PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043959

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043959

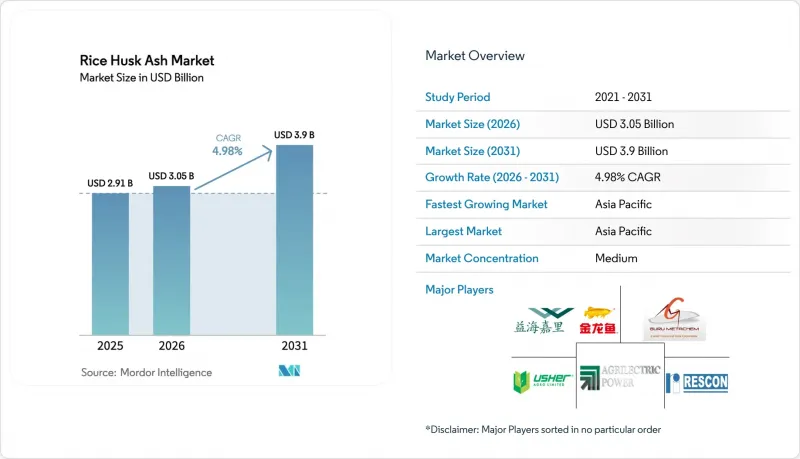

Rice Husk Ash - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Rice Husk Ash Market size is projected to be USD 2.91 billion in 2025, USD 3.05 billion in 2026, and reach USD 3.9 billion by 2031, growing at a CAGR of 4.98% from 2026 to 2031.

Supported by green-building mandates, larger biomass-power pipelines, and expanding demand for ultra-high-purity silica in advanced batteries, the rice husk ash market is shifting from a low-margin waste-management outlet toward premium, specification-driven applications. Cement producers in California, the European Union (EU), and parts of Asia are rushing to secure ASTM C618-compliant pozzolans as coal-fired fly-ash supplies tighten, while tire, refractory, and ceramic manufacturers are paying 20-40% premiums for Greater than or equal to 90% silica grades that slash embodied carbon and improve mechanical performance. Regional rice-mill operators are installing fluidized-bed combustors and baghouse filters to deliver ash with carbon residues below 4%, enabling entry to export markets that insist on third-party quality certification. Parallel developments in magnesiothermic reduction are opening a niche but fast-growing lane for battery-grade RHA feedstock that can be converted into porous silicon delivering 600-2,200 mAh/g in half-cell testing.

Global Rice Husk Ash Market Trends and Insights

Mainstream Green-Building Regulations Mandating SCMs

California's Green Building Code, the American Concrete Institute's new performance-based carbon ceilings, and forthcoming EU Green Deal procurement guidelines are forcing ready-mix suppliers to swap a portion of Portland cement for reactive supplementary cementitious materials. Rice husk ash meets ASTM C618 Class N pozzolan criteria when combusted at 500-700°C; trials show a 6-25% gain in 28-day compressive strength at 10-20% replacement rates while trimming embodied CO2 by up to 230 kg per cubic meter of concrete. LEED (Leadership in Energy and Environmental Design) and BREEAM (Building Research Establishment Environmental Assessment Method) frameworks now award additional credits for bio-based SCMs, reinforcing bankability for RHA-rich mixes on public-sector projects and utility-ratepayer-funded infrastructure. Builders in California, Germany, and Singapore are issuing bid documents that reference RHA outright rather than "natural pozzolan," accelerating standardization. Taken together, these codes and incentives add an estimated 1.2 percentage-point lift to the 2026-2031 CAGR of the Rice Husk Ash market.

Rapid Adoption in Refractory Insulating Mixes

Refractory and steel-insulation applications value RHA's low thermal conductivity of 0.037-0.073 W/m*K and stability above 1,500°C. German producer Refratechnik showed that exothermic riser sleeves with 20% RHA extended solidification time from 273 s to 511 s, cutting casting scrap by 15%. Steelmakers in Japan and South Korea now specify RHA in tundish powders that hold dissolved oxygen within +-5 ppm over 12-hour heats, mitigating reoxidation defects. Ceramic-tile manufacturers in Spain report modulus-of-rupture gains at sintering temperatures below 950°C when substituting quartz with amorphous RHA silica, a shift that saves 8-12% in kiln energy. Margins on refractory-grade ash stand 30-40% above commodity concrete ash, encouraging mills to invest in controlled combustion and post-treatment that elevate silica purity past 90%.

Lack of Globally Harmonized RHA Certification Norms

ASTM C618 mentions natural pozzolans but stops short of codifying rice husk ash, forcing every buyer to run bespoke loss-on-ignition, fineness, and strength-activity tests. Europe's EN 450-1 omits RHA entirely, while India's BIS IS 17225-6 leaves ash quality undefined, creating distrust that raises transaction costs by 10-15% on export deals. The American Concrete Institute's Code 323-24 moves to performance-based carbon caps but provides no RHA-specific acceptance criteria, perpetuating market opacity. As a result, otherwise bankable shipments are stuck in port warehouses awaiting third-party lab results, delaying cash cycles and shaving 0.6 percentage points off expected growth through 2031.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Biomass-Power Co-Generation at Rice Mills

- Government Subsidies for Agro-Waste Valorization

- Competition from Cheaper Fly Ash in Price-Sensitive Regions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

High-purity material (greater than or equal to 90% SiO2) captured 56.67% rice husk ash market share in 2025 and is expanding at a 5.64% CAGR, decisively outpacing lower-grade ash. Producers achieve these purities by burning husk in fluidized-bed kilns at 500-700°C, then applying acid leaching and air classification to strip alkali metals and carbon. At ex-works prices of USD 80-150 per ton, the segment commands a 2 times premium yet experiences minimal demand elasticity because buyers in tires, refractories, and battery anodes view purity as non-negotiable. Continental AG, for instance, cited a 15% lower energy footprint when swapping quartz-derived silica for high-purity RHA silica during its ISCC Plus certified roll-out in 2025.

The less than 90% silica category remains important for regional blended-cement and soil-amendment users that value reactivity and alkalinity over absolute SiO2 content. Delivered costs land at USD 40-70 per ton, underpinned by simple grate furnaces or open-air burning that still meet a minimum 70% combined (SiO2 + Al2O3 + Fe2O3) threshold. Agronomic trials in Bangladesh recorded a jump in grain yield to 5.55 tonnes per hectare with a 1-tonne per hectare application rate, cutting chemical fertilizer demand by 25%.

The Rice Husk Ash Market Report is Segmented by Silica Content (Greater Than or Equal To 90% Silica and Less Than 90% Silica), Application (Cement and Concrete Additive, Silica, Ceramics and Refractories, Steel - Insulating Covers, Rubber and Plastics Filler, and Other Applications), and Geography (Asia-Pacific, North America, Europe, South America, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific dominated the Rice Husk Ash market with 43.37% share in 2025 and is forecast to post a 5.25% CAGR through 2031 as Vietnam, Thailand, India, and Indonesia scale integrated rice-mill-power complexes that monetize electricity, steam, and ash in a single business model. Thailand's Ajinomoto plants alone displace 60 million liters of diesel fuel annually and funnel 15,000 tons of high-grade ash into regional cement kilns, illustrating the synergy between food processing and materials recovery. Vietnam's Hau Giang facility, commissioned in April 2025, serves as a regional blueprint by coupling a 20 MW turbine with ISO-certified ash packaging lines.

North America commands a smaller footing yet showcases strategic moves: Agrilectric Power Partners raised USD 100,000 in early 2025 for research and development aimed at high-reactivity ash, and High Rock Energy Group acquired the 27 MW Wadham Energy plant in November 2025, signaling investor appetite for long-lived, de-risked biomass assets. California's Green Building Code, which now stipulates ASTM-compliant pozzolans in public projects, is turning the Central Valley into a premium supplier corridor for both cement and refractory lines.

Europe's trajectory is intertwined with regulation. The Industrial Emissions Directive forces mills above 1 MW to install baghouses or electrostatic precipitators, a EUR 50,000-200,000 per-MW ticket that smaller, family-owned operations in Italy and Spain struggle to justify. German mills that upgraded in 2025 are now selling ash at an EUR 8-12 premium to cover capex, yet purity levels often exceed Asian benchmarks, giving them a foothold in refractory niches. South America and Africa remain nascent; Brazil's circular-economy statutes and Egypt's co-firing trials could unlock growth once consistent subsidy frameworks are in place, but infrastructure and standards gaps still curtail cross-border flows.

- AC2N THAILAND CO., LTD.

- Agrilectric Power Partners

- Astrra Chemicals

- Enpower Corp.

- Global Recycling

- Guru Metachem Pvt. Ltd.

- JASORIYA RICE MILL

- Ketan Chemicals Corp.

- Rescon

- Rice Husk Ash (Thailand)

- Usher Agro Ltd.

- Yihai Kerry

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Mainstream green-building regulations mandating SCMs

- 4.2.2 Rapid adoption in refractory insulating mixes

- 4.2.3 Expansion of biomass-power co-generation at rice mills

- 4.2.4 Government subsidies for agro-waste valorisation (India, Thailand)

- 4.2.5 Niche demand for ultra-high-purity RHA in Li-ion battery silicon anodes

- 4.3 Market Restraints

- 4.3.1 Lack of globally harmonised RHA certification norms

- 4.3.2 Competition from cheaper fly-ash in price-sensitive regions

- 4.3.3 Tightening particulate-emission limits for biomass boilers (EU IED)

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Silica Content

- 5.1.1 Greater than or equal to 90% Silica

- 5.1.2 Less than 90% Silica

- 5.2 By Application

- 5.2.1 Cement and Concrete Additive

- 5.2.2 Silica

- 5.2.3 Ceramics and Refractories

- 5.2.4 Steel - Insulating Covers

- 5.2.5 Rubber and Plastics Filler

- 5.2.6 Other Applications (Agriculture and Fertilisers, etc.)

- 5.3 By Geography

- 5.3.1 Asia-Pacific

- 5.3.1.1 China

- 5.3.1.2 Japan

- 5.3.1.3 India

- 5.3.1.4 South Korea

- 5.3.1.5 ASEAN Countries

- 5.3.1.6 Rest of Asia-Pacific

- 5.3.2 North America

- 5.3.2.1 United States

- 5.3.2.2 Canada

- 5.3.2.3 Mexico

- 5.3.3 Europe

- 5.3.3.1 Germany

- 5.3.3.2 United Kingdom

- 5.3.3.3 France

- 5.3.3.4 Italy

- 5.3.3.5 Spain

- 5.3.3.6 Russia

- 5.3.3.7 NORDIC Countries

- 5.3.3.8 Rest of Europe

- 5.3.4 South America

- 5.3.4.1 Brazil

- 5.3.4.2 Argentina

- 5.3.4.3 Rest of South America

- 5.3.5 Middle-East and Africa

- 5.3.5.1 Saudi Arabia

- 5.3.5.2 South Africa

- 5.3.5.3 Rest of Middle-East and Africa

- 5.3.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AC2N THAILAND CO., LTD.

- 6.4.2 Agrilectric Power Partners

- 6.4.3 Astrra Chemicals

- 6.4.4 Enpower Corp.

- 6.4.5 Global Recycling

- 6.4.6 Guru Metachem Pvt. Ltd.

- 6.4.7 JASORIYA RICE MILL

- 6.4.8 Ketan Chemicals Corp.

- 6.4.9 Rescon

- 6.4.10 Rice Husk Ash (Thailand)

- 6.4.11 Usher Agro Ltd.

- 6.4.12 Yihai Kerry

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs