a CAGR of 9.13% during 2026-2031.

This growth is fueled by rising demand for plant-based adaptogens, clearer regulatory frameworks for fulvic-acid-standardized formulas, and growing consumer interest in healthy aging. Heritage positioning continues to drive growth in the Asia-Pacific region, while clinical validation and clean-label claims are key factors influencing adoption in North America. Furthermore, innovations such as water-soluble powders and gummies have broadened the appeal of shilajit beyond its traditional resin form. Despite these advancements, the market faces quality-control challenges, highlighting the critical need for third-party testing and traceable sourcing to help brands secure a competitive advantage.

Global Shilajit Market Trends and Insights

Increasing popularity of plant-based and vegan supplements positions Shilajit as a natural alternative

Plant-based supplements are transforming the wellness industry as consumers increasingly prioritize transparency in ingredient sourcing, manufacturing processes, and product authenticity. Shilajit, a mineral-pitch resin naturally formed over centuries from decomposed plant matter, has gained prominence as a preferred option for vegan and vegetarian diets, offering a plant-based alternative to animal-derived supplements like collagen or fish oil. Packed with fulvic acid, trace minerals, and antioxidants, Shilajit supports energy production, immune function, and overall health, delivering benefits comparable to synthetic multivitamins. Its Ayurvedic heritage further enhances its appeal in markets where traditional and "natural" remedies are highly valued and often command a premium price. However, ensuring product purity is crucial, as adulteration with fillers or synthetic fulvic acid can undermine consumer trust and compromise its clean-label promise. To address these challenges and differentiate in a competitive market, third-party testing and certifications such as USDA Organic or Non-GMO Project Verified are becoming indispensable for building consumer confidence and trust.

Innovation in product formulations and formats

Shilajit is gaining popularity through innovative formats like gummies, liquid drops, and functional beverages, appealing to Gen-Z's preference for convenience, taste, and compatibility with their specialty diets. In 2024, brands such as Blisque and Angel Gummies launched Shilajit-infused gummies, masking the resin's bitterness with natural sweeteners and fruit extracts, while Purblack introduced its Research Grade Shilajit Resin in October 2025, standardized to >=60% fulvic acid and >=50% dibenzo-a-pyrones, targeting biohackers and performance athletes. Combination formulations are also gaining traction: Shilajit paired with ashwagandha addresses stress and energy in a single SKU, while Shilajit-turmeric blends target inflammation and joint health. Natreon's PrimaVie-a clinically studied, patented Shilajit extract-has become the ingredient of choice for premium brands seeking to substantiate efficacy claims with human trials, a move that aligns with the European Food Safety Authority's stringent health-claim regulations under Regulation (EC) 1924/2006. Advanced encapsulation technologies like liposomal and nanotechnology are improving bioavailability, though high costs limit their use to premium products. This evolution positions Shilajit as a versatile wellness platform, but brands must balance innovation with authenticity to retain traditional consumers who prefer resin as the authentic form.

Heavy metal and mycotoxin contamination risks

Regulatory agencies are intensifying their scrutiny of heavy metal levels in botanical supplements, spotlighting contamination concerns as a significant barrier to market growth. Recent studies have identified thallium concentrations of up to 0.5 µg/g in certain shilajit supplements. Extended exposure to these levels can lead to severe health repercussions, including potential neurological harm. The FDA's "Closer to Zero" initiative, designed to reduce heavy metals in food products, has introduced stringent enforcement benchmarks. Many manufacturers of shilajit grapple with consistent compliance. Research indicates that shilajit contains approximately 65 heavy metals, with dangerous ones like lead, arsenic, cadmium, and mercury present. Alarmingly, some of these metals exceed the permissible limits established by the WHO and the FDA. The contamination challenge is further complicated by geographic variability, as the quality of raw materials and their heavy metal profiles differ markedly across regions. This escalating regulatory scrutiny is pushing consolidation towards manufacturers with advanced testing capabilities and superior sourcing networks. Meanwhile, smaller players, often devoid of a robust quality control framework, encounter significant challenges.

Other drivers and restraints analyzed in the detailed report include:

- Social-media driven awareness in Gen-Z male wellness

- Expansion of e-commerce channels

- Adulteration and unregulated market players

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

In 2025, Standard Grade Shilajit captured a 45.32% market share, underscoring its stronghold in price-sensitive regions like India, Southeast Asia, and the Middle East. Here, consumers lean towards affordability over clinical validation. Typically, Standard-grade products, containing 20-30% fulvic acid and undergoing minimal purification, retail between USD 15-25 for a 30-day supply. In contrast, the Premium Grade is set to grow at a 9.51% CAGR through 2031. This surge is fueled by Western consumers and affluent urban Asians seeking standardized potency, heavy-metal testing, and clinical backing. Natreon's PrimaVie-a patented Shilajit extract boasting >=60% fulvic acid and >=50% dibenzo-a-pyrones-has emerged as the gold standard for premium formulations. Esteemed brands like Nootropics Depot and Purblack have integrated PrimaVie into their flagship offerings. Furthermore, PrimaVie's clinical trials, showcasing boosts in mitochondrial ATP production and exercise performance, align with the evidence premium consumers demand, meeting the European Food Safety Authority's health-claim standards under Regulation (EC) 1924/2006.

As counterfeit products proliferate, the premium segment's growth is a strategic countermeasure. By securing third-party certifications (like NSF, USP, and ISO 17025), ensuring transparent sourcing, and adopting tamper-evident packaging, premium brands carve out a niche that justifies prices 2-3 times higher than standard grades. Purblack's October 2025 debut of Research Grade Shilajit Resin, featuring batch-specific ICP-MS test results and GPS coordinates of collection sites, underscores this trust-centric strategy. Europe's expansion is notable, with the Traditional Herbal Medicinal Product (THR) pathway granting 178 registrations in the UK by 2024. North America mirrors this trend, as California's Proposition 65 lead limits (set at 0.5 micrograms per day) effectively necessitate premium-grade purification. While Standard grade will continue to lead in volume across Asia Pacific-thanks to Ayurvedic traditions and word-of-mouth endorsements-its market share is poised to dwindle. This shift is driven by rising incomes and heightened health awareness, steering consumers towards premium options.

The Shilajit Market Report is Segmented by Grade/Quality (Standard Grade, Premium Grade), Form (Resin, Capsules/Tablets, Powder, Others), Distribution Channel (Supermarkets/Hypermarkets, Pharmacies and Drugstores, Online Retail, Other Retail Distributors), and Geography (North America, Europe, Asia Pacific, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

In 2025, the Asia Pacific held a 61.02% market share, driven by India's role as the largest consumer and sourcing hub for Himalayan Shilajit. The Food Safety and Standards Authority of India's "Ayurveda Aahara" licensing category, introduced on September 1, 2025, reclassified Shilajit as a food supplement, enabling broader distribution through supermarkets and e-commerce. A National Sample Survey revealed that 96% of urban and 95% of rural respondents were aware of AYUSH systems, with nearly 50% spending at least INR 100 annually on AYUSH products. China is emerging as a key market, with traditional Chinese medicine practitioners incorporating Shilajit into kidney health formulations, though regulatory hurdles with the National Medical Products Administration persist. Japan's nascent market is growing as urban professionals seek nootropics and adaptogens like Shilajit to manage stress.

Europe is projected to grow at an 11.01% CAGR through 2031, driven by yoga's mainstreaming, Ayurveda's acceptance, and the Traditional Herbal Medicinal Product (THR) pathway, which enabled 178 registrations in the UK by 2024. Germany and the UK lead adoption, with consumers favoring certified organic, fair-trade Shilajit that meets EU heavy-metal limits under Regulation (EC) 1881/2006. The 2026 India-EU trade agreement reduced tariffs on Ayurvedic exports, allowing Indian brands like Dabur and Baidyanath to compete with European incumbents. Italy's market benefits from integrative medicine practitioners prescribing Shilajit, while France's BELFRIT list creates entry barriers but reduces competition for compliant products. Post-Brexit, the UK's MHRA independently regulates herbal-medicine registrations, adding complexity for brands navigating dual compliance.

North America, led by the U.S. and Canada, is expanding as adaptogens and nootropics gain popularity. The U.S. FDA's DSHEA framework treats Shilajit as a supplement, lowering entry barriers but enabling counterfeit proliferation, while California's Proposition 65 lead limits favor premium-grade products. Canada's NNHPD requires pre-market notification and safety evidence, slowing entry but enhancing trust. South America and the Middle East & Africa remain nascent markets, with growing interest in natural wellness solutions and e-commerce platforms like Mercado Libre and Jumia driving demand. Brazil's ANVISA classifies Shilajit as a novel food requiring pre-market authorization, while the UAE's Ministry of Health and Prevention has approved select products for pharmacy distribution in Dubai and Abu Dhabi.

- Pure Himalayan Shilajit

- Purblack

- Dabur

- Baidyanath

- Nootropics Depot

- aSquared Nutrition

- ACTIZEET

- Angel Gummies

- Blisque

- CHOQ LLC

- Vedikroots

- Dorado Nutrition

- Elm & Rye

- Lotus Blooming Herbs

- Natural Shilajit

- Nootrum

- Pahadi Amrut

- Rasayanam Ayurveda

- Upakarma Ayurveda

- Sunfood

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing popularity of plant-based and vegan supplements positions Shilajit as a natural alternative

- 4.2.2 Innovation in product formulations and formats

- 4.2.3 Social-media driven awareness in Gen-Z male wellness

- 4.2.4 Expansion of e-commerce channels

- 4.2.5 Rising demand for clean-label, ethically sourced Himalayan resins

- 4.2.6 Surge in holistic wellness practices and yoga/Ayurveda adoption worldwide

- 4.3 Market Restraints

- 4.3.1 Counterfeit resin proliferation on online marketplaces

- 4.3.2 Adulteration and unregulated market players

- 4.3.3 Raw material scarcity and geographic dependence

- 4.3.4 Heavy metal and mycotoxin contamination risks

- 4.4 Consumer Demand Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Grade/Quality

- 5.1.1 Standard Grade

- 5.1.2 Premium Grade

- 5.2 By Form

- 5.2.1 Resin

- 5.2.2 Capsules/Tablets

- 5.2.3 Powder

- 5.2.4 Others

- 5.3 By Distribution Channel

- 5.3.1 Supermarkets/Hypermarkets

- 5.3.2 Pharmacies and Drugstores

- 5.3.3 Online Retail

- 5.3.4 Other Retail Distributors

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Rest of North America

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 Italy

- 5.4.2.4 Rest of Europe

- 5.4.3 Asia Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.5 Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Pure Himalayan Shilajit

- 6.4.2 Purblack

- 6.4.3 Dabur

- 6.4.4 Baidyanath

- 6.4.5 Nootropics Depot

- 6.4.6 aSquared Nutrition

- 6.4.7 ACTIZEET

- 6.4.8 Angel Gummies

- 6.4.9 Blisque

- 6.4.10 CHOQ LLC

- 6.4.11 Vedikroots

- 6.4.12 Dorado Nutrition

- 6.4.13 Elm & Rye

- 6.4.14 Lotus Blooming Herbs

- 6.4.15 Natural Shilajit

- 6.4.16 Nootrum

- 6.4.17 Pahadi Amrut

- 6.4.18 Rasayanam Ayurveda

- 6.4.19 Upakarma Ayurveda

- 6.4.20 Sunfood

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK