PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044085

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044085

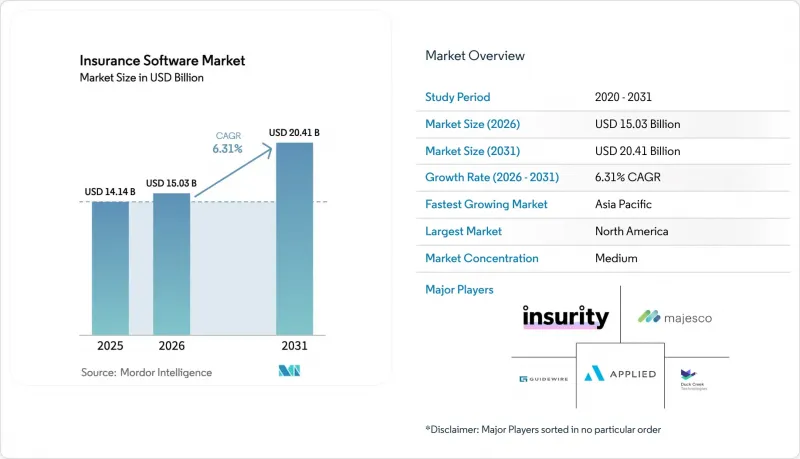

Insurance Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Insurance Software Market size was valued at USD 14.14 billion in 2025 and is estimated to grow from USD 15.03 billion in 2026 to reach USD 20.41 billion by 2031, at a CAGR of 6.31% during the forecast period (2026-2031).

Growth is propelled by insurers shifting from incremental IT upgrades to full-scale platform renewal that supports real-time pricing, embedded distribution, and continuous compliance reporting. Cloud-native deployment already accounts for 65.7% of current revenue and, at a 10.5% CAGR, will widen its lead as late adopters migrate from aging mainframes. Property and casualty (PandC) solutions dominate 2024 spending with 48.8% share, but health and accident systems grow the fastest at 12.3% CAGR on post-pandemic engagement mandates. Private equity has poured more than USD 6 billion into vendors since 2024, accelerating feature delivery cycles and intensifying price competition. Regionally, North America supplies the largest budgets, yet Asia-Pacific's double-digit expansion highlights a greenfield advantage for API-first, mobile-led deployments.

Global Insurance Software Market Trends and Insights

Cloud-native platform adoption accelerates digital transformation

Insurers now view migration to the cloud as a competitive requirement, not a cost exercise. Lincoln Financial Group completed a two-year cloud switch that cut software licensing costs and shortened cycle times by 20-30% while creating flexible DevOps pipelines. Guidewire's cloud suite already supports more than 570 insurers worldwide and lifted subscription revenue 35% in Q2 2025. Cloud architectures enable real-time data ingestion essential for dynamic pricing and embedded distribution, as seen in Duck Creek's Policy solution that delivers bi-weekly updates through low-code tools. Variable infrastructure economics arising from these deployments free capital for rapid product iterations that legacy mainframes cannot match.

Rising insurer focus on AI-driven underwriting and claims automation

Artificial intelligence has advanced from pilot to production in underwriting, fraud detection, and claims adjudication. Guidewire's Las Lenas release embeds machine-learning models that cut application review from days to minutes. LTIMindtree's AI-Smart Underwriter on ServiceNow speeds risk assessment while halving administrative loads. Salesforce now offers pre-built AI components for policy administration that boost straight-through processing rates for mid-tier carriers. Sapiens' UnderwritingPro v14 combines predictive analytics with agent portals, trimming processing costs by up to 40% and increasing customer satisfaction.

Legacy core migrations remain complex and costly

Many carriers still operate 20-year-old mainframes that lack APIs and present data-conversion risks. Life-policy data fields number into the thousands, making clean migrations prone to errors and extended testing. Equisoft notes that fear of disruption keeps some life insurers on legacy policy systems even as competitors gain agility with rules-based solutions. Balancing run-the-business continuity with phased replacement schedules inflates budgets and slows time-to-value.

Other drivers and restraints analyzed in the detailed report include:

- Shift to usage-based and embedded insurance products

- Regulatory pushes for real-time compliance and reporting APIs

- Cyber-security and data-sovereignty regulations tighten

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployment captured 65.10% of 2025 revenue, equal to the largest slice of the insurance software market. At the same time, it is forecast to post a 10.26% CAGR, making it both the incumbent and the growth engine. The insurance software market size advantage arises because elastic infrastructure supports real-time rating, low-code configuration, and bi-weekly feature drops that on-premises stacks cannot match. Subscription models convert fixed CapEx into variable OpEx, freeing budgets for innovation. Guidewire Cloud reported 35% subscription growth on the back of 570 live insurers, while Duck Creek's Active Delivery shows how automatic updates keep carriers evergreen. On-premises installations persist for regulated lines such as workers' compensation where data-sovereignty rules still hinder cloud adoption, yet their share continues to erode as hyperscalers achieve compliance certifications across additional jurisdictions.

Cloud migrations also underpin embedded insurance rollouts, because retailers and mobility platforms demand API-first connections that can be spun up in weeks. Carriers running cloud cores report launch cycles that are one-quarter of those on legacy stacks, enabling them to test niche micro-products without sunk-cost risk. Moreover, vendors bundle cloud hosting with DevSecOps toolchains and continuous penetration testing, partially offsetting new cyber-compliance burdens. As a result, enterprise architects now rank portability and event-stream processing among top vendor-selection criteria, re-inforcing the flywheel for further cloud adoption in the insurance software market.

Insurance Software Market is Segmented by Deployment (Cloud and On-Premise), Insurance Type (Life Insurance, Accident and Health Insurance, and More), End-User (Insurance Companies, Brokers and Agencies) and by Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America remains the largest regional buyer, accounting for 38.35% of 2025 global revenue. Carriers funnel budgets into cloud migration programs that unwind decades-old mainframes, comply with the NAIC Insurance Data Security Model Law, and satisfy New York's 23 NYCRR 500 rules on multi-factor authentication and 72-hour breach notifications. Vendor selection favors established suites with proven integration accelerators, as illustrated by Guidewire's USD 918 million annual recurring revenue in 2024.

Asia-Pacific delivers the fastest growth, clocking a 10.45% CAGR through 2031. Rising disposable incomes and favorable regulatory sandboxes allow carriers to launch API-centric products that bundle coverage with e-commerce, mobility, or wellness apps. When Chubb Studio integrated with a Southeast Asian super-app, it gained exposure to tens of millions of new users. China's return to premium expansion and India's 9% life-insurance growth guide vendors to localise interfaces and comply with on-shore data-residency rules.

Europe's outlook is shaped by DORA, which formalizes ICT risk-management obligations and continuous testing from 2025. Carriers invest in observability, third-party vendor assessment, and centralized incident playbooks. Meanwhile, Latin America and Africa accelerate from a low base as regulators introduce digital-policy acceptance and e-signature frameworks that remove paper-based bottlenecks. Carriers in these regions often select cloud systems bundled with managed services to offset skill shortages, illustrating the diverse yet complementary growth vectors within the insurance software market.

- Guidewire Software

- Duck Creek Technologies

- Applied Systems

- Insurity

- Majesco

- Salesforce

- Microsoft

- Oracle

- SAP

- Sapiens International

- Vertafore

- FINEOS

- EIS Group

- BriteCore

- Socotra

- OneShield Software

- EXL Service

- CGI Inc.

- Shift Technology

- TIA Technology

- ZhongAn Technology

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Cloud-native platform adoption accelerates digital transformation

- 4.2.2 Rising insurer focus on AI-driven underwriting and claims automation

- 4.2.3 Shift to usage-based and embedded insurance products

- 4.2.4 Regulatory pushes for real-time compliance and reporting APIs

- 4.2.5 PE-backed roll-ups scaling best-of-breed core systems

- 4.2.6 Climate-risk analytics unlocking new software spend

- 4.3 Market Restraints

- 4.3.1 Legacy core migrations remain complex and costly

- 4.3.2 Cyber-security and data-sovereignty regulations tighten

- 4.3.3 Shortage of insurtech-skilled talent inflates project costs

- 4.3.4 Insurer MandA delays IT refresh decisions

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Assessment of Impact of Macroeconomic Trends

- 4.9 Investment Analysis

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 Cloud

- 5.1.2 On-Premises

- 5.2 By Insurance Type

- 5.2.1 Life Insurance

- 5.2.2 Accident and Health Insurance

- 5.2.3 Property and Casualty Insurance

- 5.2.4 Other Types

- 5.3 By End User

- 5.3.1 Insurance Companies

- 5.3.2 Brokers

- 5.3.3 Agencies

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 India

- 5.4.4.4 South Korea

- 5.4.4.5 ASEAN

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Egypt

- 5.4.5.2.4 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Guidewire Software

- 6.4.2 Duck Creek Technologies

- 6.4.3 Applied Systems

- 6.4.4 Insurity

- 6.4.5 Majesco

- 6.4.6 Salesforce

- 6.4.7 Microsoft

- 6.4.8 Oracle

- 6.4.9 SAP

- 6.4.10 Sapiens International

- 6.4.11 Vertafore

- 6.4.12 FINEOS

- 6.4.13 EIS Group

- 6.4.14 BriteCore

- 6.4.15 Socotra

- 6.4.16 OneShield Software

- 6.4.17 EXL Service

- 6.4.18 CGI Inc.

- 6.4.19 Shift Technology

- 6.4.20 TIA Technology

- 6.4.21 ZhongAn Technology

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment