PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044059

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044059

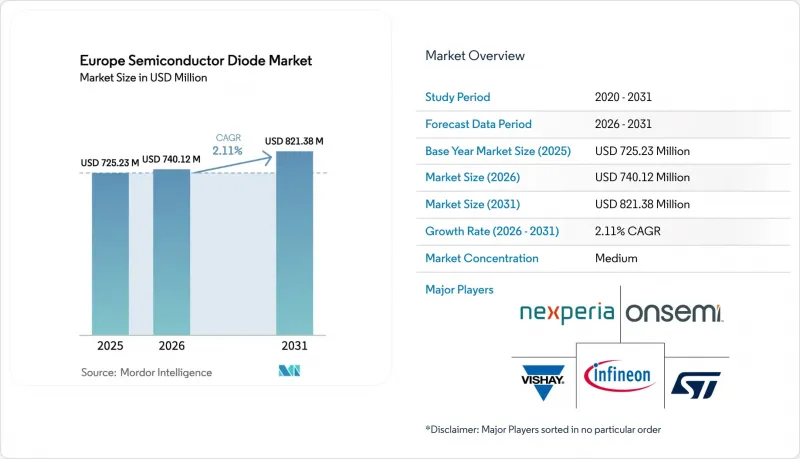

Europe Semiconductor Diode - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe Semiconductor Diode Market size was valued at USD 725.23 million in 2025 and is estimated to grow from USD 740.12 million in 2026 to reach USD 821.38 million by 2031, at a CAGR of 2.11% during the forecast period (2026-2031).

A gradual pivot toward wide-bandgap materials is unfolding as silicon carbide (SiC) and gallium nitride (GaN) capture automotive and industrial sockets, while legacy silicon remains entrenched in cost-sensitive consumer and telecom gear. Germany's public-private megaprojects, including the EUR 10 billion (USD 11.61 billion) ESMC fab and Infineon's Smart Power Fab, are anchoring regional capacity corridors and stimulating design-in activity for 200 mm SiC wafers. Italy's Catania cluster, backed by EUR 5 billion (USD 5.80 billion) for STMicroelectronics' SiC device line and EUR 730 million (USD 847.26 million) for captive substrate output, demonstrates how Chips Act incentives funnel capital toward vertical integration. Schottky rectifiers keep their central role in server power supplies and EV on-board chargers, yet transient-voltage-suppression (TVS) arrays for USB4, Thunderbolt and automotive Ethernet outpace all other device classes. Elevated electricity tariffs 197 EUR/MWh in early 2024 squeeze fab margins, but policy continuity after the September 2025 Semicon Coalition declaration signals further tailwinds for advanced-node and wide-bandgap investment.

Europe Semiconductor Diode Market Trends and Insights

E-Mobility Led SiC-Schottky Pull-Through

Battery-electric vehicles moving to 800 V platforms are the prime catalyst for SiC Schottky demand in Europe, as OEMs seek faster charging and lighter copper harnesses. STMicroelectronics logged design wins with Geely and Hyundai for fourth-generation SiC MOSFETs co-packaged with Schottky diodes for SOP-2026 lines. Infineon's HybridPACK Drive G3, rolled out in late 2024, integrates CoolSiC MOSFETs and free-wheeling diodes for German premium brands. Transitioning to 200 mm SiC wafers at Catania and Wolfspeed Saarland is expected to trim die cost per ampere by 20-25% by 2027. Yet EU anti-subsidy duties of 17-35.3% on Chinese BEV imports have softened near-term unit pull-through, and AEC-Q101 Grade 0 validation pushes product-launch lead-times out by 12-18 months.

Expansion of EU Chips Act Funding Pipeline

Seven first-of-a-kind fabs approved under the Chips Act have secured EUR 31.5 billion (USD 36.56 billion) in combined spending, with three dedicated to wide-bandgap devices. STMicroelectronics alone commands EUR 5 billion (USD 5.80 billion) for device capacity and EUR 730 million (USD 847.21 million) for substrates in Sicily, while onsemi allocates EUR 1.64 billion (USD 1.90 billion) to Roznov SiC expansion. Spain's Imec-backed Malaga center and the EUR 700 million NanoIC pilot line, funded in February 2026, give SMEs 300 mm access and de-risk advanced-node prototyping. The Semicon Coalition's call for a "Chips Act 2.0" could unlock another EUR 20-30 billion (USD 23.21 -34.82 billion) in private capital by 2028.

SiC Substrate Cost Delta vs. Si Greater Than 6X

Substrates account for half of finished SiC diode cost and still price out at six times equivalent silicon wafers, hindering broader penetration. Moving from 150 mm to 200 mm cuts cost per square centimeter by roughly 20% by 2027, yet the absolute premium stays quadruple that of silicon through 2031. Vertical integration at STMicro and Infineon remains the chief hedge against volatile spot markets.

Other drivers and restraints analyzed in the detailed report include:

- Telecom 5G / FTTx Rectifier Renewal

- EV On-Board Charger Design-Wins for GaN TVS

- Automotive OEM PPAP Backlog Less Than18 Months

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Schottky devices represented 43.12% of the Europe semiconductor diode market size in 2025, a share rooted in their sub-0.5 V forward drop that improves synchronous rectifier efficiency in EV chargers and server PSUs. Zener and small-signal diodes serve as references and for switching, while TVS and ESD arrays post the steepest 2.36% CAGR thanks to USB4 and automotive Ethernet rollouts.

More OEMs now specify GaN TVS for 48 V mild-hybrid buses, citing order-of-magnitude lower capacitance than silicon counterparts. Schottky demand also benefits from 5G base-station retrofits that require less than 10 ns of reverse recovery time. Niche laser diodes for LiDAR contribute under 5% of revenue but see solid traction in 905 nm edge-emitting designs, even as VCSEL alternatives loom.

Silicon retained 71.43% Europe semiconductor diode market share in 2025, underpinned by its mature supply chain, abundant wafer capacity and decades-long reliability data favored by consumer, telecom and low-voltage industrial buyers. Silicon carbide, though still a minority material, is pacing a 2.44% CAGR to 2031 as 800 V traction inverters, 650 V servo drives and 350 kW grid-scale battery chargers demand 30-40% lower switching losses than silicon can deliver. STMicroelectronics' Catania hub targets 15,000 200 mm wafers per week by 2033, while onsemi's Roznov line will push 40,000 150 mm wafers annually by 2027, moves that could lift SiC's slice of the Europe semiconductor diode market size toward 9-10% over the forecast horizon. Gallium nitride, holding barely 3% volume in 2025, is carving footholds in 11 kW on-board chargers and 48 V mild-hybrid DC-DC converters, where 500 kHz switching shrinks inductors and raises power density in cramped engine bays. Emerging ultra-wide-bandgap options such as gallium oxide remain pre-commercial, but EU-funded pilot lines like NanoIC are sampling demonstrator diodes that withstand over 3 kV reverse bias at junction temperatures above 200 °C.

Vertical-integration plays are rewriting cost curves: STMicroelectronics' EUR 730 million captive-substrate project seeks to internalize 40% of its SiC wafer demand by 2026, cutting exposure to spot-market swings and shaving die cost per ampere by nearly one-quarter. Infineon pursues a similar hedge at Dresden, shifting to 200 mm SiC production today and piloting 300 mm lots for post-2027 ramps. Device makers without in-house boule capacity, including GeneSiC and Littelfuse subsidiaries, increasingly lock multi-year substrate supply contracts or pivot toward GaN where wafer economics are comparatively benign. Silicon will still dominate low-voltage sockets USB power bricks, set-top boxes, home appliances-yet its region-wide share is likely to dip to the high-sixties by 2031 as automotive, renewable-energy and heavy-industry clients standardize on wide-bandgap rectifiers for efficiency mandates and lifetime cost reductions.

The Europe Semiconductor Diode Market Report is Segmented by Type (Schottky, Zener, and More), Base Material (Silicon, Silicon Carbide, and More), End-Use Industry (Automotive and Transportation, Consumer Electronics, and More), Application (Power Rectification and Conversion, and More), Package Type (Surface Mount, and Through-Hole), and Country (Germany, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Infineon Technologies AG

- STMicroelectronics N.V.

- Nexperia B.V.

- Vishay Intertechnology, Inc.

- onsemi Corporation

- ROHM Co., Ltd.

- Littelfuse, Inc.

- Toshiba Electronic Devices and Storage Corp.

- Renesas Electronics Corp.

- Hitachi Power Semiconductor Device Ltd.

- Mitsubishi Electric Corp.

- Microchip Technology Inc.

- Central Semiconductor Corp.

- WeEn Semiconductors

- Semikron Danfoss

- GeneSiC Semiconductor

- ABB Semiconductors

- Diotec Semiconductor AG

- IXYS (Littelfuse)

- Wolfspeed, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Mobility Led SiC-Schottky Pull-Through

- 4.2.2 Expansion of EU Chips Act Funding Pipeline

- 4.2.3 Telecom 5G / FTTx Rectifier Replacement Cycle

- 4.2.4 EV On-Board Charger Design-Wins for GaN TVS

- 4.2.5 Power-Dense Data-Centre PSUs Less Than 3 kW

- 4.2.6 Edge-AI Industrial Drives Less Than 650 V

- 4.3 Market Restraints

- 4.3.1 SiC Substrate Cost Delta vs. Si Greater Than 6x

- 4.3.2 Automotive OEM PPAP Backlog Less Than 18 Months

- 4.3.3 EU Energy-Price Volatility on Fab OPEX

- 4.3.4 Trade-Remedy Tariffs on Chinese BEV Imports

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 Schottky

- 5.1.2 Zener

- 5.1.3 TVS / ESD

- 5.1.4 Laser

- 5.1.5 Small-Signal Switching

- 5.1.6 Other Types

- 5.2 By Base Material

- 5.2.1 Silicon (Si)

- 5.2.2 Silicon Carbide (SiC)

- 5.2.3 Gallium Nitride (GaN)

- 5.2.4 Other Base Materials

- 5.3 By End-Use Industry

- 5.3.1 Automotive and Transportation

- 5.3.2 Consumer Electronics

- 5.3.3 Communications Infrastructure

- 5.3.4 Industrial Automation and Power

- 5.3.5 Computing and Data Centre

- 5.3.6 Other End-Use Industries

- 5.4 By Application

- 5.4.1 Power Rectification and Conversion

- 5.4.2 Voltage Regulation and Reference

- 5.4.3 Electrostatic / Surge / Circuit Protection

- 5.4.4 Other Applications

- 5.5 By Package Type

- 5.5.1 Surface Mount (SMD)

- 5.5.2 Through-Hole

- 5.6 By Country

- 5.6.1 Germany

- 5.6.2 United Kingdom

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank / Share, Products and Services, Recent Developments)

- 6.1.1 Infineon Technologies AG

- 6.1.2 STMicroelectronics N.V.

- 6.1.3 Nexperia B.V.

- 6.1.4 Vishay Intertechnology, Inc.

- 6.1.5 onsemi Corporation

- 6.1.6 ROHM Co., Ltd.

- 6.1.7 Littelfuse, Inc.

- 6.1.8 Toshiba Electronic Devices and Storage Corp.

- 6.1.9 Renesas Electronics Corp.

- 6.1.10 Hitachi Power Semiconductor Device Ltd.

- 6.1.11 Mitsubishi Electric Corp.

- 6.1.12 Microchip Technology Inc.

- 6.1.13 Central Semiconductor Corp.

- 6.1.14 WeEn Semiconductors

- 6.1.15 Semikron Danfoss

- 6.1.16 GeneSiC Semiconductor

- 6.1.17 ABB Semiconductors

- 6.1.18 Diotec Semiconductor AG

- 6.1.19 IXYS (Littelfuse)

- 6.1.20 Wolfspeed, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment