PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044057

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044057

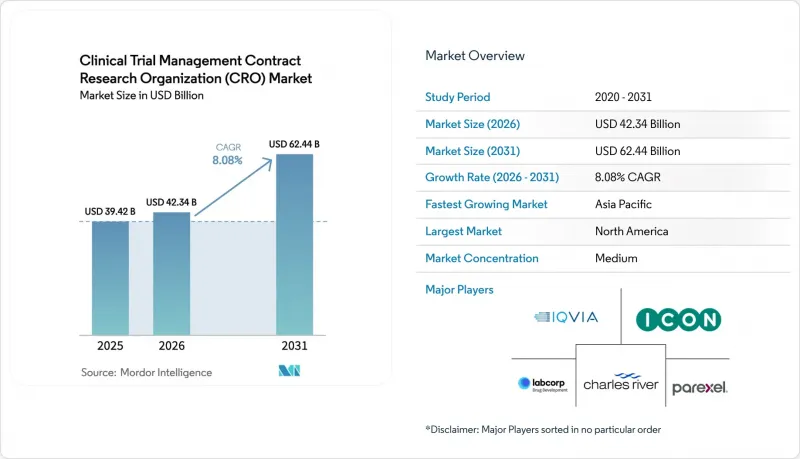

Clinical Trial Management Contract Research Organization (CRO) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Clinical Trial Management Contract Research Organization Market was valued at USD 39.42 billion in 2025 and expected to grow from USD 42.34 billion in 2026 to reach USD 62.44 billion by 2031, at a CAGR of 8.08% during the forecast period (2026-2031).

Growing therapeutic complexity, tighter regulatory oversight, and the escalating costs of in-house trial infrastructure push sponsors toward full-service partners that can coordinate global studies seamlessly. Hybrid and decentralized models, validated by the FDA in 2024, shave 15-25% off per-patient costs and improve retention, making them a centerpiece of sponsor sourcing strategies. Oncology's capital-intensive protocols, Bayesian adaptive designs, and the surge of GLP-1 cardiovascular outcome studies collectively sustain premium pricing for specialist providers. Meanwhile, AI-enabled patient matching platforms and unified data lakes give technology-forward CROs an edge in bid defense, while sponsors reward end-to-end offerings that compress cycle times and bolster data integrity. Altogether, the Clinical Trial Management CRO market is positioned for durable double-digit expansion as outsourcing shifts from transactional staffing to strategic, analytics-driven partnerships.

Global Clinical Trial Management Contract Research Organization (CRO) Market Trends and Insights

Increasing Pharmaceutical R&D Outsourcing to CROs

More than half of all sponsor clinical budgets flowed to external providers in 2024, up 5 percentage points since 2020, as leaner R&D headcounts and pipeline diversity made vertical integration less feasible. Mid-cap biotechs outsourced majority of operations, using milestone-based contracts that shift risk yet accelerate market entry by roughly eight months for oncology assets. The Clinical Trial Management CRO market benefits because sponsors now extend outsourcing upstream into discovery biology and toxicology, enlarging deal scope from individual trials to multi-asset platforms. Risk-sharing terms align incentives but pressure CRO balance sheets, prompting larger players to build cash reserves or secure revolving credit lines. Government grant flows, particularly the NIH's USD 3.2 billion infrastructure pool in 2024, funnel academic studies toward CRO support, broadening the addressable client base.

Rising Complexity of Clinical Trials and Regulatory Requirements

Median Phase III oncology trials enrolled 800 patients across 150 sites in 2024, as regulators insisted on broader demographic representation . Bayesian adaptive designs, codified in FDA guidance in March 2024, require specialized biostatistical skills available to only about one-third of sponsors, increasing reliance on CRO analytics teams. Europe's Clinical Trial Regulation, fully live from January 2025, will require centralized submission via CTIS and tightened reporting timelines, compelling IT investments that only large CROs can absorb comfortably. Japan's real-world evidence mandate and China's alignment with ICH E6(R3) further elevate compliance hurdles. As a result, scale and capital intensity force consolidation, lifting the Clinical Trial Management CRO market entry barrier for smaller firms.

Investigator Site Capacity Constraints and Patient Recruitment Challenges

North American site availability fell 8% in 2024 because burnout prompted principal investigators to scale back commitments. Activation timelines stretched to 16 weeks, delaying first-patient-in schedules, while oncology recruitment failure hit 37%. Predictive analytics platforms mitigate risk but require multi-year data histories, delaying ROI. India's 240 newly certified sites and China's 60-day approvals offer relief, yet linguistic and consent-form nuances slow turn-on, reinforcing site shortfalls that temporarily temper Clinical Trial Management CRO market growth.

Other drivers and restraints analyzed in the detailed report include:

- Growing Prevalence of Chronic Diseases Driving Trial Volume

- Adoption of Decentralized and Hybrid Trial Models

- Data Integrity Concerns and Regulatory Scrutiny of CRO Operations

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Clinical Services captured 54.1% of the Clinical Trial Management CRO market revenue in 2025, reflecting a clear sponsor bias for single-vendor accountability around protocol, data, and regulatory deliverables. The Clinical Trial Management CRO market size for full-service contracts continues to widen as complex oncology and GLP-1 mega-trials reward integrated execution models. Sponsors accept higher fees because unified quality oversight reduces re-work and inspection findings. Discovery outsourcing, forecast at 8.56% CAGR to 2031, gains traction with platform biotechs that lack vivaria or assay labs. Concurrently, pharmacovigilance and medical-writing demand rises as post-marketing commitments multiply under real-world evidence guidelines.

Functional service providers (FSPs) reported significant revenue growth in 2025, supplying embedded biostatisticians, data managers, and medical writers on variable terms that appeal to cash-constrained biotechs. Yet scaling FSP engagements to global Phase III demands hybrid models that blend staff augmentation with centralized governance. AI-driven screening has trimmed labor hours in discovery assays, pressuring margins, so CROs race to patent proprietary cell and disease models that command premium licensing fees. The Clinical Trial Management CRO industry increasingly views technology ownership, not merely headcount, as the determinant of long-run profitability.

Oncology held 30.40% of the Clinical Trial Management CRO market share in 2025. High-dose antibody-drug conjugate protocols require specialized infusion centers and intricate safety monitoring, driving per-study values above USD 100 million. Infectious diseases, while a smaller base, is the fastest-growing segment at 8.99% CAGR as governments invest in pandemic readiness platforms. Cardiovascular-metabolic outcome trials, catalyzed by GLP-1 classes, enroll 5,000+ patients, creating blockbuster engagements with longitudinal follow-up that stick CROs to sponsors for 5-7 years.

Neurology studies struggle with rare-disease recruitment, but the segment remains lucrative because decentralized cognitive assessments lower participant burden and extend geographic reach. Immunology trials increasingly depend on multi-omics biomarkers, pushing CROs to build central lab alliances. Respiratory projects moderated in 2024 after COVID-19 tapering; however, long-COVID and asthma biologics partially offset the dip. Master protocol guidance from April 2024 favors CROs with deep therapeutic benches capable of running multi-arm, multi-drug platforms, enhancing differentiation within the Clinical Trial Management CRO market.

The Clinical Trial Management Contract Research Organization (CRO) Market Report is Segmented by Service Type (Discovery Services, Pre-Clinical Services and More), Therapeutic Area (Oncology, CNS / Neurology and More), Clinical Phase (Pre-Clinical, Phase I and More), End-User (Pharmaceutical and Biopharmaceutical Companies, and More), and Geography (North America, Europe, and More). Market Forecasts are in Value (USD).

Geography Analysis

North America generated 38.90% of 2025 revenue as the Clinical Trial Management CRO market anchor, owing to dense investigator networks, high sponsor headcount, and swift FDA guidance cycles. Yet average Phase III per-patient costs reached USD 60,000, motivating geographic diversification. Decentralized models, cleared by the FDA in 2024, cut site visit frequency and leverage EMR-based endpoints, reducing direct costs by about one-fifth. Still, site capacity pressures persist; U.S. centers managed 12 concurrent protocols in 2024, elevating deviation rates that compel CROs to raise monitoring budgets. Asia-Pacific will expand at 8.32% CAGR through 2031, underpinned by China's 60-day approvals and India's 240 newly certified sites. Harmonization with ICH E6(R3) in 2024 calmed sponsor concerns about Chinese data acceptability . India's corporate hospital networks provide standardized electronic records, but regional ethics committees add cycle time variability. Japan's English-language pathway, introduced in 2024, trims documentation lead times, though its aging population complicates naive-patient recruitment. Southeast Asian countries entice early-phase oncology trials with cost savings near 50%, yet regulator capacity lags, extending dossier review.

Europe retained stable share after the January 2025 CTIS launch unified submissions across 27 member states. Centralized portals slice administrative load, but Brexit imposes duplicate filings for U.K. sites, fragmenting what was once a contiguous region. Eastern Europe offers 40-50% lower per-patient costs but geopolitical risk reduced trial placements 12% in 2024. The Middle East & Africa and South America are emerging zones; South Africa's harmonized ethics approvals and disease epidemiology position it as the sub-Saharan beachhead, while Brazil's ANVISA backlog remains a gating factor for rapid study start-ups. Collectively, these dynamics ensure the Clinical Trial Management CRO market enjoys balanced regional growth without over-reliance on any single geography.

- Allucent

- Caidya

- Charles River Labs

- Ergomed

- Fortrea

- ICON

- IQVIA

- LabCorp

- Linical

- MedPace

- Novotech

- Orphan-Reach

- Parexel International

- Precision for Medicine

- PROMETRIKA

- Quanticate

- Simbec Orion

- Syneos Health

- Thermo Fisher Scientific

- Veristat

- Worldwide Clinical Trials

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Pharmaceutical R&D Outsourcing

- 4.2.2 Rising Trial and Regulatory Complexity

- 4.2.3 Growing Chronic-Disease Trial Volume

- 4.2.4 Adoption of Decentralized and Hybrid Models

- 4.2.5 Technological Advancements in AI And Data Analytics for Trial Optimization

- 4.2.6 Expansion of Rare-Disease and Orphan-Drug Development Programs

- 4.3 Market Restraints

- 4.3.1 Investigator-Site Capacity and Recruitment

- 4.3.2 Data-Integrity Scrutiny of CRO Operations

- 4.3.3 High Costs of Clinical Trials Are Limiting Sponsor Budgets and Trial Starts

- 4.3.4 Shortage of Qualified Clinical Research Professionals and Investigator Burnout

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts (Value, USD)

- 5.1 By Service Type

- 5.1.1 Discovery Services

- 5.1.2 Pre-clinical Services

- 5.1.3 Clinical Services

- 5.1.4 Others

- 5.2 By Therapeutic Area

- 5.2.1 Oncology

- 5.2.2 CNS / Neurology

- 5.2.3 Cardiovascular & Metabolic

- 5.2.4 Infectious Diseases

- 5.2.5 Immunology / Inflammatory

- 5.2.6 Respiratory

- 5.2.7 Others

- 5.3 By Clinical Phase

- 5.3.1 Pre-clinical

- 5.3.2 Phase I

- 5.3.3 Phase II

- 5.3.4 Phase III

- 5.3.5 Phase IV

- 5.4 By End-Users

- 5.4.1 Pharmaceutical and Biopharmaceutical Companies

- 5.4.2 Medical Devices companies

- 5.4.3 Academic & Research Institutes

- 5.4.4 Government & Non-Profit Organisations

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Spain

- 5.5.2.6 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 India

- 5.5.3.3 Japan

- 5.5.3.4 South Korea

- 5.5.3.5 Australia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 Middle East and Africa

- 5.5.4.1 GCC

- 5.5.4.2 South Africa

- 5.5.4.3 Rest of Middle East and Africa

- 5.5.5 South America

- 5.5.5.1 Brazil

- 5.5.5.2 Argentina

- 5.5.5.3 Rest of South America

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Market Share Analysis

- 6.3 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.3.1 Allucent

- 6.3.2 Caidya

- 6.3.3 Charles River Labs

- 6.3.4 Ergomed

- 6.3.5 Fortrea

- 6.3.6 ICON plc

- 6.3.7 IQVIA

- 6.3.8 Labcorp Drug Development

- 6.3.9 Linical

- 6.3.10 Medpace

- 6.3.11 Novotech

- 6.3.12 Orphan-Reach

- 6.3.13 Parexel

- 6.3.14 Precision for Medicine

- 6.3.15 PROMETRIKA

- 6.3.16 Quanticate

- 6.3.17 Simbec Orion

- 6.3.18 Syneos Health

- 6.3.19 Thermo Fisher

- 6.3.20 Veristat

- 6.3.21 Worldwide Clinical Trials

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment