PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044074

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044074

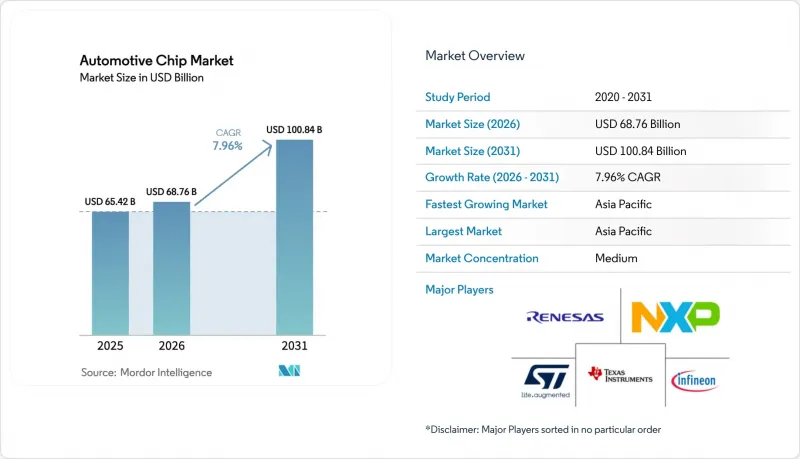

Automotive Chip - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The automotive chip market size is expected to grow from USD 65.42 billion in 2025 to USD 68.76 billion in 2026 and is forecast to reach USD 100.84 billion by 2031 at 7.96% CAGR over 2026-2031.

Software-defined vehicle programs, wide-bandgap power devices, and government incentives for domestic wafer capacity are lifting silicon demand across every vehicle domain. Microcontrollers remain indispensable for real-time safety functions, yet advanced-node system-on-chips are gaining share as zonal gateways replace dozens of legacy control units. Battery cost parity is accelerating battery-electric-vehicle (BEV) penetration, doubling the value of power discretes and sensors per car. Investment programs such as the United States CHIPS and Science Act and the European Chips Act underscore the strategic nature of automotive semiconductors. At the same time, chronic 28-45 nanometer line congestion is lengthening lead times, prompting tier-1 suppliers to pre-pay for capacity or vertically integrate power-device production.

Global Automotive Chip Market Trends and Insights

Accelerating Transition to Software-Defined and Zonal E-Architectures

Automakers are collapsing as many as 150 control units into a handful of zonal gateways that run containerized software on multi-core processors. Consolidation raises silicon content per car by up to 30% because zonal controllers require fault-tolerant CPUs, time-sensitive-networking switches, and secure power-management ICs. BMW's Neue Klasse platform will deploy centralized chips that cut wiring mass by 40% and trim integration cost. Volkswagen's co-operation with Horizon Robotics proves OEMs will share intellectual property if it shortens release cycles. Ethernet PHYs capable of 10 Gbps have emerged as critical enablers because sensor fusion demands sub-millisecond latency.

Rapid Adoption of SiC and GaN Power Devices in High-Voltage EV Platforms

Silicon-carbide and gallium-nitride components support 800-volt battery packs that add up to 350 kW fast charging without thermal drift, shrinking charge times below 15 minutes for 80% state-of-charge. onsemi's EliteSiC M3e module withstands 200 °C junction temperatures, letting automakers scale back inverter coolers by a quarter and remove USD 50 of material per vehicle. Volkswagen's five-year volume guarantee for silicon-carbide parts underlines the strategic value assigned to wide-bandgap devices. Joint gallium-nitride R&D between GlobalFoundries and onsemi on 300 mm wafers aims to halve costs by 2027.

Chronic 28-45 nm Foundry Capacity Bottlenecks Despite New Fabs

Automotive microcontrollers lean on mature 28-45 nm platforms where analog and embedded-flash blocks are field-proven. Global foundry utilization ran above 95% all through 2025, sending lead times beyond forty weeks and inflating prices by double digits. New United States and German fabs will add capacity only after 2027, and qualification means automotive volumes will be felt closer to 2030. Tier-1 suppliers have responded with take-or-pay contracts, exchanging flexibility for guaranteed wafers.

Other drivers and restraints analyzed in the detailed report include:

- OEM Push for 4 nm / 5 nm Automotive SoCs Enabling Level 3 plus ADAS

- Government-Mandated Cyber-Security and OTA Standards Raising Silicon Content

- Functional-Safety Certification Costs Burdening Mid-Tier Suppliers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Microcontrollers and microprocessors owned 36.82% of 2025 revenue, the largest slice of the automotive chip market, as engine, chassis, and body controllers continue to rely on low-latency deterministic logic. Sensors, however, represent the fastest lane, rising at an 8.01% CAGR; radar, camera, and LiDAR arrays are now mandatory in Europe, North America, and Japan for automatic emergency braking systems. The automotive chip market size tied to sensors is expected to double by 2031 as Level 3 plus functionality reaches compact cars. Power-management ICs scale in parity with BEV inverters, while discrete devices such as IGBTs or MOSFETs keep a 15-18% foothold. Memory remains a resilient niche, benefiting from growing over-the-air map downloads and infotainment caching.

OEMs rely on tight software integration between microcontrollers and security modules, ensuring ISO 26262 compliance without oversizing the silicon. Meanwhile, system suppliers are packaging radar transceivers and microprocessors inside single mold-compounds, cutting printed-circuit-board area by 30%. The convergence blurs component boundaries, drawing new competition from consumer-electronics sensor vendors. As vehicles migrate to zonal architectures, mixed-signal microcontrollers with safety-islands and gigabit Ethernet MACs are expected to replace older 16-bit units, improving functional headroom for future software features.

The 23-45 nanometer class accounted for 44.57% of 2025 shipments, the single-largest automotive chip market share because embedded-flash libraries, analog IP and ISO 26262 tool flows are mature at these geometries. Nodes at or below 10 nanometers are projected to expand at a 7.99% CAGR through 2031 as centralized compute domains need 200 TOPS of AI inference inside 50 W envelopes. This migration raises the automotive chip market size tied to advanced processes despite non-recurring engineering expenses that now top USD 500 million per design. Tier-1 suppliers accept the higher cost because a single 5 nanometer system-on-chip can replace up to ten 40 nanometer microcontrollers, trimming bill-of-materials and wiring harness length.

Foundries answer safety demands by adding redundant metallization, ECC SRAM and extra scribe-line monitors so that first-pass automotive qualification completes inside 24 months. Qualcomm and Mobileye already tape out 4 nanometer and 5 nanometer parts, winning design slots once reserved for integrated-device makers that own legacy fabs. To hedge supply risk, automakers sign capacity agreements that guarantee wafer starts but require multi-year volume commitments. Mature 90 nanometer and larger nodes remain viable for power discretes and high-voltage analog, yet the value pool is shifting to logic-dense products where software-defined features can be unlocked over the air.

Silicon delivered 75.92% of 2025 revenue because no other substrate matches its cost per transistor across microcontrollers, memory and network ICs. Gallium nitride is forecast to grow at an 8.09% CAGR as on-board chargers move to 98% efficiency and shrink passive components by Silicon-carbide already commands 12-14% of the automotive chip market size and is entrenched in 800-volt traction inverters that cut conduction losses 30% versus silicon IGBTs.

Vertical integration is changing price curves; onsemi's long-term wafer deal with Wolfspeed secures raw silicon-carbide through 2027, while its collaboration with GlobalFoundries aims to halve gallium-nitride costs on 300 mm by 2027. Cost parity with silicon for 400-volt hybrids could arrive within five years, widening adoption beyond premium BEVs. Gallium-arsenide and indium-phosphide occupy radar and LiDAR niches but together stay below 3% share. As OEMs chase efficiency gains, wide-bandgap substrates are expected to lift the overall automotive chip market share of power devices even if silicon continues to rule logic and memory.

Automotive Chip Market is Segmented by Components (Microprocessors and Microcontrollers, and More), Fabrication Node (<= 10 Nm, and More), Semiconductor Material (Silicon, and More), Propulsion Type (ICE Vehicles, and More), Vehicle Class (Passenger Cars and More), Application Domain (Powertrain and Chassis, and More), End-Market (OEM-Installed, and More), and Geography. Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific generated 40.61% of global revenue in 2025 and is anticipated to deliver the quickest 8.41% CAGR to 2031, underscored by China's requirement that one in two new cars be electric or plug-in hybrid by 2035. Domestic makers such as BYD and NIO are integrating home-grown microcontrollers to sidestep export controls, a shift that lifts regional dollar content. Japan and South Korea nurture chiplet research consortia that match best-in-class CPU tiles with local high-bandwidth memory, positioning the bloc to capture next-generation centralized compute sockets. India trails on per-vehicle silicon spend, yet a USD 9.1 billion electronics incentive could lift national assembly capacity twofold by 2028.

North America and Europe combined for roughly 46% of 2025 sales, supported by the USD 52.7 billion United States CHIPS program and EUR 43 billion European Chips Act. U.S. automakers favor domestically sourced microcontrollers to de-risk supply lines after 2021 shortages, and Intel's Arizona investment adds frontline logic capacity from 2027. Europe keeps the world's highest semiconductor spend per car, averaging USD 650, because regulatory timetables accelerate BEV and ADAS deployment. Infineon's Dresden expansion and STMicroelectronics' Catania silicon-carbide push solidify the bloc's power-device leadership.

The Middle East and Africa plus South America share the remaining 13%, yet both regions show library pockets of growth. Saudi Arabia's public-private EV investments pull demand for high-current gallium-nitride chargers, while Brazil's Rota 2030 fuel-efficiency target adds microcontroller value to flex-fuel drivetrains. Localized assembly is limited, so most chips continue to be imported from Asian foundries, keeping logistics overhead high.

- STMicroelectronics N.V.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Renesas Electronics Corp.

- Texas Instruments Inc.

- onsemi

- Analog Devices Inc.

- Toshiba Electronic Devices and Storage Corp.

- Micron Technology Inc.

- ROHM Co., Ltd.

- Robert Bosch Semiconductor

- Wolfspeed Inc.

- Semikron Danfoss

- Mitsubishi Electric Corp.

- Nexperia B.V.

- Littelfuse Inc.

- Alpha and Omega Semiconductor Ltd.

- Microchip Technology Inc.

- Qualcomm Technologies Inc.

- Samsung Electronics Co., Ltd.

- MediaTek Inc.

- Ambarella Inc.

- Mobileye Global Inc.

- GigaDevice Semiconductor

- Silicon Labs

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating Transition to Software-Defined and Zonal E-Architectures

- 4.2.2 Rapid Adoption of SiC and GaN Power Devices in High-Voltage EV Platforms

- 4.2.3 OEM Push for 4-Nm / 5-Nm Automotive SoCs Enabling L3+ ADAS

- 4.2.4 Government-Mandated Cyber-Security and OTA Standards (Unece R155/R156) Raising Silicon Content

- 4.2.5 Battery Cost Parity Accelerating BEV Penetration

- 4.2.6 Chiplet-Based Modular Designs Shortening Tier-1 Time-To-Market

- 4.3 Market Restraints

- 4.3.1 Chronic 28-45 Nm Foundry Capacity Bottlenecks Despite New Fabs

- 4.3.2 Functional-Safety (ISO 26262 / ASIL-D) Certification Costs Burdening Mid-Tier Suppliers

- 4.3.3 Limited Thermal-Management Headroom in 3-D Packaging For In-Cabin Domains

- 4.3.4 Export-Control Restrictions On EDA / IP for Chinese OEMs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Macroeconomic Impact Assessment

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Microcontrollers and Microprocessors

- 5.1.2 Power Management and Driver ICs

- 5.1.3 Discrete Power Devices (IGBT, MOSFET, SiC, GaN)

- 5.1.4 Sensors (Image, LiDAR, Radar, MEMS)

- 5.1.5 Memory (DRAM, NAND, NOR)

- 5.1.6 Connectivity and Network ICs (Ethernet, CAN-FD, LIN, FlexRay)

- 5.1.7 Other Components

- 5.2 By Fabrication Node

- 5.2.1 <= 10 nm

- 5.2.2 11 - 22 nm

- 5.2.3 23 - 45 nm

- 5.2.4 > 45 nm

- 5.3 By Semiconductor Material

- 5.3.1 Silicon (Si)

- 5.3.2 Silicon Carbide (SiC)

- 5.3.3 Gallium Nitride (GaN)

- 5.3.4 Other Semiconductor Materials

- 5.4 By Propulsion Type

- 5.4.1 Internal Combustion Engine (ICE) Vehicles

- 5.4.2 Hybrid and Plug-in Hybrid Electric Vehicles (HEV / PHEV)

- 5.4.3 Battery Electric Vehicles (BEV)

- 5.4.4 Fuel-Cell Electric Vehicles (FCEV)

- 5.5 By Vehicle Class

- 5.5.1 Passenger Cars

- 5.5.2 Light Commercial Vehicles (LCV)

- 5.5.3 Heavy Commercial Vehicles (HCV and Buses)

- 5.6 By Application Domain

- 5.6.1 Powertrain and Chassis

- 5.6.2 Advanced Driver Assistance and Safety

- 5.6.3 Body, Comfort and Convenience

- 5.6.4 Telematics, Infotainment and Connectivity

- 5.6.5 Battery Management Systems (BMS)

- 5.7 By End-Market

- 5.7.1 OEM-Installed (Factory-Fit)

- 5.7.2 Aftermarket Retro-Fit

- 5.8 By Geography

- 5.8.1 North America

- 5.8.1.1 United States

- 5.8.1.2 Canada

- 5.8.1.3 Mexico

- 5.8.2 South America

- 5.8.2.1 Brazil

- 5.8.2.2 Argentina

- 5.8.2.3 Rest of South America

- 5.8.3 Europe

- 5.8.3.1 Germany

- 5.8.3.2 France

- 5.8.3.3 United Kingdom

- 5.8.3.4 Italy

- 5.8.3.5 Spain

- 5.8.3.6 Rest of Europe

- 5.8.4 Asia Pacific

- 5.8.4.1 China

- 5.8.4.2 Japan

- 5.8.4.3 South Korea

- 5.8.4.4 India

- 5.8.4.5 Rest of Asia Pacific

- 5.8.5 Middle East

- 5.8.5.1 Saudi Arabia

- 5.8.5.2 United Arab Emirates

- 5.8.5.3 Turkey

- 5.8.5.4 Rest of Middle East

- 5.8.6 Africa

- 5.8.6.1 South Africa

- 5.8.6.2 Egypt

- 5.8.6.3 Rest of Africa

- 5.8.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 STMicroelectronics N.V.

- 6.4.2 Infineon Technologies AG

- 6.4.3 NXP Semiconductors N.V.

- 6.4.4 Renesas Electronics Corp.

- 6.4.5 Texas Instruments Inc.

- 6.4.6 onsemi

- 6.4.7 Analog Devices Inc.

- 6.4.8 Toshiba Electronic Devices and Storage Corp.

- 6.4.9 Micron Technology Inc.

- 6.4.10 ROHM Co., Ltd.

- 6.4.11 Robert Bosch Semiconductor

- 6.4.12 Wolfspeed Inc.

- 6.4.13 Semikron Danfoss

- 6.4.14 Mitsubishi Electric Corp.

- 6.4.15 Nexperia B.V.

- 6.4.16 Littelfuse Inc.

- 6.4.17 Alpha and Omega Semiconductor Ltd.

- 6.4.18 Microchip Technology Inc.

- 6.4.19 Qualcomm Technologies Inc.

- 6.4.20 Samsung Electronics Co., Ltd.

- 6.4.21 MediaTek Inc.

- 6.4.22 Ambarella Inc.

- 6.4.23 Mobileye Global Inc.

- 6.4.24 GigaDevice Semiconductor

- 6.4.25 Silicon Labs

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment