PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044049

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044049

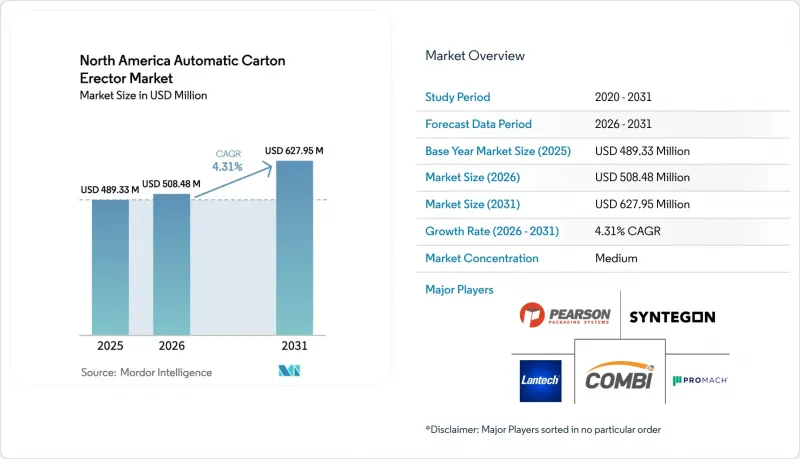

North America Automatic Carton Erector - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The North America automatic carton erector market size is expected to increase from USD 489.33 million in 2025 to USD 508.48 million in 2026 and reach USD 627.95 million by 2031, growing at a CAGR of 4.31% over 2026-2031.

Expanding e-commerce footprints, double-digit rises in warehouse wages, and stricter food-safety mandates collectively steer procurement budgets toward automated case forming. Finance teams now calculate 18- to 24-month payback horizons as labor represents nearly one-third of end-of-line packaging cost, while 40%-50% wage inflation since 2019 accelerates automation justification. Vendors face fewer technology barriers because vision-guided robotics, servo motion, and modular frames have become standard offerings, so competitive advantage shifts to pre-wired, quick-install packages that minimize engineering lead time. Deeper capital scrutiny inside legacy food plants tempers the overall growth pace because electrical upgrades, floor-leveling, and fire-code retrofits can double installed cost when retrofitting 30-year-old buildings. Key adoption differentials surface across segments. Regular slotted case (RSC) formats still dominate because they handle 70%-80% of corrugated shipping volume, yet retailers' dimensional-weight surcharges spur faster uptake of tray formers and wraparound styles. Mid-tier 20-40 carton-per-minute (CPM) machines account for two-fifths of 2025 revenue because they match throughput on most frozen food, pharma, and contract-packaging lines; however, >40 CPM systems are gaining share in beverage and snack operations that now run three shifts during seasonal peaks. Fully automatic platforms comprise almost two-thirds of 2025 installations, but their growth is gated by the scarcity of technicians who can maintain servo drives, vision cameras, and PLC code. Geography again shapes ROI; the United States controls more than four-fifths of 2025 sales, Canada emerges as the fastest grower through 2031 on the back of greenfield fulfillment hubs, and Mexico is a nearshoring wild card whose upside depends on service-network reach and wage-cost trajectories.

North America Automatic Carton Erector Market Trends and Insights

Boom in E-Commerce Fulfillment Centers

Online retailers embed automatic erectors inside greenfield distribution hubs to eliminate 8- to 12-second manual case assembly steps, sustaining throughput targets above 1,000 units per hour. Walmart Canada's USD 6.5 billion Vaughan and Calgary nodes integrate carton forming with high-density storage, while Amazon's 2.8 million square-foot YYC4 site runs robotic picking that depends on pre-erected cartons. Micro-fulfillment specialists such as Metro Supply Chain pair AutoStore cubes with compact erectors, pushing order-to-ship cycles under 30 minutes. Distributed networks multiply the number of required machines even when single-site volumes drop, favoring modular, plug-and-play formats that forklift into position and wire up in hours rather than days.

Rising Labor Costs Prompting Automation Adoption

Average warehouse wages reached USD 18.99 per hour in Q2 2024, a 40%-50% jump since 2019, compressing carton-erector payback periods to 18-24 months. High turnover magnifies savings; each replacement costs firms USD 3,500 in recruiting and onboarding, repeating every 8-12 months in many distribution centers. Contract logistics providers reshoring operations from Asia enter labor-scarce markets where unemployment hovers near record lows, leaving automation as the only scalable path. Nonetheless, only 13% of surveyed warehouses report full packaging automation because upstream palletizing and downstream labeling must be modernized in parallel.

High Upfront Capital Expenditure

Entry-level semi-automatic units start near USD 15,000, while fully automatic, vision-equipped platforms exceed USD 100,000, a hurdle for food processors operating on single-digit margins. Total installed cost doubles after accounting for blank feeders, downstream sealers, and system integration, stretching ROI beyond 36 months when plants run only one shift. Leasing models remain nascent in packaging machinery, forcing firms to draw on working-capital lines priced above 7% interest in 2024. Contract manufacturers with variable volume commitments hesitate to lock in fixed costs, and many postpone automation until private-equity consolidators roll up multiple sites to achieve scale.

Other drivers and restraints analyzed in the detailed report include:

- Stricter Food Safety Packaging Regulations

- Integration of Vision-Guided Robotics

- Skilled Technician Shortage for Maintenance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Regular slotted case erectors accounted for 45.32% of the market share in 2025, underscoring their entrenched role in pallet-optimized shipping lanes, yet their growth aligns with the overall North America automatic carton erector market. Specialty case erectors is projected to outpace the baseline at 5.34% because right-sized packaging trims dimensional-weight fees that erode digital-retail margins. Tray formers serve fresh produce and ready-meal sectors that need airflow and shelf visibility, while tablock designs remove adhesive, lowering consumables budgets and improving curbside recyclability. Wraparound styles offer billboard-quality graphics for warehouse-club aisles, but they require precision product loading and intolerance for SKU variances, increasing the importance of integrated robotics.

Vision-guided systems now enable sub-10-minute tool-free changeovers, making mixed-format production economical at batch sizes below 500. Combi's Ergopack 2.0, capable of switching between RSC and tray within minutes, answers multi-SKU demands in grocery e-commerce fulfillment. Pharmaceutical and nutraceutical contract packers add tamper-evident inserts during erection, leveraging specialty formats for compliance as well as marketing. The shift toward sustainability reinforces the trend, since wraparounds and trays often reduce corrugated usage by 10%-15%, supporting corporate ESG scorecards.

Systems rated 20-40 CPM captured 40.21% of the market share in 2025, aligning with the North America automatic carton erector market size requirements of frozen food, OTC pharma, and contract-packaging lines that balance volume with frequent changeovers. Sub-20 CPM machines persist in artisan and clinical-trial environments where manual assembly still pencils out. Equipment above 40 CPM is forecast to grow 5.53%, driven by beverage, snack, and same-day-delivery fulfillment centers whose uptime economics demand automated forming.

Schneider's servo-driven platform hits 60 CPM while still fitting a 12-foot footprint, enabling Labor Day beverage promotions without adding temporary workers. The ROI accelerates in continuous 2- or 3-shift plants; a 60 CPM erector running 20 hours daily erects 72,000 cases, eliminating four to five operators and recouping capital in 12-15 months. The constraint lies upstream, and downstream case sealers, packers, and palletizers must match speed, often bumping system budgets toward USD 0.5-0.75 million.

The North America Automatic Carton Erector Market Report is Segmented by Product Type (Regular Slotted Case Erectors, Tablock Case Erectors, Tray Forming Erectors, and Specialty Case Erectors), Speed Band (Up To 20 CPM, 20-40 CPM, and Above 40 CPM), End-Use Industry (Food and Beverage, and More), Automation Level (Semi-Automatic, and Fully Automatic), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- ProMach Inc.

- Syntegon Technology GmbH

- Combi Packaging Systems LLC

- Pearson Packaging Systems LLC

- Lantech LLC

- Massman Automation Designs LLC

- Schneider Packaging Equipment Company Inc.

- EndFlex LLC

- Douglas Machine Inc.

- Delkor Systems Inc.

- ADCO Manufacturing

- Somic Packaging Inc.

- Econocorp Inc.

- BluePrint Automation B.V.

- JLS Automation

- Hamrick Manufacturing and Service Inc.

- Texwrap Packaging Systems LLC

- Kliklok-Woodman LLC

- PMI KYOTO Packaging Systems Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Labor Costs Prompting Automation Adoption

- 4.2.2 Boom in E-Commerce Fulfillment Centers

- 4.2.3 Stricter Food Safety Packaging Regulations

- 4.2.4 Integration of Vision-Guided Robotics

- 4.2.5 Adoption of Plug-and-Play Modular Machines

- 4.2.6 Shift Toward Recyclable Corrugated Materials

- 4.3 Market Restraints

- 4.3.1 High Upfront Capital Expenditure

- 4.3.2 Limited Floor Space in Legacy Facilities

- 4.3.3 Skilled Technician Shortage for Maintenance

- 4.3.4 Supply Chain Volatility of Corrugated Board

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Regular Slotted Case Erectors

- 5.1.2 Tablock Case Erectors

- 5.1.3 Tray Forming Erectors

- 5.1.4 Specialty Case Erectors

- 5.2 By Speed Band (Cartons per Minute)

- 5.2.1 Up to 20 CPM

- 5.2.2 20-40 CPM

- 5.2.3 Above 40 CPM

- 5.3 By End-Use Industry

- 5.3.1 Food and Beverage

- 5.3.2 E-Commerce and Retail

- 5.3.3 Pharmaceuticals

- 5.3.4 Industrial Goods

- 5.3.5 Other End-Use Industries

- 5.4 By Automation Level

- 5.4.1 Semi-Automatic

- 5.4.2 Fully Automatic

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 ProMach Inc.

- 6.4.2 Syntegon Technology GmbH

- 6.4.3 Combi Packaging Systems LLC

- 6.4.4 Pearson Packaging Systems LLC

- 6.4.5 Lantech LLC

- 6.4.6 Massman Automation Designs LLC

- 6.4.7 Schneider Packaging Equipment Company Inc.

- 6.4.8 EndFlex LLC

- 6.4.9 Douglas Machine Inc.

- 6.4.10 Delkor Systems Inc.

- 6.4.11 ADCO Manufacturing

- 6.4.12 Somic Packaging Inc.

- 6.4.13 Econocorp Inc.

- 6.4.14 BluePrint Automation B.V.

- 6.4.15 JLS Automation

- 6.4.16 Hamrick Manufacturing and Service Inc.

- 6.4.17 Texwrap Packaging Systems LLC

- 6.4.18 Kliklok-Woodman LLC

- 6.4.19 PMI KYOTO Packaging Systems Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment