PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044072

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044072

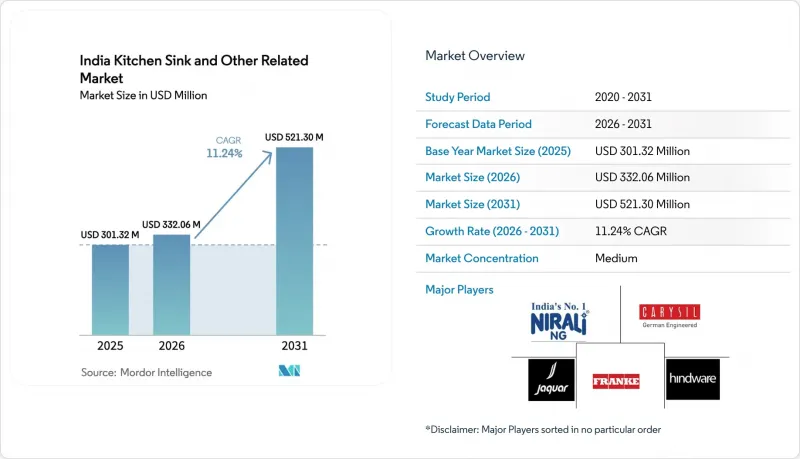

India Kitchen Sink And Other Related - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The India kitchen sink and other related market size is expected to increase from USD 301.32 million in 2025 to USD 332.06 million in 2026 and reach USD 521.3 million by 2031, growing at a CAGR of 11.24% over 2026-2031.

Residential apartment handovers in Mumbai, Delhi NCR, and Bengaluru anchor fixture purchases and create predictable order cycles for organized brands that are specified at the construction stage. Modular-kitchen adoption in tier-1 and tier-2 households is accelerating the shift to integrated sink-faucet ecosystems and workstation-led accessories, lifting average selling prices and cross-sell rates for premium portfolios. Digital channels are shortening discovery and purchase cycles, with online marketplaces already contributing a meaningful slice of sales and projected to grow faster than traditional outlets through 2031. Quality-control enforcement under Indian standards is consolidating supply toward ISI-marked, QR-verifiable products, which supports trust-based retailing in large-format chains and government procurement. Stainless steel remains the workhorse material but faces margin pressure from input-cost swings, while value-added quartz composites are gaining traction due to design latitude and perceived durability benefits among urban renovators.

India Kitchen Sink And Other Related Market Trends and Insights

Accelerating Modular-Kitchen Adoption in Urban India

India's modular-kitchen category is scaling as households prioritize compact layouts, storage efficiency, and integrated fixtures, with spending on coordinated sinks and faucets rising alongside cabinetry and countertop upgrades. Developers in premium apartment projects have moved pre-bundle branded sinks into handovers to standardize finish quality and reduce post-occupancy service calls, which sets a benchmark that influences later retrofit cycles in the same micro-markets. Urban consumers are treating the kitchen as a social and functional center, which supports demand for workstation-style sinks that integrate accessories and improve prep ergonomics. Organized brands are deepening collaboration with modular-kitchen OEMs and gallery networks, so sinks are specified early in the design, a shift that results in larger order values and lower return rates than aftermarket replacements. Penetration beyond metros remains a runway as tier-2 and tier-3 households seek aspirational upgrades and respond to experiential showrooms and digital visualization tools that clarify fit and finish choices.

Housing Completions and New Launches Supporting Sink Demand

Residential unit deliveries across India's top markets rose in FY25, and the 406,889 completed units reported for the top nine cities translate directly into first-fix demand for sinks specified by developers and contractors. Premium projects in larger cities are increasingly opting for dual-mount or undermount formats that elevate countertop continuity and visual appeal, which then shape homeowner expectations in the resale and renovation cycles. Mid-market launches often choose durable stainless-steel models to meet cost and maintenance criteria, reinforcing the breadth of price points within the India kitchen sink and other related markets. As launches and land acquisitions extend deeper into tier-2 locations, organized brands gain access to markets that were once served mainly by local fabricators, opening room for certified products and structured warranties. The tilt toward high-specification housing sustains a pathway for value-added sink materials and accessories that deliver visible differentiation for buyers upgrading kitchens as part of broader interior investments.

Unorganized Price Competition in Stainless Steel

Price-led competition from unorganized fabricators continues to strain entry-level SKUs, especially in rural and tier-3 corridors where cash-and-carry buying and hyper-local distribution are entrenched. These vendors typically avoid certification costs and operate at lower overheads, which enables sharp undercutting against branded 304-grade offerings that meet formal specifications. The result is a constraint on premium-feature adoption at the lowest price tiers, slowing the migration to noise-dampening pads, anti-condensation coatings, and accessory-ready ledges. As quality-control orders tighten and ISI marking becomes mainstream in procurement, traceable SKUs gain an advantage in large-format retail and public tenders, which can shift demand toward organized labels over time. For brands, the near-term response centers on education, warranty reinforcement, and dealer-incentive structures that highlight lifecycle value rather than headline price.

Other drivers and restraints analyzed in the detailed report include:

- Omnichannel Retail Expansion for Kitchen Hardware

- Premiumization Toward Quartz/Granite Aesthetics

- Raw-Material Cost Volatility Pressuring Margins

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Stainless steel accounted for 84% share in 2025, and quartz composites are projected to advance at a 16.39% CAGR through 2031 as design-led formats gain attention among urban homeowners. Stainless steel remains the primary choice across budgets due to corrosion resistance, installer familiarity, and a broad catalog of sizes that fit Indian kitchens. Its ubiquity also reflects wide dealer coverage in traditional hardware stores and plumber-led channels that influence sink selection at the installation stage. Over the forecast horizon, cost spikes in steel inputs and rising preference for coordinated aesthetics with engineered-stone surfaces support incremental share gains for composites. The India kitchen sink and other related market benefits, as organized labels scale workstation-led offerings that integrate cutting boards, racks, and colanders for compact counters and dual-income households.

Quartz composites enable color-matched installations and seamless visual lines with granite or engineered-stone counters, which premium developers and modular-kitchen integrators highlight in showflats and studios. As experiential retail expands, homeowners can map accessories fit and clearance in galleries and through digital visualizers, which reduces post-install friction. Certified products and QR-verifiable markings also become important as retailers and public buyers emphasize traceability, and these elements further formalize the India kitchen sink and other related market size for higher-spec materials tied to warranties and service. Organized suppliers with diversified portfolios can spread certification costs and inventory planning across multiple SKUs, which supports steady availability in popular sizes. In parallel, capacity additions in composites by integrated players support faster lead times and ensure consistency that benefits both builders and renovators.

Top-mount installations held 30% share in 2025, while dual-mount formats are forecast to grow at a 12.26% CAGR through 2031 as homeowners seek flexibility to switch between drop-in and undermount placements during renovation cycles. Undermount formats improve wipe-down convenience and visual continuity on stone counters but require skilled installers and precision tools that are unevenly available outside metros. This capability gap slows undermount adoption in semi-urban markets where installers may charge premiums for stone cutting and epoxy sealing. Dual-mount designs bridge this gap by allowing drop-in installation today and an undermount switch later without replacing the sink, which aligns with phased remodel budgets. As a result, the India kitchen sink and other related market sees higher accessory attachment on dual-mount SKUs, particularly where workstation ledges add prep efficiency in compact kitchens.

Premium galleries and modular-kitchen studios often showcase undermount and dual-mount side by side, which helps buyers visualize task flows and cleaning routines. Organized brands are standardizing clip systems and edge profiles to simplify reconfiguration and reduce installer time on site. This also supports service networks that can guarantee fit across common countertop thicknesses and stone types. The India kitchen sink industry uses these upgrade paths to improve lifecycle value and encourage repeat purchases of accessories matched to sink geometry. With growing countertop replacement cycles in apartments handed over in the past decade, dual-mount offerings capture a meaningful slice of renovation-driven demand.

The India Kitchen Sink and Other Related Market is Segmented by Material (Stainless Steel, Quartz, Fireclay, and More), Installation Type (Top-Mount/Drop-In, Undermount, and More), Bowl Configuration (Single Bowl, Dual Bowl, Single Bowl With Drainboard), End User (Residential, Commercial), Distribution Channel (Supermarkets/Hypermarkets, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Jaquar Group

- Hindware Home Innovation Ltd.

- CERA Sanitaryware Ltd.

- Kohler India Corp.

- Franke Faber India Pvt. Ltd.

- Nirali BG

- Carysil Ltd.

- Roca Parryware

- Hafele India (BLANCO)

- Elica PB Whirlpool Kitchen Appliances

- KAFF

- Elkay Manufacturing

- Sonet Industries

- RUHE

- Aster Kitchen Sinks

- Ozone Overseas

- Princeware International

- IKEA

- Villeroy & Boch

- LG Hausys India

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Modular-Kitchen Adoption In Urban India

- 4.2.2 Housing Completions And New Launches Supporting Sink Demand

- 4.2.3 Omnichannel Retail Expansion For Kitchen Hardware

- 4.2.4 Premiumization Toward Quartz/Granite Aesthetics

- 4.2.5 Bis-Led Quality Standardization (Isi Marking) Shifting Demand To Organized Brands

- 4.2.6 Countertop Upgrade Cycles Enabling Undermount Formats

- 4.3 Market Restraints

- 4.3.1 Unorganized Price Competition In Stainless Steel

- 4.3.2 Raw-Material Cost Volatility Pressuring Margins

- 4.3.3 Installation Skill Gaps For Undermount/Flush Formats

- 4.3.4 Compliance Cost Burden For Msmes Under QCO

- 4.4 Industry Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

- 4.6 Insights into the Latest Trends and Innovations in the Market

- 4.7 Insights on Recent Developments (New Product Launches, Strategic Initiatives, Investments, Partnerships, JVs, Expansion, M&As, etc.) in the Market

5 Market Size & Growth Forecasts

- 5.1 By Material

- 5.1.1 Stainless Steel

- 5.1.2 Quartz

- 5.1.3 Fireclay

- 5.1.4 Granite/Marble

- 5.1.5 Acrylic

- 5.1.6 Others

- 5.2 By Installation Type

- 5.2.1 Top-Mount / Drop-In

- 5.2.2 Undermount

- 5.2.3 Farmhouse / Apron-Front

- 5.2.4 Flush Mount

- 5.2.5 Dual Mount

- 5.2.6 Others

- 5.3 By Bowl Configuration

- 5.3.1 Single Bowl

- 5.3.2 Dual Bowl

- 5.3.3 Single Bowl with Drainboard

- 5.4 By End User

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.5 By Distribution Channel

- 5.5.1 Supermarkets/Hypermarkets

- 5.5.2 Exclusive Stores

- 5.5.3 Online

- 5.5.4 Other

- 5.6 By Geography

- 5.6.1 North India

- 5.6.2 South India

- 5.6.3 West India

- 5.6.4 East India

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Jaquar Group

- 6.4.2 Hindware Home Innovation Ltd.

- 6.4.3 CERA Sanitaryware Ltd.

- 6.4.4 Kohler India Corp.

- 6.4.5 Franke Faber India Pvt. Ltd.

- 6.4.6 Nirali BG

- 6.4.7 Carysil Ltd.

- 6.4.8 Roca Parryware

- 6.4.9 Hafele India (BLANCO)

- 6.4.10 Elica PB Whirlpool Kitchen Appliances

- 6.4.11 KAFF

- 6.4.12 Elkay Manufacturing

- 6.4.13 Sonet Industries

- 6.4.14 RUHE

- 6.4.15 Aster Kitchen Sinks

- 6.4.16 Ozone Overseas

- 6.4.17 Princeware International

- 6.4.18 IKEA

- 6.4.19 Villeroy & Boch

- 6.4.20 LG Hausys India

7 Market Opportunities & Future Outlook

- 7.1 Tier-2/3 Countertop-Plus-Undermount Bundles to Accelerate Premium Adoption

- 7.2 Bis QCO-Compliant Grade-304 Sinks With QR-Verifiable Isi Marking For Organized Retail And Government Procurement