PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043972

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2043972

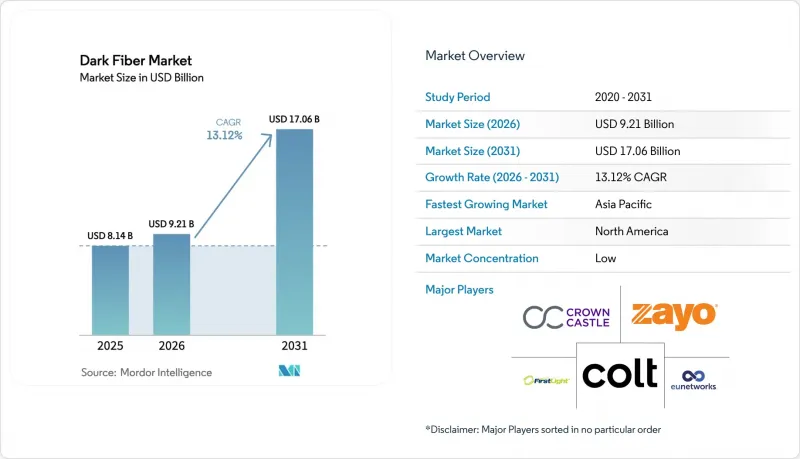

Dark Fiber - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The dark fiber market size in 2026 is estimated at USD 9.21 billion, growing from 2025 value of USD 8.14 billion with 2031 projections showing USD 17.06 billion, growing at 13.12% CAGR over 2026-2031.

Fueled by the exponential bandwidth demands of artificial intelligence workloads, edge computing rollouts, and dense 5G backhaul, the dark fiber market is transitioning from leased lit services to owned infrastructure models. Hyperscale data center operators now favor direct control over fiber routes, pressuring incumbent telecom carriers that historically monetized capacity by the strand. Emerging deployment techniques, such as micro-trenching and aerial placement, help navigate urban right-of-way constraints, even as specialty fiber shortages add complexity. Geographic growth is pivoting toward the Asia-Pacific region, where sovereign cloud mandates and nationwide rural broadband programs are accelerating build-outs. Long-haul expansions remain essential for inter-regional traffic flows, but submarine routes are gaining momentum as content providers scramble for diverse paths across oceans.

Global Dark Fiber Market Trends and Insights

Growing Bandwidth Demand From Cloud And Content Providers

Cloud hyperscalers crossed the utilization threshold where owning strands is cheaper than leasing, prompting multi-country route acquisitions that added 15,000 route-miles to Amazon and USD 2.3 billion in new fiber to Microsoft in 2024. Content delivery networks now require sub-10 millisecond latency in metropolitan areas, leading to dense ring topologies that incumbent carriers struggle to monetize under legacy pricing models. The shift transfers pricing power to neutral infrastructure specialists and enlarges the addressable dark fiber market for wholesale providers.

Rising Adoption Of 5G Networks Requiring Dense Fiber Backhaul

Each 5G cell site demands 10-25 Gbps throughput, a tenfold jump from 4G. Verizon alone added 45,000 new fiber connections during its 2024 Ultra Wideband rollout, investing USD 1.8 billion primarily in dark fiber contracts. The European Union's Gigabit Infrastructure Act accelerates similar builds across member states. Densification outpaces conduit availability, elevating micro-trenching and pole attachments as cost-efficient alternatives and sustaining the near-term demand for dark fiber.

High Initial Capital Expenditure For Fiber Laying

Typical construction now costs USD 15,000-50,000 per route mile, inflated by a 28% rise in equipment and labor costs in 2024. Bond-funded municipal plans stalled, with 40% of projects missing financing milestones and slip dates extending beyond 18 months. Seven-plus-year returns deter new entrants and incite consolidation trends that may temper the addressable base of independent providers in the dark fiber market.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Data Center Interconnect Deployments

- Telecom Operators' Shift From Copper To Fiber Infrastructure

- Complex Right-Of-Way And Permitting Procedures

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-mode fiber captured 71.12% of 2025 revenue and remains the anchor for long-distance builds, thanks to minimal signal loss over multi-kilometer spans, a performance edge that protects the dark fiber market share leadership of this strand type. Terabit-class wavelength division multiplexing keeps single-mode relevant for backbone, metropolitan, and submarine projects where operators need room to scale capacity without undertaking new civil works. The dark fiber market size tied to single-mode strands expands further as enterprises demand carrier-grade resilience on private routes that bypass congested lit networks.

Multimode fiber, although limited to sub-300-meter reaches, is experiencing an acceleration of 13.64% CAGR in data center and factory environments, where wider cores simplify installation and reduce transceiver costs. Composite cables bundling single-mode and multimode cores now dominate campus builds, allowing customers to future-proof against shifting distance and bandwidth needs. Vendors are pushing OM5 multimode enhancements that support short-wave division multiplexing, a step that could stretch use cases beyond server-row connections. The combined approach secures duct utilization efficiency, reinforcing operator preference for higher core counts that preserve upgrade headroom without repeat trenching.

Long-haul infrastructure accounted for 51.76% of 2025 revenue, underscoring its pivotal role in linking hyperscale data centers and national traffic hubs. Lucrative intercity routes command the highest revenue per strand kilometer and protect the segment's dark fiber market share. Metro rings terminate this capacity into enterprise districts, but it is the backbone span that ensures uninterrupted cloud and content delivery across continents.

Submarine systems are projected to post the fastest 13.73% CAGR as global content providers co-fund new cables that diversify geopolitical exposure and reduce latency between hemispheres. Next-generation wet plant designs now ship with 24 to 48 fiber pairs, converting physical routes into dense wholesale inventories that expand the dark fiber market size associated with subsea corridors. Meanwhile, metro operators exploit "dig-once" policies to extend landings inland, stitching together hybrid terrestrial-subsea meshes that raise resiliency benchmarks for OTT and fintech customers.

The Dark Fiber Market Report is Segmented by Fiber Type (Singlemode Fiber, and Multimode Fiber), Network Type (Long-Haul, Metro, and Submarine), End User Industry (Government and Defense, Banking Financial Services and Insurance, Education, Manufacturing, Energy and Utilities, and More), Application (Enterprise Networking, Industrial Automation, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America accounted for 39.21% of 2025 spending, driven by hyperscale data center clusters in Virginia, Ohio, and Texas, as well as a wave of municipal open-access builds. The dark fiber market size in North America is growing steadily as operators exchange legacy copper for fiber to meet regulatory minimums on broadband speeds, while state-level subsidy programs help offset the economic challenges faced by smaller carriers in rural areas. Urban congestion challenges are being mitigated as cities streamline multi-agency permitting into one-touch processes, thereby progressively reducing build timelines.

Europe supports growth through the Gigabit Infrastructure Act, which mandates that buildings be fiber-ready by 2027. Cross-border connectivity stimulates investments in new terrestrial corridors, extending from Frankfurt to Marseille, and submarine entries into Ireland and Portugal. The region's data sovereignty rules are driving demand for intra-EU routing diversity, resulting in a second-tier boom in dark fiber market contracting among data center operators, financial firms, and cloud resellers. Asia-Pacific posts the fastest 13.97% CAGR thanks to China's USD 43 billion rural fiber subsidy and India's USD 8.7 billion modernization program. Southeast Asian nations are pursuing sovereign cloud projects, which involve establishing terrestrial corridors from Singapore through Malaysia into Thailand. Meanwhile, Japan and South Korea are upgrading their aging metro ducts with higher fiber counts to meet the proliferation of edge computing. The Middle East and Africa witness national broadband agendas that prioritize landing points and pan-regional corridors, although project finance can lag behind political ambition. South America is led by Brazil and Argentina in spearheading fiber densification, despite macroeconomic volatility.

- Zayo Group Holdings Inc.

- Crown Castle Fiber LLC

- Colt Technology Services Group Limited

- euNetworks Group Holdings Limited

- FirstLight Fiber Inc.

- GTT Communications Inc.

- Consolidated Communications Holdings Inc.

- Uniti Group Inc.

- FiberLight LLC

- EXA Infrastructure Topco Limited

- Segra Communications LLC

- Neos Networks Limited

- Hudson Fiber Network Inc.

- Arelion AB

- Tampnet AS

- RETN Limited

- Aqua Comms DAC

- Metro Optic Inc.

- Dark Fibre Africa (Pty) Ltd.

- GlobalConnect A/S

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Bandwidth Demand from Cloud and Content Providers

- 4.2.2 Rising Adoption of 5G Networks Requiring Dense Fiber Backhaul

- 4.2.3 Increasing Data Center Interconnect Deployments

- 4.2.4 Telecom Operators' Shift from Copper to Fiber Infrastructure

- 4.2.5 Municipal Open-Access Dark Fiber Initiatives Accelerating Local Builds

- 4.2.6 Surging Subsea Cable Branching Units Enabling Terrestrial Landing Dark Fiber

- 4.3 Market Restraints

- 4.3.1 High Initial Capital Expenditure for Fiber Laying

- 4.3.2 Complex Right-of-Way and Permitting Procedures

- 4.3.3 Fiber Route Saturation in Tier-1 Metro Corridors

- 4.3.4 Supply Chain Disruptions for Specialty Fiber and Duct Materials

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Fiber Type

- 5.1.1 Singlemode Fiber

- 5.1.2 Multimode Fiber

- 5.2 By Network Type

- 5.2.1 Long-Haul

- 5.2.2 Metro

- 5.2.3 Submarine

- 5.3 By End User Industry

- 5.3.1 Telecom and Internet Service Providers

- 5.3.2 Data Centers and Cloud Providers

- 5.3.3 Government and Defense

- 5.3.4 Banking, Financial Services and Insurance

- 5.3.5 Healthcare

- 5.3.6 Education

- 5.3.7 Manufacturing

- 5.3.8 Energy and Utilities

- 5.4 By Application

- 5.4.1 Data Transmission and Telecommunication

- 5.4.2 Enterprise Networking

- 5.4.3 Industrial Automation

- 5.4.4 Military and Defense Communications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Russia

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 India

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 Zayo Group Holdings Inc.

- 6.4.2 Crown Castle Fiber LLC

- 6.4.3 Colt Technology Services Group Limited

- 6.4.4 euNetworks Group Holdings Limited

- 6.4.5 FirstLight Fiber Inc.

- 6.4.6 GTT Communications Inc.

- 6.4.7 Consolidated Communications Holdings Inc.

- 6.4.8 Uniti Group Inc.

- 6.4.9 FiberLight LLC

- 6.4.10 EXA Infrastructure Topco Limited

- 6.4.11 Segra Communications LLC

- 6.4.12 Neos Networks Limited

- 6.4.13 Hudson Fiber Network Inc.

- 6.4.14 Arelion AB

- 6.4.15 Tampnet AS

- 6.4.16 RETN Limited

- 6.4.17 Aqua Comms DAC

- 6.4.18 Metro Optic Inc.

- 6.4.19 Dark Fibre Africa (Pty) Ltd.

- 6.4.20 GlobalConnect A/S

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment