PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044033

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044033

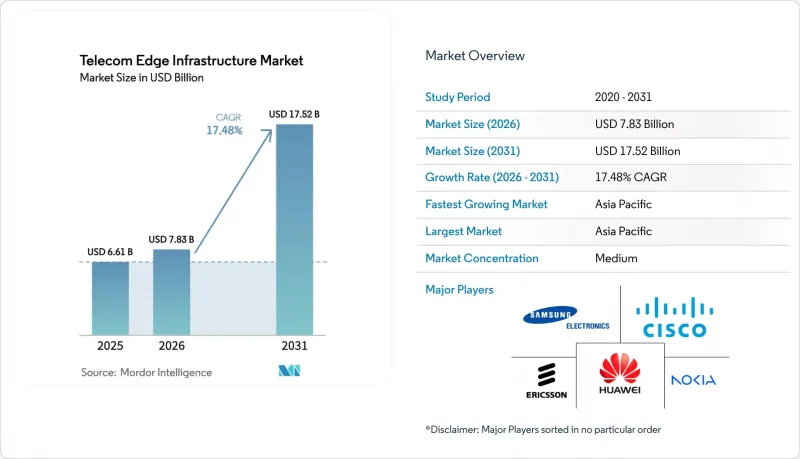

Telecom Edge Infrastructure - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Telecom Edge Infrastructure Market size is expected to grow from USD 6.61 billion in 2025 to USD 7.83 billion in 2026 and is forecast to reach USD 17.52 billion by 2031 at 17.48% CAGR over 2026-2031. Rising traffic from 5G devices, tighter latency targets for factory automation, and tier-1 operator capital re-allocation toward micro-edge nodes underpin this acceleration. Hardware still dominates spending, yet software-defined network functions and orchestration platforms are capturing incremental value as carriers shift from purpose-built appliances to cloud-native workloads. Hyperscale cloud providers are embedding compute at cell-site distances, giving enterprises quick access to sub-10 millisecond round-trip latency and tilting the balance of power away from traditional equipment vendors. Regulatory deadlines for gigabit connectivity and data residency add urgency, while energy-saving RAN controllers improve total cost of ownership and reinforce the business case for distributed deployments.

Global Telecom Edge Infrastructure Market Trends and Insights 5G NR Roll-Out Acceleration

Standalone 5G migration is advancing faster than initial operator forecasts, compressing the schedule for edge node deployment. China recorded 79% standalone penetration by late 2025, while India reached 49.2% and Singapore 37%. The decoupling between marketing claims and core-network upgrades is evident in the 192 operators globally that committed to a standalone architecture, compared with 384 commercial 5G launches. Standalone cores unlock network slicing and URLLC services, sharpening demand for distributed compute. Japan's full-stack virtualized network achieved roughly 20% energy savings after the activation of the RAN Intelligent Controller, illustrating parallel opex benefits. Operators that defer standalone upgrades risk ceding industrial clients to rivals able to guarantee deterministic latency.

Surge in Ultra-Low-Latency Enterprise Use-Cases

Manufacturing, healthcare, and energy firms now require sub-10-millisecond latency for closed-loop control and teleoperation. A 2025 time-sensitive networking trial achieved 122-nanosecond synchronization over 5G, enabling robotic assembly that once relied on industrial Ethernet. Food-processing plants using private 5G with on-prem edge compute issued predictive-maintenance alerts in 6 milliseconds, cutting unplanned downtime. Remote surgery experiments established a 1-5 millisecond latency ceiling for haptic feedback, unachievable from centralized clouds hundreds of kilometers away. Above 90% of enterprises piloting private 5G reported payback within 12 months, driven more by productivity gains than by connectivity cost reductions. The telecom edge infrastructure market is therefore extending beyond early adopters into mainstream operational technology buyers.

Fragmented Standards Across MEC and Open RAN Stacks

Parallel standard bodies publish overlapping specifications that rarely interoperate cleanly. PlugFest testing in 2025 revealed integration failures topping 30% for multi-vendor RAN elements. Operators often maintain separate orchestration planes for each supplier's edge platform, inflating both capital and engineering costs. Vertical integration can reduce risk but raises fears of vendor lock-in. The absence of a unified framework delays broad adoption and cools investment appetite.

Other drivers and restraints analyzed in the detailed report include:

- Private 5G and Campus Networks Adoption

- Telco CAPEX Shift Toward Distributed Cloud Architecture

- High Upfront Site Power and Cooling Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software captured the fastest growth, rising 20.88% through 2031, while hardware retained 53.41% of 2025 revenue. The telecom edge infrastructure market size for software is projected to expand as virtualized user-plane functions and firewalls migrate to Kubernetes containers, freeing operators from proprietary appliances. Universal customer-premises equipment and white-box servers commoditize hardware, lowering margins yet enlarging the pool of suppliers. Orchestration platforms from multiple vendors abstract complexity, cutting service introduction cycles from months to weeks. Integration and managed-service offers remain vital because most carriers lack in-house cloud engineering skills, positioning system integrators to capture a rising share of spending.

A secondary trend sees chip manufacturers bundling accelerator cards with open-source frameworks, simplifying deployment and boosting performance. Hardware vendors respond by shipping ruggedized edge servers built for harsh cell-site environments. The telecom edge infrastructure market continues to balance between cost-optimizing commodity gear and premium, integrated stacks packaged with lifecycle services that de-risk adoption for conservative network operators.

Macro and micro sites still lead deployments, yet on-premises enterprise locations are forecast to grow at 22.02%, reflecting surging interest from factories, hospitals, and ports. The telecom edge infrastructure market share for enterprise sites is set to grow as private networks handle machine control loops on plant floors. Aggregation hubs fill a performance gap for workloads tolerant of sub-20 millisecond latency, while refurbished central offices drive cost-efficient regional coverage.

Private industrial clients prize deterministic performance and data sovereignty, pushing them to self-host compute or contract specialized integrators. Telecom operators counter with managed private 5G to defend relevance, but intense price competition shrinks gross margins. White-box gear and open-source management stacks lower entry barriers, encouraging plant owners to experiment with multi-vendor architectures.

The Telecom Edge Infrastructure Market Report is Segmented by Component (Hardware, Software, and Services), Edge Location (Macro/Micro Cell Sites, Aggregation Hubs, and More), Deployment Model (On-Premise, Telco/Private Cloud, and Hybrid), Application (Enhanced Mobile Broadband (eMBB), and More), End-User Industry (Telecom Operators, Manufacturing, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific leads adoption, accounting for 42.52% of 2025 revenue and a forecast CAGR of 21.61%. Nationwide 5G coverage in China, Japan, and South Korea, underpinned by dense fiber backhaul, supports large-scale edge nodes inside smart-manufacturing clusters. India rolls out standalone 5G across tier-1 and tier-2 cities, though rural fiber scarcity tempers uniform distribution. Southeast Asian smart-city programs in Singapore and Thailand accelerate public-sector edge spending.

North America contributes roughly one-quarter of revenue. U.S. operators deploy thirty-plus metro edge zones to target gaming, computer vision, and retail analytics. Canada builds private networks in automotive and aerospace plants, leveraging government incentives for digital transformation. Operators differentiate through service-level agreements that guarantee sub-20 millisecond latency across hybrid footprints.

Europe records a similar aggregate share, spurred by the Digital Decade requirement for gigabit coverage. Germany, France, and Spain focus on industrial and automotive corridors, while the Nordics exploit abundant renewable energy to offer carbon-neutral edge hosting. Standards fragmentation and spectrum licensing complexities introduce integration delays, yet robust fiber infrastructure smooths long-run scaling.

The Middle East and Africa see uneven progress. Gulf states leverage high disposable income and government diversification agendas to deploy smart-city edge platforms. Sub-Saharan Africa endures fiber gaps, forcing operators to concentrate on macro-site deployments and satellite backhaul for edge outreach. South America gains momentum in Brazil and Argentina, where urban 5G coverage and industrial interest coincide, though regulatory uncertainty around spectrum caps slows multi-country expansion.

List of Companies Covered in this Report:

- Telefonaktiebolaget LM Ericsson

- Nokia Corporation

- Huawei Technologies Co., Ltd.

- Cisco Systems, Inc.

- Samsung Electronics Co., Ltd.

- ZTE Corporation

- NEC Corporation

- Dell Technologies Inc.

- Hewlett Packard Enterprise Company

- Intel Corporation

- Juniper Networks, Inc.

- VMware, Inc. ( Broadcom)

- Red Hat, Inc. (International Business Machines Corporation)

- Amazon Web Services, Inc.

- Microsoft Corporation

- Google LLC

- Mavenir Systems, Inc.

- Parallel Wireless, Inc.

- Rakuten Symphony, Inc. (Rakuten Group, Inc.)

- Affirmed Networks, Inc. (Microsoft Corporation)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 5G NR Roll-Out Acceleration

- 4.2.2 Surge in Ultra-Low-Latency Enterprise Use-Cases

- 4.2.3 Private 5G and Campus Networks Adoption

- 4.2.4 Telco CAPEX Shift Toward Distributed Cloud Architecture

- 4.2.5 RAN Intelligent Controller (RIC) Enabling Agile Edge Apps

- 4.2.6 Micro-Edge Sustainability Incentives (Renewable Power)

- 4.3 Market Restraints

- 4.3.1 Fragmented Standards Across MEC and Open RAN Stacks

- 4.3.2 High Upfront Site Power and Cooling Costs

- 4.3.3 Limited Edge-To-Core Orchestration Skill-Set Among CSPs

- 4.3.4 Fiber Backhaul Bottlenecks in Emerging Economies

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.1.1 Edge Servers

- 5.1.1.2 uCPE / White-box

- 5.1.1.3 RAN Distributed Units (DU)

- 5.1.2 Software

- 5.1.2.1 Virtualized Network Functions

- 5.1.2.2 Edge Orchestration Platforms

- 5.1.3 Services

- 5.1.1 Hardware

- 5.2 By Edge Location

- 5.2.1 Macro / Micro Cell Sites

- 5.2.2 Aggregation Hubs

- 5.2.3 Central Offices

- 5.2.4 Regional Data Centers

- 5.2.5 Enterprise On-prem Edge

- 5.3 By Deployment Model

- 5.3.1 On-premises

- 5.3.2 Telco / Private Cloud

- 5.3.3 Hybrid

- 5.4 By Application

- 5.4.1 Enhanced Mobile Broadband (eMBB)

- 5.4.2 Massive IoT (mMTC)

- 5.4.3 Mission-critical / URLLC

- 5.5 By End-user Industry

- 5.5.1 Telecom Operators

- 5.5.2 Manufacturing

- 5.5.3 Healthcare

- 5.5.4 Media and Entertainment

- 5.5.5 Transportation and Logistics

- 5.5.6 Other end-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Russia

- 5.6.3.5 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 Saudi Arabia

- 5.6.5.1.2 United Arab Emirates

- 5.6.5.1.3 Rest of the Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Telefonaktiebolaget LM Ericsson

- 6.4.2 Nokia Corporation

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Cisco Systems, Inc.

- 6.4.5 Samsung Electronics Co., Ltd.

- 6.4.6 ZTE Corporation

- 6.4.7 NEC Corporation

- 6.4.8 Dell Technologies Inc.

- 6.4.9 Hewlett Packard Enterprise Company

- 6.4.10 Intel Corporation

- 6.4.11 Juniper Networks, Inc.

- 6.4.12 VMware, Inc. ( Broadcom)

- 6.4.13 Red Hat, Inc. (International Business Machines Corporation)

- 6.4.14 Amazon Web Services, Inc.

- 6.4.15 Microsoft Corporation

- 6.4.16 Google LLC

- 6.4.17 Mavenir Systems, Inc.

- 6.4.18 Parallel Wireless, Inc.

- 6.4.19 Rakuten Symphony, Inc. (Rakuten Group, Inc.)

- 6.4.20 Affirmed Networks, Inc. (Microsoft Corporation)

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment