PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044039

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044039

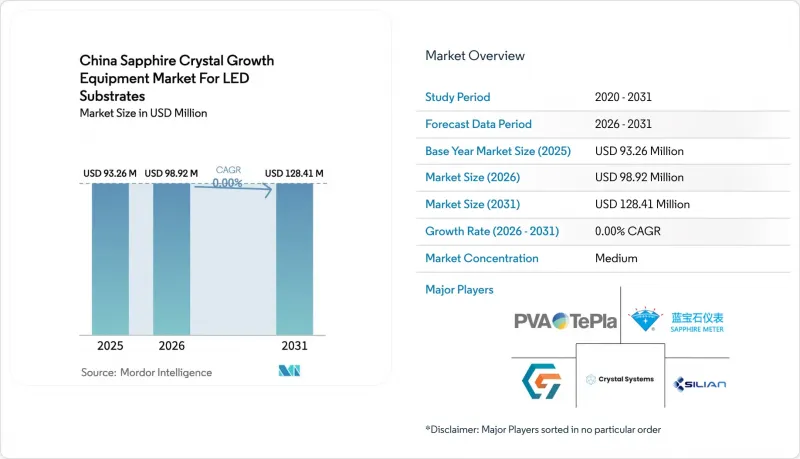

China Sapphire Crystal Growth Equipment For LED Substrates - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The China sapphire crystal growth equipment market for LED substrates industry size was valued at USD 93.26 million in 2025 and is estimated to grow from USD 98.92 million in 2026 to reach USD 128.41 million by 2031, at a CAGR of 0% during the forecast period (2026-2031).

Government directives that require at least 50% domestic content in new semiconductor fabs, together with the RMB 344 billion (USD 49.8 billion) Big Fund Phase 3 allocation, are redirecting procurement toward Chinese suppliers of Kyropoulos, Czochralski and edge-defined film-fed-growth (EFG) furnaces. Demand is further underpinned by Mini-LED backlighting investments for televisions and automotive displays, by provincial 14th Five-Year Plans that list sapphire substrates as strategic materials, and by the integration of artificial-intelligence process control that trims cycle time and improves yield. Environmental audits on high-temperature furnaces and volatility in high-purity alumina feedstock prices, however, temper near-term expansion and incentivize upgrades that cut emissions and material waste.

Insights and Trends of China Sapphire Crystal Growth Equipment Market For LED Substrates

Accelerating Mini-LED Backlighting Investments

Television and automotive display makers are shifting from edge-lit to direct-lit Mini-LED architectures that require many more chips per panel, driving a matching surge in sapphire substrate demand. Leading LED manufacturers validated 6-inch and 8-inch wafers during 2025 pilot runs, which pushed equipment tenders for Kyropoulos and Czochralski furnaces capable of lower dislocation densities. Patterned sapphire substrates that boost light-extraction efficiency by nearly one-third further raise equipment requirements because they add laser patterning and plasma etch steps to the production line. Vendors able to bundle crystal growth, patterning and polishing solutions capture larger wallet share as vertically integrated LED makers prefer one-stop procurement. Consequently, Mini-LED investment pipelines continue to anchor near-term tool orders across coastal manufacturing clusters.

Export-Oriented Capacity Expansion by Chinese LED Makers

Beijing's December 2025 rule that at least half of semiconductor tools in approved projects must be sourced domestically drives a structural shift in bidding criteria. Crystal growth equipment makers that pass technology certification gain immediate access to centrally funded orders, while imported systems without local value-add lose price competitiveness after tariff equivalencies and extended delivery lead times. The Big Fund's earmark for compound semiconductor materials further cushions working-capital needs, enabling smaller substrate producers to swap 4-inch lines for 6-inch platforms without prohibitive upfront cash outlay. Parallel provincial grants and tax credits accelerate retrofit timetables, locking in a near-term demand bulge for China-made furnaces, control software and consumable-grade crucibles.

Volatility in High-Purity Alumina Prices

High-purity alumina accounts for a sizable share of sapphire boule cost, so sudden price spikes quickly erode wafer-house margins. Bauxite supply disruptions in 2025 exposed the fragility of the refining chain, lifting spot quotes and forcing several substrate makers to delay furnace purchases. Larger producers cushioned the shock with long-term offtake contracts and in-house refining pilots, yet smaller firms lacked that hedge and trimmed operating rates. Equipment vendors felt the knock-on effects of order lumpiness and extended payment terms, which complicated factory scheduling. Sustained feedstock volatility, therefore, weighs on near-term demand and encourages vertical integration that diverts capital away from new crystal growth tools.

Other drivers and restraints analyzed in the detailed report include:

- Rising Adoption of Large-Diameter (Above 300 mm) Sapphire Ingots

- Export-Oriented Capacity Expansion by Chinese LED Makers

- Technical Barriers in Scaling Kyropoulos Furnaces Beyond 12 Inch

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Sales of crystal growth furnaces represented 70.13% of the China sapphire crystal growth equipment market for LED substrates industry in 2025. Retrofit demand centers on heater redesigns and crucible upgrades that enhance throughput without full chassis replacement, preserving the installed base. Growth-automation and process-control systems are projected to rise at a 6.21% CAGR, a faster clip than the overall market, as wafer houses deploy AI modules that shorten seeding cycles and standardize operator skill variability. Pollution-control and electrified heating retrofits also gain traction as emis-sion rules tighten, opening another revenue stream within the thermal-field subsystem niche.

Growth-automation and process-control modules are on track to lift their contribution to the sapphire crystal growth equipment market size as wafer houses retrofit legacy furnaces instead of buying new frames. Tool makers package closed-loop thermal management, in-situ defect imaging and predictive maintenance software as bolt-on kits that install during scheduled shutdowns, preserving production continuity. Longer-life crucibles and low-NOx heater assemblies are bundled into these upgrades, giving customers a single contact for both hardware and software. This integrated offer compresses payback to less than two years for most mid-volume fabs, a period that aligns with provincial subsidy windows and supports recurring revenue for vendors through software licenses and consumable replenishment.

The China Sapphire Crystal Growth Equipment Market for LED Substrates Industry Report is Segmented by Equipment Type (Crystal Growth Furnaces, Thermal Field and Crucible Systems, and More), Growth Technology (Kyropoulos Method, Edge-Defined Film-Fed Growth, Heat Exchanger Method, and More), and Sapphire Diameter Capability (Up To 150 Mm, 150-300 Mm, and Above 300 Mm). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Zhejiang Jingsheng Mechanical & Electrical Co., Ltd.

- Chongqing Silian Optoelectronics Science & Technology Co., Ltd.

- GT Advanced Technologies Inc.

- PVA TePla AG

- Crystal Systems Corporation

- Advanced Technology & Materials Co., Ltd.

- Xi'an Chaowei Sapphire Technology Co., Ltd.

- Suzhou Crystal Power Co., Ltd.

- Beijing Naura Microelectronics Equipment Co., Ltd.

- Kunshan Grace Crystal Equipment Co., Ltd.

- Hangzhou Jingpu Electronic Equipment Co., Ltd.

- Hebei Synlight Crystal Equipment Co., Ltd.

- Shenyang Crystec Equipment Co., Ltd.

- Nantong Tianren Sapphire Machinery Co., Ltd.

- Zhejiang Crystal-Optech Co., Ltd.

- Ningbo Aurora Crystal Technology Co., Ltd.

- Wuxi Haoyuan Crystal Technology Co., Ltd.

- Yunnan Crystaland New Material Co., Ltd.

- Sichuan Jinmei Machinery Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Mini-LED Back-lighting Investments

- 4.2.2 Subsidies for Domestic Equipment Localization

- 4.2.3 Rising Adoption of Large-Diameter (Above 300 mm) Sapphire Ingots

- 4.2.4 Surge in Smart-Lighting Urban Projects

- 4.2.5 Export?Oriented Capacity Expansion by Chinese LED Makers

- 4.2.6 Integration of AI-Based Process Control in Growth Furnaces

- 4.3 Market Restraints

- 4.3.1 Volatility in High-Purity Alumina Prices

- 4.3.2 Technical Barriers in Scaling Kyropoulos Furnaces Beyond 12-inch

- 4.3.3 Stringent Environmental Audits on High-Temperature Furnaces

- 4.3.4 Slow Retrofit Cycles Among Tier-2 LED Wafer Houses

- 4.4 Industry Ecosystem Analysis

- 4.5 Porter's Five Forces Analysis

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Equipment Type

- 5.1.1 Crystal Growth Furnaces

- 5.1.2 Thermal Field and Crucible Systems

- 5.1.3 Growth Automation and Process Control Systems

- 5.2 By Growth Technology

- 5.2.1 Kyropoulos Method

- 5.2.2 Edge-Defined Film-Fed Growth (EFG)

- 5.2.3 Heat Exchanger Method

- 5.2.4 Czochralski Method

- 5.3 By Sapphire Diameter Capability

- 5.3.1 Upto 150 mm

- 5.3.2 150-300 mm

- 5.3.3 Above 300 mm

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Zhejiang Jingsheng Mechanical & Electrical Co., Ltd.

- 6.4.2 Chongqing Silian Optoelectronics Science & Technology Co., Ltd.

- 6.4.3 GT Advanced Technologies Inc.

- 6.4.4 PVA TePla AG

- 6.4.5 Crystal Systems Corporation

- 6.4.6 Advanced Technology & Materials Co., Ltd.

- 6.4.7 Xi'an Chaowei Sapphire Technology Co., Ltd.

- 6.4.8 Suzhou Crystal Power Co., Ltd.

- 6.4.9 Beijing Naura Microelectronics Equipment Co., Ltd.

- 6.4.10 Kunshan Grace Crystal Equipment Co., Ltd.

- 6.4.11 Hangzhou Jingpu Electronic Equipment Co., Ltd.

- 6.4.12 Hebei Synlight Crystal Equipment Co., Ltd.

- 6.4.13 Shenyang Crystec Equipment Co., Ltd.

- 6.4.14 Nantong Tianren Sapphire Machinery Co., Ltd.

- 6.4.15 Zhejiang Crystal-Optech Co., Ltd.

- 6.4.16 Ningbo Aurora Crystal Technology Co., Ltd.

- 6.4.17 Wuxi Haoyuan Crystal Technology Co., Ltd.

- 6.4.18 Yunnan Crystaland New Material Co., Ltd.

- 6.4.19 Sichuan Jinmei Machinery Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment