PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044063

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044063

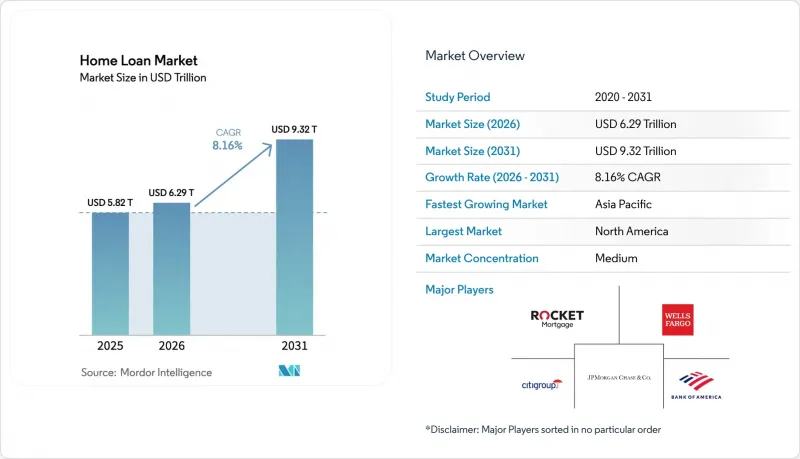

Home Loan - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The home loan market size was valued at USD 5.82 trillion in 2025 and estimated to grow from USD 6.29 trillion in 2026 to reach USD 9.32 trillion by 2031, at a CAGR of 8.16% during the forecast period (2026-2031).

Robust demographic expansion, steady urban migration, and the rapid digitization of mortgage workflows continue to keep annual origination volumes on an upswing despite tightening monetary conditions. Technology-enabled lenders are compressing approval cycles from weeks to days, lowering operating costs and broadening access to credit, especially in underserved regions. Government-backed affordable-housing schemes across emerging markets, together with ESG-linked incentives for energy-efficient dwellings, are further enlarging the total addressable borrower base. At the same time, cross-border labor mobility and the revival of private-label securitization are unlocking new revenue streams for specialized lenders, offsetting headwinds from elevated policy rates and stricter macro-prudential rules.

Global Home Loan Market Trends and Insights

Rapid Rise of Digital-First Mortgage Platforms

Digital-first originators shorten application cycles by up to 20-fold while reducing processing expenses nearly 80%, letting lenders price aggressively and still improve margins. They reach borrowers in locations where branch networks are uneconomical, widening the home loan market. Automated marketing analytics lower acquisition costs and raise conversion ratios, supporting sustained share gains. End-to-end integrations with agents, appraisers, and title firms compress closing timelines, lifting industry throughput. Continuous, 24/7 application status feeds meet rising consumer expectations, decreasing abandonment rates, and stabilizing revenue flows.

AI-Driven Credit Scoring Broadening Borrower Pool

Machine-learning models ingest rental histories, utility payments, and gig-economy income to evaluate creditworthiness beyond traditional scores, enabling previously excluded segments to qualify responsibly. Real-time fraud screens enhance risk controls, aligning with regulatory mandates. Government-sponsored enterprise connectivity streamlines secondary-market execution, freeing up capital for further origination. AI chatbots capture borrower data in MISMO-compliant formats, cutting manual entry and speeding approvals. This approach is particularly beneficial for self-employed professionals, enlarging the effective home loan market.

Persistently High Policy Rates

The U.S. 30-year fixed mortgage rate has hovered above 7% since January 2025 and is widely expected to stay above 6% until 2026, dampening affordability and refinancing volumes. Similar pressures are visible in the UK, where the Bank of England delays substantive rate cuts amid lingering inflation concerns. Eurozone averages have climbed to about 4%, and Canadian borrowers face payment shocks as USD 300 billion in mortgages reset over the next year. Elevated rates deter prospective buyers and lock existing owners into low-coupon loans, muting transaction volumes and slowing home loan market expansion.

Other drivers and restraints analyzed in the detailed report include:

- Government-Backed Affordable-Housing Push

- Acceleration of Green-Home Incentives

- Tightening Macro-Prudential Rules

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Purchase financing dominated 2025 with 62.36% home loan market share and is forecasted to expand at a 8.91% CAGR through 2031, underscoring enduring owner-occupier demand even amid higher borrowing costs. Urban immigration, rising household formation, and growing middle-class wealth in emerging economies are pivotal contributors. Renovation and improvement loans are gaining ground as homeowners unlock accumulated equity to fund energy-efficient upgrades, encouraged by green-subsidy programs. Refinance activity, which had surged during pandemic-era rate cuts, now accounts for a modest slice of the home loan market as less than 3% of outstanding borrowers can economically refinance at prevailing rates. Lenders are therefore refocusing technology investment on purchase-money efficiencies, leveraging AI-driven underwriting to close deals quickly in competitive housing markets.

Lower average ticket sizes in emerging cities, combined with government guarantee schemes, are broadening lender portfolios while mitigating credit risk. In contrast, construction loans remain cyclical, reflecting developer confidence and local regulatory frameworks. Growth prospects through 2031 remain strongest in markets where public housing initiatives dovetail with digital lending adoption, signaling a healthy pipeline for the home loan market.

Traditional banks held a 66.81% share in the global home loan market in 2025, benefiting from low-cost deposit funding that supports competitive fixed-rate offers. Nevertheless, fintech and non-bank entities are expanding at a 14.84% CAGR, propelled by agile technology stacks and lighter capital constraints. Housing-finance companies bridge the two models in markets such as India, where Bajaj Housing Finance's USD 16 billion IPO illustrated investor confidence in specialized lenders. Non-bank lenders in Australia, whose collective book stands at USD 74 billion, are on track to double assets within five years, evidencing global momentum toward alternative funding channels. The home loan market size attributable to these challenger segments is increasing as they target self-employed borrowers and near-prime profiles underserved by banks.

Regulatory arbitrage and securitization access help sustain the growth trajectory, while partnerships with digital-first platforms shorten time-to-yes decisions. Banks are responding by integrating robo-underwriting and adopting cloud-native loan origination systems, but cultural change and legacy infrastructure remain hurdles. Through 2031, the competitive gap is likely to narrow, yet diversified funding bases and niche specializations keep alternative lenders structurally advantaged in specific borrower cohorts within the home loan market.

The Global Home Loan Market Report is Segmented by Loan Purpose (Purchase, Home Improvement/Renovation, Others), Provider (Banks, Housing Finance Companies, Others), Interest Rates (Fixed Interest Rates, Floating Interest Rates), Loan Tenure (Less Than or Equal To 10 Years, 11 - 20 Years, and More), and Geography (North America, South America, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America commanded 40.32% of the global home loan market share in 2025, underpinned by the U.S. secondary-market machinery in which Ginnie Mae guarantees continue to attract 25-33% foreign investment into mortgage-backed securities. Elevated rates above 7% and low existing inventory suppress transaction throughput, evidenced by 26% of 2024 purchases closing in cash. Canada faces USD 300 billion in 2025 renewals, testing household resilience as fixed terms written during 2020 roll off.

Asia-Pacific is the fastest-growing geography, projected at a 9.86% CAGR, as India records an 11-year high of 173,000 unit sales during H1 2024 and anticipates the real-estate sector tripling to USD 1.5 trillion by 2034. China's policy move to trim mortgage rates by 50 basis points and relax second-home down payments to 15% could benefit 50 million households. Mature markets like Australia see durable demand linked to high net migration and tight supply, whereas Japan emphasizes urban redevelopment to offset demographic decline.

Europe shows tentative recovery with Q4 2024 nominal home prices up 4.9% year over year, though divergence is stark: German prices fell 7.1% while Poland rose 13%. Mortgage production has sagged amid 4% average rates, and French outstanding balances dipped 0.65% to EUR 1.424 trillion by mid-2024. The Netherlands expects rates to edge lower to 3-3.5% by late 2025, yet continued supply shortages push average transaction values toward EUR 488,000.

- Rocket Mortgage (Quicken Loans)

- Wells Fargo & Co.

- Bank of America Corporation

- JPMorgan Chase & Co.

- Citigroup Inc.

- HSBC Group

- Goldman Sachs (Marcus)

- Charles Schwab & Co.

- Morgan Stanley

- U.S. Bank

- Barclays plc

- BNP Paribas Personal Finance

- Santander Consumer Finance

- ANZ Bank

- Commonwealth Bank of Australia

- China Construction Bank

- ICICI Bank Ltd.

- LIC Housing Finance Ltd.

- Dewan Housing Finance Corp. Ltd.

- Nationwide Building Society

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid rise of digital first mortgage origination platforms

- 4.2.2 AI-driven credit scoring expanding borrower pool

- 4.2.3 Government-backed affordable-housing push in emerging markets

- 4.2.4 Acceleration of green-home incentives & ESG-linked mortgages

- 4.2.5 Cross-border labour mobility boosting expatriate home-buy demand

- 4.2.6 Expansion of private-label securitisation reviving lender liquidity

- 4.3 Market Restraints

- 4.3.1 Persistently high policy rates in key economies

- 4.3.2 Tightening macro-prudential rules on loan-to-value & debt-to-income

- 4.3.3 Rising climate-risk insurance premiums in coastal zones

- 4.3.4 Fin-crime compliance costs squeezing thin-margin lenders

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

5 Market Size & Growth Forecasts (Value)

- 5.1 By Loan Purpose

- 5.1.1 Purchase (New/Existing)

- 5.1.2 Home Improvement/Renovation

- 5.1.3 Others (Construction, Refinance, etc.)

- 5.2 By Provider

- 5.2.1 Banks

- 5.2.2 Housing Finance Companies

- 5.2.3 Others

- 5.3 By Interest Rates

- 5.3.1 Fixed Interest Rates

- 5.3.2 Floating Interest Rates

- 5.4 By Loan Tenure

- 5.4.1 Less than or equal to 10 Years

- 5.4.2 11 - 20 Years

- 5.4.3 Longer than 20 Years

- 5.5 By Region

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Colombia

- 5.5.2.5 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Spain

- 5.5.3.5 Italy

- 5.5.3.6 Benelux (Belgium, Netherlands, and Luxembourg)

- 5.5.3.7 Nordics (Sweden, Norway, Denmark, Finland, and Iceland)

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 South-East Asia (Singapore, Indonesia, Malaysia, Thailand, Vietnam, and Philippines)

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle East and Africa

- 5.5.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for Key Companies, Products & Services, and Recent Developments)

- 6.4.1 Rocket Mortgage (Quicken Loans)

- 6.4.2 Wells Fargo & Co.

- 6.4.3 Bank of America Corporation

- 6.4.4 JPMorgan Chase & Co.

- 6.4.5 Citigroup Inc.

- 6.4.6 HSBC Group

- 6.4.7 Goldman Sachs (Marcus)

- 6.4.8 Charles Schwab & Co.

- 6.4.9 Morgan Stanley

- 6.4.10 U.S. Bank

- 6.4.11 Barclays plc

- 6.4.12 BNP Paribas Personal Finance

- 6.4.13 Santander Consumer Finance

- 6.4.14 ANZ Bank

- 6.4.15 Commonwealth Bank of Australia

- 6.4.16 China Construction Bank

- 6.4.17 ICICI Bank Ltd.

- 6.4.18 LIC Housing Finance Ltd.

- 6.4.19 Dewan Housing Finance Corp. Ltd.

- 6.4.20 Nationwide Building Society

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment