PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044081

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044081

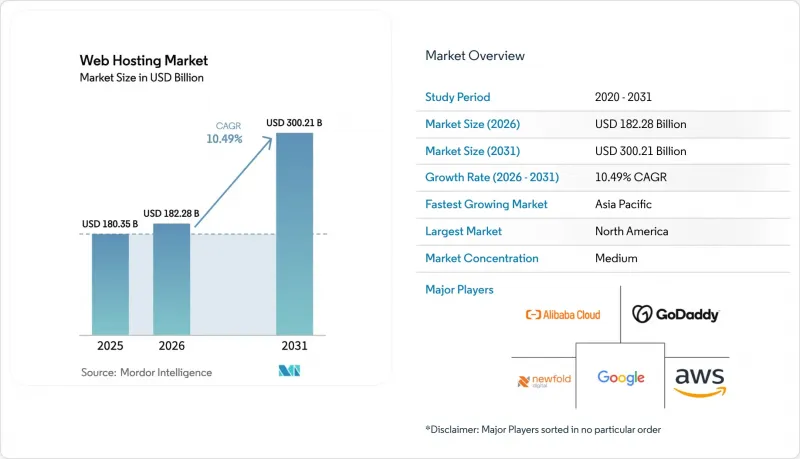

Web Hosting - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Web Hosting market size was valued at USD 180.35 billion in 2025 and estimated to grow from USD 182.28 billion in 2026 to reach USD 300.21 billion by 2031, at a CAGR of 10.49% during the forecast period (2026-2031). Ongoing adoption of generative AI workloads is steering enterprises toward GPU-ready edge infrastructure that legacy shared servers cannot support. Data-residency rules in the European Union, India, and China are accelerating hybrid deployments as firms distribute applications across on-premise, sovereign, and hyperscale clouds. Small merchants launching digital storefronts on no-code platforms are demanding 99.99% uptime, which is shifting spend toward cloud and managed WordPress tiers. Providers now compete on bundled observability tools and carbon-neutral credentials because basic uptime promises have become table stakes.

Global Web Hosting Market Trends and Insights

Explosive E-Commerce Expansion Among SMEs

No-code commerce platforms counted 4.6 million global merchants in late 2024, forcing providers to deliver elastic infrastructure that can absorb flash-sale traffic. Micro-retailers now expect bundles with PCI-DSS scans and integrated payment gateways, so value is shifting from raw server capacity to turnkey storefront enablement. Providers that embed hosting inside end-to-end commerce suites gain share among merchants lacking DevOps staff. Cross-border shopping in Southeast Asia requires edge points of presence to keep latency under 100 milliseconds, encouraging regional data-center rollouts. Monthly subscription contracts improve agility for retailers but raise churn risk for hosts, prompting investment in predictive-retention tooling.

Surging Demand for High-Availability and Low-Latency Sites

Financial regulators now classify digital-channel uptime as a compliance metric; European Banking Authority rules mandate 99.95% availability for banks. Video streaming, real-time gaming and tele-medicine rely on edge caching within 50 kilometers of users, which only hyperscalers and mature CDN operators can supply at scale. The rise of serverless computing has normalized globally distributed execution, removing the bottleneck of single-region origin servers. Latency-sensitive workloads tied to autonomous vehicles and industrial IoT require 5G-integrated edge hosting, a gap that traditional shared hosts struggle to bridge. Observability dashboards exposing latency and error rates in real time have become differentiators more than basic uptime guarantees.

Acute Shortage of Cloud-Certified Hosting Engineers

LinkedIn reported demand for cloud architecture skills outpacing supply by 2.3 times in 2025. Median salaries above USD 150,000 tempt engineers to move from hosting vendors to fintechs and SaaS unicorns. Under-staffed teams delay automation projects that customers expect, while multi-month reskilling programs carry uncertain returns. Remote work narrows traditional wage arbitrage, and credentials alone no longer guarantee competence, lengthening hiring cycles.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Migration to Hybrid and Multi-Cloud Architectures

- Carbon-Neutral Green Hosting Differentiation

- Escalating Cyber-Attacks and Data-Sovereignty Regulation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Shared hosting controlled 37.28% revenue in 2025 yet the segment is losing ground as even entry-level users migrate to cloud platforms offering auto-scaling and stronger security. Cloud hosting is forecast to grow at 10.53% and is expected to command a sizeable share of the Web Hosting market size by 2031. VPS and dedicated hosting hold niche positions among developers wanting root access and regulated industries needing single-tenant hardware. Colocation attracts firms retaining physical control while outsourcing facilities operations. Managed WordPress tiers bundle caching and staging, enabling agencies to focus on content rather than infrastructure.

The shift toward cloud accelerated in 2024-2025 as providers deprecated cPanel-based plans in favor of Kubernetes-orchestrated stacks. Multi-cloud became mainstream with 78% of enterprises running workloads across at least two vendors, reflecting strategic avoidance of lock-in. Managed WordPress players now add headless CMS features so clients can push static assets to edge networks, shrinking page-load times and extending the Web Hosting market reach into modern Jamstack workflows.

Public cloud still accounts for 45.58% of 2025 spend; however, hybrid and multi-cloud environments are projected to grow at a 10.75% CAGR through 2031 as compliance requirements drive workload distribution. This shift will increase the Web Hosting market share of hybrid solutions in regions that enforce strict data-location laws. Private cloud remains relevant where physical isolation is mandated, though hosted private services blur the line between dedicated and multitenant.

Managing hybrid estates demands synchronized identity, replicated databases, and consistent tagging. Kubernetes delivers portability, while FinOps teams optimize cost spikes that occur when always-on workloads migrate unmodified. The rise of confidential computing-Intel SGX, AMD SEV, ARM TrustZone-enables hybrid deployments where sensitive data remains encrypted even during processing, addressing regulatory concerns that previously forced on-premise deployment of workloads handling personally identifiable information.

The Web Hosting Market is Segmented by Hosting Type (Shared Hosting, Virtual Private Server Hosting, and More), Deployment Mode (Public Cloud, Private Cloud, and More), End-User Vertical (Large Enterprises, Small and Medium-Sized Enterprises, and More), Application (Public Websites, and More), Pricing Model (Subscription, and More) and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 38.63% of 2025 revenue, supported by dense hyperscale data-center clusters and early enterprise cloud adoption. Growth is moderating as the region approaches saturation, yet sovereign-cloud variants and AI-specific GPU farms sustain investment. outh America's hosting demand concentrates in Brazil and Argentina, where inflation volatility and currency devaluation force providers to denominate contracts in U.S. dollars and implement dynamic pricing that adjusts monthly based on exchange-rate fluctuations.

Asia-Pacific is projected to expand at a 10.93% CAGR, underpinned by the proliferation of digital payments in India, where UPI volumes crossed 100 billion transactions in 2024. Indonesian and Vietnamese fintechs deploy low-latency nodes in Jakarta and Ho Chi Minh City to comply with national regulations. Edge expansions by providers such as Telehouse added 15 data centers in 2024, cutting round-trip latency from 180 milliseconds to under 50 milliseconds in key metros.

Europe balances GDPR nuances with the need for scale. Regional companies such as OVHcloud and Hetzner promote in-region data storage, while AWS responded in 2024 with an isolated European Sovereign Cloud. Middle East and Africa represent nascent markets where mobile-first internet adoption-smartphone penetration exceeds 80% in UAE and Saudi Arabia-drives demand for hosting optimized for cellular networks with high latency and intermittent connectivity.

List of Companies Covered in this Report:

- Amazon Web Services

- Google LLC

- Microsoft Corporation

- GoDaddy Inc.

- Newfold Digital

- Alibaba Cloud

- Tencent Cloud

- Liquid Web LLC

- DigitalOcean

- OVH Groupe SA

- Hetzner Online GmbH

- WP Engine

- 1and1 IONOS

- Hostinger International Ltd.

- SiteGround Hosting Ltd.

- A2 Hosting LLC

- Kinsta Inc.

- DreamHost LLC

- GreenGeeks LLC

- InMotion Hosting Inc.

- The Constant Company LLC

- Namecheap Inc.

- HostGator LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Drivers

- 4.1.1 Explosive E-Commerce Expansion Among SMEs

- 4.1.2 Surging Demand For High-Availability and Low-Latency Sites

- 4.1.3 Rapid Migration To Hybrid/Multi-Cloud Architectures

- 4.1.4 Carbon-Neutral Green Hosting Differentiation

- 4.1.5 Gen-AI-Ready Edge and GPU Server Demand Surge

- 4.2 Market Restraints

- 4.2.1 Acute Shortage of Cloud-Certified Hosting Engineers

- 4.2.2 Escalating Cyber-Attacks and Data-Sovereignty Regulation

- 4.2.3 Margin Pressure From Race-To-Zero Pricing

- 4.2.4 Energy-Price Volatility And Power-CAPEX Inflation

- 4.3 Value Chain Analysis

- 4.4 Regulatory Landscape

- 4.5 Technological Outlook

- 4.6 Porter's Five Forces

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Consumers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Sustainability Positioning and Green Hosting Initiatives

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Hosting Type

- 5.1.1 Shared Hosting

- 5.1.2 Virtual Private Server (VPS) Hosting

- 5.1.3 Dedicated Hosting

- 5.1.4 Cloud Hosting

- 5.1.5 Colocation Hosting

- 5.1.6 Managed WordPress Hosting

- 5.1.7 Reseller Hosting

- 5.1.8 Other Hosting Types

- 5.2 By Deployment Mode

- 5.2.1 Public Cloud

- 5.2.2 Private Cloud

- 5.2.3 Hybrid/Multi-Cloud

- 5.3 By End-user Vertical

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-sized Enterprises (SMEs)

- 5.3.3 Individual Bloggers/Creators

- 5.3.4 Software Developers and SaaS Start-ups

- 5.4 By Application

- 5.4.1 Public Websites

- 5.4.2 E-commerce Stores

- 5.4.3 Web Applications

- 5.4.4 Mobile Applications and APIs

- 5.4.5 SaaS/PaaS Platforms

- 5.4.6 Other Applications

- 5.5 By Pricing Model

- 5.5.1 Subscription (Fixed-Term)

- 5.5.2 Metered/Pay-as-you-go

- 5.5.3 Tiered (Usage-Bracket)

- 5.5.4 Freemium and Ad-Supported

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 United Arab Emirates

- 5.6.5.2 Saudi Arabia

- 5.6.5.3 South Africa

- 5.6.5.4 Nigeria

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials as available, Strategic Information, Market Rank / Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Amazon Web Services

- 6.4.2 Google LLC

- 6.4.3 Microsoft Corporation

- 6.4.4 GoDaddy Inc.

- 6.4.5 Newfold Digital

- 6.4.6 Alibaba Cloud

- 6.4.7 Tencent Cloud

- 6.4.8 Liquid Web LLC

- 6.4.9 DigitalOcean

- 6.4.10 OVH Groupe SA

- 6.4.11 Hetzner Online GmbH

- 6.4.12 WP Engine

- 6.4.13 1and1 IONOS

- 6.4.14 Hostinger International Ltd.

- 6.4.15 SiteGround Hosting Ltd.

- 6.4.16 A2 Hosting LLC

- 6.4.17 Kinsta Inc.

- 6.4.18 DreamHost LLC

- 6.4.19 GreenGeeks LLC

- 6.4.20 InMotion Hosting Inc.

- 6.4.21 The Constant Company LLC

- 6.4.22 Namecheap Inc.

- 6.4.23 HostGator LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment