PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043962

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043962

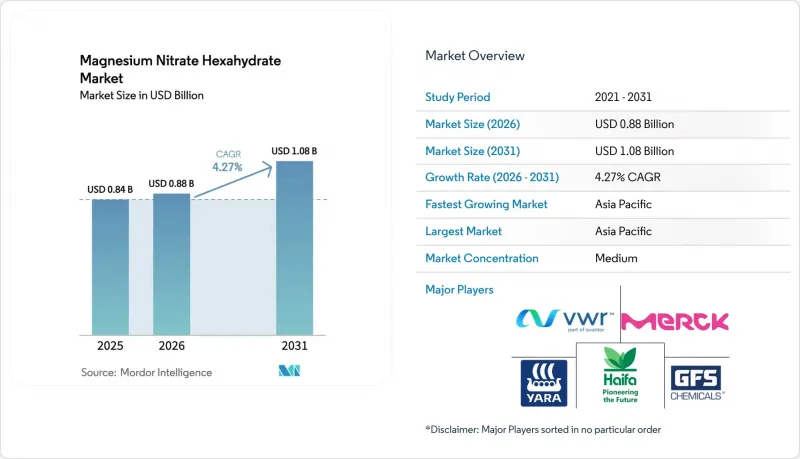

Magnesium Nitrate Hexahydrate - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Magnesium Nitrate Hexahydrate Market size is expected to increase from USD 0.84 billion in 2025 to USD 0.88 billion in 2026 and reach USD 1.08 billion by 2031, growing at a CAGR of 4.27% over 2026-2031.

Demand growth pivots on two reinforcing factors. First, greenhouse and drip-irrigated farms are replacing calcium-ammonium nitrate with water-soluble magnesium nitrate to correct simultaneous nitrogen and magnesium deficiencies without raising soil pH, a shift that directly lifts fertilizer-grade volumes. Second, industrial users value the compound's hygroscopicity in nitric-acid concentration, its oxidizing balance in mining explosives, and its latent-heat profile in phase-change thermal storage, which together create a recurring, diversified pull that moderates cyclical swings in the agriculture cycle. Competitive intensity remains moderate because quality specifications differ sharply between fertilizer, industrial, and reagent grades, creating natural customer lock-in and room for specialty producers to price for purity. Upstream magnesium price volatility injects margin risk, yet the supply chain is slowly regionalizing as projects in Arkansas and Brazil move closer to first metal, a development that should smooth raw-material shocks for downstream formulators by the late forecast period.

Global Magnesium Nitrate Hexahydrate Market Trends and Insights

Rising Demand for Specialty and Water-Soluble Fertilizers

Precision fertigation systems allow growers to meter nutrients in line with evapotranspiration, and magnesium nitrate delivers 16% nitrogen with 9.4% magnesium in a form that stays neutral in solution. Field trials in 2026 found that 0.5% seed priming lifted maize germination by 12% under drought stress, underscoring its resilience benefit. A 6,000-ton plant opened in Brazil in 2025, enabling regional distributors to supply soluble grades with a two-week lead time instead of six, removing a historic logistics hurdle for coffee and citrus growers. Foliar studies in 2025 showed that 2% sprays boosted sweet-corn ear weight by 9% and cut blossom-end rot by 22%, proving the compound's role in protecting marketable yield. Demand lifts in a stepwise fashion as farms install drip systems, meaning the driver's full effect lands over a medium horizon.

Growing Adoption as Catalytic Feedstock in Fine Chemicals

Magnesium nitrate converts to high-surface-area magnesium oxide on calcination, an attribute prized for Lewis-acid catalysis. A 2025 study achieved 94% ketone-to-alcohol conversion at 120°C using oxide derived from the salt, beating palladium on cost per mole converted. Petrochemical licensors specify 2N-5N grades as supports in reforming and cracking catalysts because decomposition releases no sulfur that would poison active metals. Dehydrating qualities make it an alternative to sulfuric acid for pushing nitric acid to 95 wt%, a purity demanded in explosives and certain active pharmaceutical ingredients. Validation cycles in pharmaceuticals run four to six years, placing growth in the long-term bucket.

Health and Environmental Scrutiny of Nitrate Discharge

The United States caps nitrate-nitrogen in drinking water at 10 mg/L, and the European Union limits groundwater nitrate to 50 mg/L, rules that force growers in vulnerable zones to trim soluble nitrate inputs or add cover crops. Municipal plants considering magnesium-nitrate coagulants must show that residual nitrate stays inside discharge permits that now often include dual phosphorus and nitrate ceilings, complicating business cases. An Environmental Protection Agency (EPA) paper in 2024 linked farm runoff to the Gulf of Mexico hypoxic zone, fast-tracking state mandates for controlled-release fertilizers that depress immediate demand. Because regulators already enforce these limits, the restraint bites in the short term.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Use in Mining Explosives and Detonators

- Emerging Use in Thermal-Energy-Storage Phase-Change Materials

- Volatile Magnesium Ore and Brine Supply Pricing

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fertilizer Grade captured 51.28% of the magnesium nitrate hexahydrate market share in 2025 and is projected to expand at a 5.03% CAGR as protected-agriculture acreage grows and soluble blends displace bulk dolomitic lime. Industrial Grade posted slower growth because demand in nitric-acid concentration, detonators, and petrochemical catalysts is mature, yet its multi-year contracts buffer revenue during fertilizer downturns. Reagent Grade, manufactured at 98-99.5% purity, serves analytical laboratories and pharmaceutical synthesis niches where batch traceability commands premiums of 50-80% over commodity grades.

The magnesium nitrate hexahydrate market size for Reagent Grade is forecast to grow substantially as pharmaceutical validation cycles clear and demand for water-quality testing kits expands. Fertilizer Grade pricing remains tethered to global nitrogen benchmarks, but freight savings from the new Brazilian plant could widen delivered-cost spreads by 8-10%, defending margins despite volatile upstream magnesium prices. Suppliers that can swing output between grades stand to arbitrage transient price spikes, yet most facilities are purpose-built, reinforcing moderate market concentration.

Dehydrating-agent use held 35.22% of revenue in 2025 and will grow at 4.78% CAGR because pharmaceutical and explosives producers rely on up-to-95% nitric acid that the salt delivers without sulfate contamination. Oxidizing-agent volumes track mining explosives research programs, many of which sit in advanced pilots, so near-term growth is slower but could inflect if regulatory shifts keep tightening pure ammonium nitrate.

The magnesium nitrate hexahydrate market size for Solubilizing Agent roles in fertigation is set to touch a higher value, mirroring drip-irrigation acreage expansion. Catalytic-promoter demand, though under 10% of volume, is projected to post the highest margin growth as oxide nanoclusters emerge as low-cost supports in transfer-hydrogenation routes for fine chemicals. Function splits underscore a classic dual-engine profile: large agricultural tonnage plus small, high-value chemical niches.

The Magnesium Nitrate Hexahydrate Market Report is Segmented by Grade (Fertilizer Grade, and More), Primary Function (Solubilizing Agent, and More), Application (Fertilizers and Foliar Sprays, Chemical Synthesis and Catalysts, and More), End-User Industry (Agriculture, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific led the magnesium nitrate hexahydrate market in 2025 with 25.12% revenue and is positioned for the fastest 4.96% CAGR through 2031. China's upstream dominance in primary magnesium secures captive feedstock for domestic nitrate producers, keeping ex-works prices 12-18% lower than imports in most months. India's government subsidies for micro-irrigation under the Pradhan Mantri Krishi Sinchayee Yojana are catalyzing fertigation adoption among tomato and capsicum growers, accelerating soluble-grade demand. Japan and South Korea, while small in tonnage, buy high-purity reagent grades, supporting premium unit margins.

North America ranks second in revenue, split between the United States' industrial and laboratory consumption and Mexico's protected-agriculture boom. The December 2025 Defense Production Act award to build a brine-to-metal plant in Arkansas could shave 5-7% off regional nitrate production costs once operational, improving supply resilience against Chinese power curtailments. Canada's role remains niche, focused on explosives predispersions for hard-rock mines and reagent sales to pharmaceutical plants in Ontario and Quebec.

Europe posts moderate tonnage but commands high value because buyers seek reagent and coagulant grades certified to EN and REACH (Registration, Evaluation, Authorisation and Restriction of Chemicals) standards. Stricter nitrate and phosphorus directives are rotating demand from agriculture into municipal water treatment, cushioning revenue even as fertilizer tonnage flattens. South America is the fastest-expanding export destination for Israeli and Norwegian producers, following the Brazilian specialty-fertilizer plant that cut delivery lead times by a month. The Middle East and Africa lag in volume yet show upside in petrochemicals and acid-mine-drainage remediation in South African gold and coal fields.

- American Elements

- Avantor Inc.

- GFS Chemicals Inc.

- Haifa Negev Technologies LTD

- Merck KGaA

- Noah Chemicals

- Sure Chemical Co., Ltd. Shijiazhuang

- Spectrum Chemical

- Thermo Fisher Scientific Inc.

- Valudor Products, LLC

- Yara

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising demand for specialty and water-soluble fertilizers

- 4.2.2 Growing adoption as catalytic feedstock in fine-chemicals

- 4.2.3 Increasing use in mining explosives and detonators

- 4.2.4 Emerging use in thermal-energy-storage phase-change materials

- 4.2.5 Deployment in 3-D-printed concrete admixtures

- 4.3 Market Restraints

- 4.3.1 Health and environmental scrutiny of nitrate discharge

- 4.3.2 Volatile magnesium ore and brine supply chain pricing

- 4.3.3 Substitution by calcium-/ammonium-nitrate blends in fertigation

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Bargaining Power of Suppliers

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Grade

- 5.1.1 Fertilizer Grade

- 5.1.2 Industrial Grade

- 5.1.3 Reagent Grade

- 5.1.4 Other Grades (Pharmaceutical Grade, Electronic/Ultra-high-purity Grade)

- 5.2 By Primary Function

- 5.2.1 Solubilizing Agent

- 5.2.2 Dehydrating Agent

- 5.2.3 Oxidizing Agent

- 5.2.4 Catalyzing/Promoter Agent

- 5.3 By Application

- 5.3.1 Fertilizers and Foliar Sprays

- 5.3.2 Chemical Synthesis and Catalysts

- 5.3.3 Explosives and Propellants

- 5.3.4 Water and Waste-water Treatment

- 5.3.5 Concrete and Construction Additives

- 5.3.6 Other Applications (Thermal Energy Storage (TES), Pharmaceuticals and Nutraceuticals, etc.)

- 5.4 By End-user Industry

- 5.4.1 Agriculture

- 5.4.2 Chemical and Petrochemical

- 5.4.3 Mining and Metallurgy

- 5.4.4 Building and Construction

- 5.4.5 Water and Waste-water Management

- 5.4.6 Other End-user Industries (Healthcare and Life-Sciences, Textile, etc.)

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 ASEAN Countries

- 5.5.1.6 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 NORDIC Countries

- 5.5.3.8 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 South Africa

- 5.5.5.3 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 American Elements

- 6.4.2 Avantor Inc.

- 6.4.3 GFS Chemicals Inc.

- 6.4.4 Haifa Negev Technologies LTD

- 6.4.5 Merck KGaA

- 6.4.6 Noah Chemicals

- 6.4.7 Sure Chemical Co., Ltd. Shijiazhuang

- 6.4.8 Spectrum Chemical

- 6.4.9 Thermo Fisher Scientific Inc.

- 6.4.10 Valudor Products, LLC

- 6.4.11 Yara

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment

8 Key Strategic Questions for CEOs