PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044050

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044050

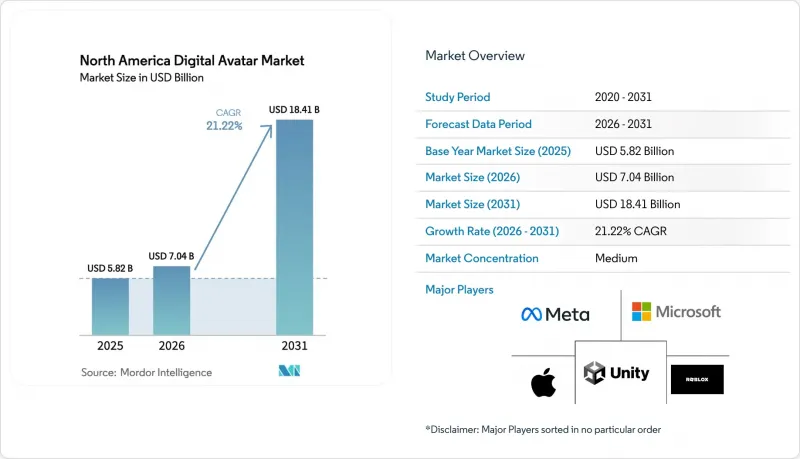

North America Digital Avatar - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The North America digital avatar market size is expected to increase from USD 5.82 billion in 2025 to USD 7.04 billion in 2026 and reach USD 18.41 billion by 2031, growing at a CAGR of 21.22% over 2026-2031.

Persistent hardware progress, emotion-AI breakthroughs, and clear disclosure rules are accelerating enterprise adoption across customer care, telehealth, and immersive commerce. Heavy investment by hyperscalers such as Meta Platforms and Microsoft, which together earmark well above USD 10 billion per year for metaverse tooling, keeps compute and software capabilities on an aggressive improvement curve. At the same time, rising labor shortages in health systems and retail contact centers are prompting budget reallocation from headcount to avatar-enabled automation, while legal certainty around COPPA 2.0 and state biometric statutes is reducing procurement friction. These converging forces position the North America digital avatar market to outgrow most adjacent conversational-AI segments over the next five years.

North America Digital Avatar Market Trends and Insights

Proliferation of Virtual Reality and Augmented Reality Hardware

Rapid uptake of affordable head-mounted displays is lifting baseline demand for immersive identity layers. Meta's USD 299 Quest 3S, released in late 2024, and Apple's Vision Pro, which entered commercial circulation in early 2025, collectively pushed the North American installed base of XR headsets past 15 million devices. Both headsets ship with built-in codec-avatar pipelines that map facial muscle movement and hand gestures, enabling lifelike embodiment during remote collaboration, virtual showrooms, and surgical simulations. Middleware vendors such as Unity have responded with on-device inference engines that shave server round-trips, lowering latency beneath the 100 millisecond threshold viewed by cognitive researchers as critical for natural social presence. As edge rendering capacity increases, enterprises no longer face a trade-off between photorealism and responsiveness, removing a historical adoption ceiling for the North America digital avatar market.

Growing Adoption of Digital Avatars in Customer Service Chatbots

Contact-center cost inflation and consumer demand for 24/7 assistance have produced a surge in avatar-equipped virtual agents. More than 8,000 such agents went live across financial and retail networks in 2025, up 140% year over year. BNY Mellon alone activated 20,000 photorealistic assistants that now resolve two-thirds of tier-1 wealth-management inquiries, trimming annual operating spend by USD 42 million. Disclosure mandates from the Federal Trade Commission require clear identification of synthetic staff, and this legal clarity has paradoxically accelerated procurement as chief risk officers now have definitive compliance frameworks. The measurable lift in customer-satisfaction scores is persuading additional banks and retailers to pilot conversational avatars in 2026, cementing the channel as an early-cycle revenue driver for the North America digital avatar market.

High Computational Costs for Real-Time Rendering

Despite progress in edge inference, photorealistic avatars still require premium GPUs or substantial cloud budgets. A single RTX 6000 Ada card retails at roughly USD 6,800, and enterprise-grade servers often need multiple units to sustain 4K, 60 fps sessions. On-demand cloud rendering, priced near USD 0.45 per GPU-hour, converts into monthly bills that many small businesses cannot absorb. Optimization tools such as Unity's Ziva have shaved polygon counts by 40%, yet the residual cost still restrains broad deployments in education and mid-tier healthcare systems. Unless Moore's-law-like efficiency gains reach rendering stacks, this expense will continue to drag on the North America digital avatar market growth.

Other drivers and restraints analyzed in the detailed report include:

- Increasing Popularity of Virtual Influencers for Brand Marketing

- Rise of Metaverse Platforms Led by Gaming and Social Media

- Data Privacy and Security Concerns Around Biometric Likeness

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The interactive avatars is scaling quickly, advancing at a 22.53% CAGR as organizations migrate from one-way mascots to conversational agents that deliver measurable business outcomes. Hospitals within the Ardent network shortened average emergency-department wait times by 22 minutes after installing triage avatars, a performance proof point that encourages further health-system rollouts. Interactive designs incorporate automatic speech recognition, large-language reasoning, and emotion-AI, allowing them to deflect repetitive inquiries and escalate only complex cases, thereby preserving staff bandwidth. In gaming, Microsoft Teams' Mesh avatars now host internal project reviews and client demos for more than 1.8 million corporate users, reducing reported meeting fatigue by double digits.

Non-interactive avatars remain central to branding missions, especially in entertainment franchises determined to maintain color-graded stylistic consistency. Their 57.89% share in 2025 reflects wide deployment across social channels, festivals, and merchandise campaigns. However, as language models improve contextual guardrails, interactive agents are expected to absorb much of the marketing storytelling workload. Ongoing advances in low-latency rendering are helping diminish user frustration over lag, making the North America digital avatar market progressively skew toward two-way formats.

3D avatars held a 52.32% share in 2025, but AI-generated humans is expected to grow at a CAGR of 22.67% during the forecast period. It is closing the gap by promising cinematic quality without weeks of manual rigging. Epic Games' MetaHuman Creator compresses asset build time from nearly a month to under 2 hours, a shift that brought 420 studios into the workflow last year. Neural rendering add-ons such as NVIDIA Audio2Face hit 98% lip-sync accuracy across 14 languages, a vital feature for localized content in multicultural North America. Enterprises favor these toolchains because they permit rapid A/B experimentation of persona tone, attire, and voice without reshoots.

3D avatars are not vanishing; their lower compute requirements make them attractive for browser-based or mobile contexts with bandwidth ceilings. Snap's Bitmoji, which retains a stylized 2D-plus aesthetic, serves hundreds of millions of messages daily and continues to anchor brand partnership packs. Over the forecast horizon, hybrid toolkits that merge procedural meshes with neural texturing will dominate, cushioning the transition for art teams steeped in legacy workflows while satisfying executive mandates for higher realism in customer-facing deployments. Such convergence sustains multi-stack demand, broadening the addressable base for the North America digital avatar market.

The North America Digital Avatar Market Report is Segmented by Product Type (Interactive Digital Avatars, and Non-Interactive Digital Avatars), Technology (2D Avatar, 3D Avatars, and AI-Generated Realistic Human Avatars), Application (Customer Service and Virtual Agents, and More), End User Industry (Media and Entertainment, Retail and Ecommerce, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Meta Platforms Inc.

- Microsoft Corporation

- Apple Inc.

- Roblox Corporation

- Unity Software Inc.

- NVIDIA Corporation

- Epic Games Inc.

- Amazon.com Inc.

- Alphabet Inc.

- Snap Inc.

- Inworld AI Inc.

- Wolf3D OU (Ready Player Me)

- Genies Inc.

- Soul Machines Ltd.

- Reallusion Inc.

- Pinscreen Inc.

- Loom.ai Inc.

- Adobe Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Virtual Reality and Augmented Reality Hardware

- 4.2.2 Growing Adoption of Digital Avatars in Customer Service Chatbots

- 4.2.3 Increasing Popularity of Virtual Influencers for Brand Marketing

- 4.2.4 Rise of Metaverse Platforms Led by Gaming and Social Media

- 4.2.5 Integration of Emotion-AI for Hyper-Realistic Avatar Expressions

- 4.2.6 Expansion of Telepresence Robots Powered by Photorealistic Avatars

- 4.3 Market Restraints

- 4.3.1 High Computational Costs for Real-Time Rendering

- 4.3.2 Data Privacy and Security Concerns Around Biometric Likeness

- 4.3.3 Limited Interoperability Standards Across Avatar Ecosystems

- 4.3.4 Ethical Backlash Against Deepfake-based Avatar Generation

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Type

- 5.1.1 Interactive Digital Avatars

- 5.1.2 Non-Interactive Digital Avatars

- 5.2 By Technology

- 5.2.1 2D Avatar

- 5.2.2 3D Avatars

- 5.2.3 AI-Generated Realistic Human Avatars

- 5.3 By Application

- 5.3.1 Customer Service and Virtual Agents

- 5.3.2 Marketing and Advertising

- 5.3.3 Gaming and Entertainment

- 5.3.4 E-Learning and Training

- 5.3.5 Healthcare and Telehealth

- 5.3.6 Social Media and Content Creation

- 5.4 By End User Industry

- 5.4.1 Media and Entertainment

- 5.4.2 Retail and Ecommerce

- 5.4.3 Healthcare Providers

- 5.4.4 Education Institutions

- 5.4.5 Banking and Financial Services (BFSI)

- 5.4.6 Government and Public Services

- 5.4.7 Other End User Industries

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Meta Platforms Inc.

- 6.4.2 Microsoft Corporation

- 6.4.3 Apple Inc.

- 6.4.4 Roblox Corporation

- 6.4.5 Unity Software Inc.

- 6.4.6 NVIDIA Corporation

- 6.4.7 Epic Games Inc.

- 6.4.8 Amazon.com Inc.

- 6.4.9 Alphabet Inc.

- 6.4.10 Snap Inc.

- 6.4.11 Inworld AI Inc.

- 6.4.12 Wolf3D OU (Ready Player Me)

- 6.4.13 Genies Inc.

- 6.4.14 Soul Machines Ltd.

- 6.4.15 Reallusion Inc.

- 6.4.16 Pinscreen Inc.

- 6.4.17 Loom.ai Inc.

- 6.4.18 Adobe Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment