PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044107

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044107

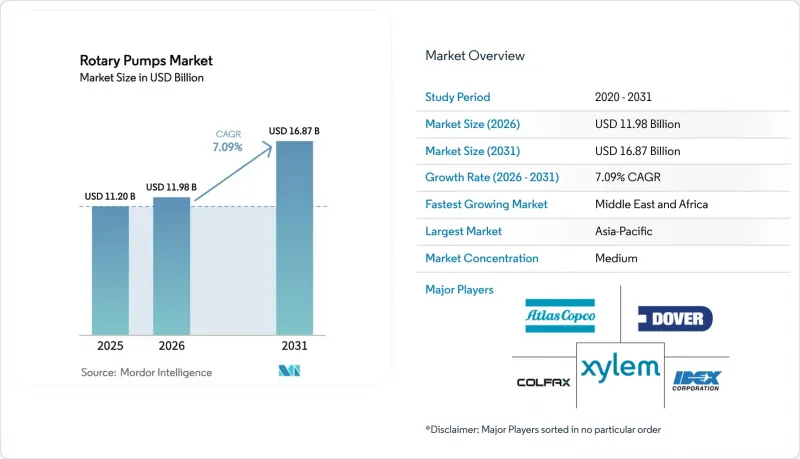

Rotary Pumps - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The rotary pumps market size is projected to expand from USD 11.20 billion in 2025 and USD 11.98 billion in 2026 to USD 16.87 billion by 2031, registering a 7.09% CAGR between 2026 and 2031.

Structural demand is strengthening as refineries retrofit high-viscosity service lines, Asian petrochemical complexes commission API-676 gear and screw models, and North American food processors replace legacy sanitary centrifugals to meet tightening hygiene rules. Offshore operators are standardizing twin-screw units on deep-water FPSOs to avoid pulsation-induced fatigue, while United States municipalities, armed with Infrastructure Investment and Jobs Act grants, are specifying rotary lobe and progressive-cavity pumps for sludge, digester, and influent duties. Rising adoption of digital-twin platforms that monitor vibration, temperature, and seal-health data is converting transactional spare-part sales into long-term monitoring contracts, handing an advantage to incumbents with large installed bases. Counterfeit aftermarket parts and stricter volatile-organic-compound (VOC) rules in Europe complicate total-cost-of-ownership calculations, yet API-676 certification and sensor-enabled reliability remain decisive purchase criteria across end markets.

Global Rotary Pumps Market Trends and Insights

Energy-Sector Brownfield Upgrades Driving High-Viscosity Fluid Handling Demand

Refiners across North America and the Middle East are redirecting capital from greenfield projects to debottlenecking programs that must accommodate heavier crude blends and renewable feedstocks, prompting large-scale replacement of centrifugal pumps with external-gear and twin-screw models certified for viscosities above 5,000 cP. Equinor's USD 1 billion modernization at the Mongstad refinery integrates electrified rotary pumps that are expected to curb Scope 2 emissions by 30%. The Oil and Gas Climate Initiative projects that member companies will require 2,500 additional rotary units by 2028, anchoring multi-year demand visibility. Strict API-676 seal, vibration, and casing limits restrict the qualified supplier pool, enabling compliant vendors to secure premium pricing. Together these factors ensure that even when overall refinery construction slows, brownfield replacement volumes for high-viscosity pumps will keep expanding.

Petrochemical Capacity Additions in China and India Requiring API-676 Compliant Rotary Pumps

China's record 14.81 million bpd throughput in 2025, supported by Rongsheng's 40 million t/yr Zhejiang complex, is steadily shifting long-term orders toward high-pressure gear and screw pumps that now include locally engineered 70 MPa ratings to reduce import dependence. India's 1.5 million bpd refinery expansion plan through 2030 has led Reliance and Indian Oil to pre-qualify twin-screw suppliers for polymer-grade propylene and butadiene transfer duties. The International Energy Agency forecasts petrochemical feedstock demand to rise 6.2% annually through 2030, reinforcing the pull for API-676 equipment across resin and elastomer plants. Engineering, procurement, and construction contractors are mandating dual-pressurized seals with leak-detection ports to satisfy tighter environmental rules, bolstering supplier differentiation. Consequently, Asian petrochemical mega-projects will remain the single largest booking source for compliant rotary pumps over the forecast horizon.

Availability of Low-Cost Counterfeit Spares from Unorganized Asian Vendors

The European Union Intellectual Property Office notes that counterfeit rotors, seals, and bearings now represent 12% of industrial parts seized at EU borders, with most originating in China and India. Substandard elastomers degrade quickly in high-temperature or chemically aggressive environments, leading to premature leaks and costly downtime. E-commerce platforms make uncertified parts easy to procure, overwhelming maintenance teams that lack strict vendor-qualification protocols. The Hydraulic Institute has introduced QR-code and blockchain authentication frameworks, but adoption outside North America remains limited, allowing gray-market channels to persist. Until plant operators universally implement verification systems, counterfeit spares will continue to erode legitimate aftermarket margins and damage OEM brand equity.

Other drivers and restraints analyzed in the detailed report include:

- Recovery of Offshore FPSO Construction in Brazil Boosting Twin-Screw Pump Orders

- Food-Grade Gear Pump Uptake Amid U.S. FSMA Clean-in-Place Mandates

- Strict VOC-Emission Rules Limiting Mechanical-Seal Selection for Rotary Pumps in EU

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

External-gear pumps commanded 32.47% of share in 2025 because their simple, rugged architecture tolerates sand-laden crude and high suction lift in upstream fields. Their share is expected to slide as twin-screw models, projected to grow 8.43% through 2031, solve pulsation and gas-entrainment issues common on FPSO topsides and polymer reactors. Seatrium's P-84 and P-85 FPSO contracts and NETZSCH's 1,400 m3/h XXLB-F launch confirm that operators and suppliers are scaling two-screw technology for mega-project service, reinforcing the shift toward performance-differentiated solutions. Internal-gear pumps, meanwhile, are securing hygienic niches in beverage, chocolate, and personal-care fluids where low shear is critical, while vane and triple-screw types remain limited to mobile hydraulics and high-pressure marine lubrication. Roto Pumps' modular P-Range shows that innovation continues in mature external-gear designs, but total cost-of-ownership metrics increasingly favor screw technologies that promise longer seal life and lower vibration.

Customer specifications now bundle API-676 compliance with digital-readiness, forcing vendors to embed sensor ports or factory-installed vibration probes even on standard frames. As energy-transition fuels such as bio-oils and renewable diesel flood pipelines, fluid viscosities vary more widely, amplifying the value of screw pumps that can adjust speed without losing volumetric efficiency. Consequently, competitive dynamics in the rotary pumps market should tilt toward suppliers capable of mass-producing robust, digitally enabled twin-screw platforms while retaining niche margins in external-gear replacement business.

Oil and gas accounted for 28.42% of the share in 2025 through broader upstream, midstream, and downstream deployment, yet the segment's forward momentum trails the headline market CAGR as decarbonization targets cap fossil-fuel capital spending. Food and beverage processors, by contrast, are forecast to expand pump purchases at a 9.11% CAGR through 2031 because FSMA mandates and EU Farm-to-Fork incentives compel systematic upgrades to sanitary equipment. Integrated sensors in new hygienic lines generate actionable data on cleaning cycles and process temperature, reducing compliance risk and explaining the segment's robust adoption curve.

Chemical and petrochemical plants still generate large-ticket orders for high-pressure, high-temperature gear and screw pumps, especially at Chinese and Indian complexes processing polymer-grade monomers. Water, wastewater, and power create steady base demand, with Infrastructure Investment and Jobs Act allocations lining up progressive-cavity and lobe pump replacements in aging U.S. facilities. Mining, pulp, and paper add volatility-resilient demand for abrasion-resistant rotary designs, ensuring that supplier revenue streams become more diversified and less sensitive to oil-price cycles over the forecast horizon.

The Rotary Pumps Market Report is Segmented by Type (External-Gear, Internal-Gear, and More), End-User Industry (Oil and Gas, Power Generation, Chemicals and Petrochemicals, Food and Beverage, and More), Discharge Pressure (Up To 10 Bar, 10-25 Bar, 25-100 Bar, and Above 100 Bar), Pump Capacity (Up To 50 M3/H, 51-150 M3/H, 151-500 M3/H, and Above 500 M3/H), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific held 40.19% of share in 2025, buoyed by record Chinese refinery runs and India's import-substitution policy that channels orders to domestic API-676 suppliers. The Middle East and Africa are forecast to post a 9.08% CAGR as Saudi Aramco's Jazan expansion, the UAE's Ruwais complex, and Nigeria's 650,000 bpd Dangote refinery reach full capacity, each specifying high-flow, high-pressure gear and screw models. North America benefits from brownfield hydroprocessing upgrades and USD 50 billion in federal water-infrastructure spending that subsidizes municipal pump replacements, anchoring a dependable order pipeline.

Europe combines hygienic pump innovation with VOC-induced retrofit headwinds, producing steady but not spectacular growth as operators weigh the cost of double seals against sealless options. South America's trajectory leans heavily on Brazil's FPSO build program and Chilean copper-concentrate pipelines, ensuring a long though narrower backlog for abrasion-resistant and low-pulsation units. Overall, geographic diversification tempers macro volatility and supports a balanced global growth outlook for rotary pump suppliers.

Asia's developed economies are also pivoting toward lower-carbon fuels, with Japan repurposing one-third of its idled refining capacity for sustainable-aviation-fuel production, a shift that is already generating new tenders for duplex-steel twin-screw pumps rated above 100 bar. Australia's LNG liquefaction operators are meanwhile installing rotary lobe and progressive-cavity units on water-treatment modules to comply with tightened discharge permits, expanding aftermarket service revenue for vendors that maintain Perth or Darwin service depots. South Korea is upgrading chemical recycling lines at Ulsan and Yeosu to process mixed plastic waste, specifying API-676 gear pumps fitted with magnetic couplings to eliminate fugitive VOC emissions and meet Industrial Emissions Directive-equivalent local standards. Finally, Singapore's Jurong Island is adding bio-cracker capacity that calls for above-500 m3/h screw pumps capable of handling fatty-acid feedstocks with viscosities above 1,000 cP, reinforcing Southeast Asia's role as a premium market for high-performance rotary equipment.

- Dover Corporation (Pump Solutions Group)

- IDEX Corporation (Viking Pump)

- Colfax Corporation (IMO / Allweiler)

- SPX Flow Inc.

- Xylem Inc.

- Atlas Copco AB

- Gardner Denver Holdings Inc.

- Pfeiffer Vacuum Technology AG

- ULVAC Inc.

- Busch SE

- Flowserve Corporation

- KSB SE and Co. KGaA

- Netzsch Pumpen and Systeme GmbH

- Alfa Laval AB

- PCM SA

- Seepex GmbH

- ITT Inc.

- Sulzer Ltd.

- DESMI A/S

- Kirloskar Brothers Ltd.

- Verder Group

- Roto Pumps Ltd.

- Tuthill Corporation

- Blackmer (PSG brand)

- Vogelsang GmbH and Co. KG

- Roper Technologies Inc. (Roper Pump Company)

- Leistritz AG

- Eureka Pumps AS

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Energy-Sector Brown-Field Upgrades Driving High-Viscosity Fluid Handling Demand

- 4.2.2 Petrochemical Capacity Additions in China and India Requiring API-676 Compliant Rotary Pumps

- 4.2.3 Recovery of Offshore FPSO Construction in Brazil Boosting Twin-Screw Pump Orders

- 4.2.4 Food-Grade Gear Pump Uptake Amid U.S. FSMA Clean-In-Place Mandates

- 4.2.5 Rising European Craft-Brewery Installations Favoring Low-Shear Lobe Pumps

- 4.2.6 AI-Enabled Predictive Maintenance Models Increasing Aftermarket Revenues

- 4.3 Market Restraints

- 4.3.1 Availability of Low-Cost Counterfeit Spares from Unorganized Asian Vendors

- 4.3.2 Strict VOC-Emission Rules Limiting Mechanical-Seal Selection for Rotary Pumps in EU

- 4.3.3 High Upfront Cost Versus Centrifugal Alternatives in Municipal Water Plants

- 4.3.4 Skilled-Labor Shortage for Screw-Pump Maintenance in Sub-Saharan Africa

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Type

- 5.1.1 External-Gear

- 5.1.2 Internal-Gear

- 5.1.3 Twin-Screw

- 5.1.4 Triple-Screw

- 5.1.5 Vane

- 5.2 By End-user Industry

- 5.2.1 Oil and Gas

- 5.2.2 Power Generation

- 5.2.3 Chemicals and Petrochemicals

- 5.2.4 Food and Beverage

- 5.2.5 Water and Waste-water

- 5.2.6 Other End-user Industries

- 5.3 By Discharge Pressure

- 5.3.1 Up to 10 bar

- 5.3.2 10-25 bar

- 5.3.3 25-100 bar

- 5.3.4 Above 100 bar

- 5.4 By Pump Capacity (m3/h)

- 5.4.1 Up to 50

- 5.4.2 51-150

- 5.4.3 151-500

- 5.4.4 Above 500

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Chile

- 5.5.2.4 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 Saudi Arabia

- 5.5.5.1.2 United Arab Emirates

- 5.5.5.1.3 Turkey

- 5.5.5.1.4 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Nigeria

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, and Recent Developments)

- 6.4.1 Dover Corporation (Pump Solutions Group)

- 6.4.2 IDEX Corporation (Viking Pump)

- 6.4.3 Colfax Corporation (IMO / Allweiler)

- 6.4.4 SPX Flow Inc.

- 6.4.5 Xylem Inc.

- 6.4.6 Atlas Copco AB

- 6.4.7 Gardner Denver Holdings Inc.

- 6.4.8 Pfeiffer Vacuum Technology AG

- 6.4.9 ULVAC Inc.

- 6.4.10 Busch SE

- 6.4.11 Flowserve Corporation

- 6.4.12 KSB SE and Co. KGaA

- 6.4.13 Netzsch Pumpen and Systeme GmbH

- 6.4.14 Alfa Laval AB

- 6.4.15 PCM SA

- 6.4.16 Seepex GmbH

- 6.4.17 ITT Inc.

- 6.4.18 Sulzer Ltd.

- 6.4.19 DESMI A/S

- 6.4.20 Kirloskar Brothers Ltd.

- 6.4.21 Verder Group

- 6.4.22 Roto Pumps Ltd.

- 6.4.23 Tuthill Corporation

- 6.4.24 Blackmer (PSG brand)

- 6.4.25 Vogelsang GmbH and Co. KG

- 6.4.26 Roper Technologies Inc. (Roper Pump Company)

- 6.4.27 Leistritz AG

- 6.4.28 Eureka Pumps AS

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment