PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044128

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044128

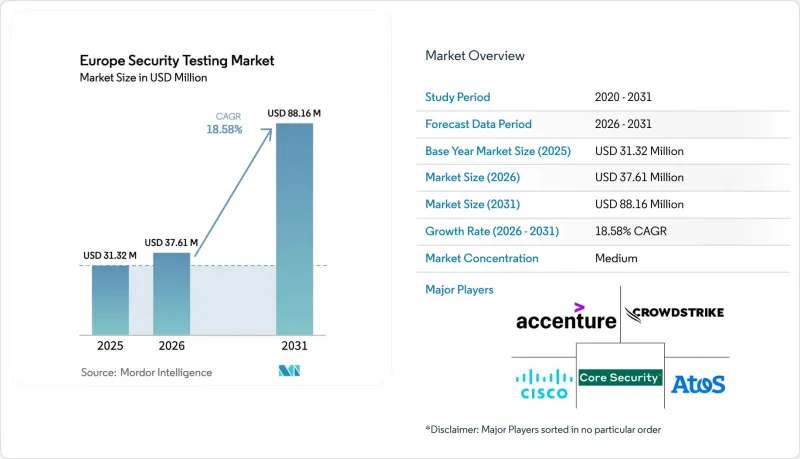

Europe Security Testing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Europe Security Testing Market size is projected to expand from USD 31.32 million in 2025 and USD 37.61 million in 2026 to USD 88.16 million by 2031, registering a CAGR of 18.58% between 2026 to 2031.

Robust growth is underpinned by synchronized regulatory deadlines, a sharp rise in critical-infrastructure breaches, and the rapid spread of cloud-first development models. Germany's Mittelstand factories, France's public-sector digital-sovereignty programs, and the United Kingdom's financial-services resilience agenda are shaping procurement priorities, while hybrid deployment architectures are becoming the default path to balance data-sovereignty needs with on-demand scalability. Vendor competition is intensifying as global consultancies, pure-play application security platforms, and local champions vie to offer bundled managed-testing subscriptions that address a widening skills gap. At the same time, artificial-intelligence analytics that suppress false positives are beginning to dictate buying decisions, especially among organizations fatigued by alert overload.

Europe Security Testing Market Trends and Insights

Heightened Post-2023 Critical-Infrastructure Cyber-Attacks in Power and Rail

A 68% jump in serious incidents against European power and transport networks between 2024-2025 has moved continuous testing from a best practice to a board mandate. The 2024 ransomware disruption at Deutsche Bahn and the late-2024 DDoS attacks on Polish utilities exposed protocol weaknesses in operational-technology (OT) environments once thought to be insulated. Regulators now fine entities up to 2% of global turnover for failing to run quarterly vulnerability scans, prompting rail and grid operators to pre-book multi-year managed-testing contracts. Vendors able to decode Modbus, DNP3, and IEC 61850 traffic are winning deals because they offer actionable insights instead of generic advisories. In the short term, the scramble for OT specialists is tightening consulting supply, lifting project day rates and encouraging tool makers to embed industrial-protocol libraries directly into automated scanners.

Accelerated EU NIS2 and DORA Compliance Deadlines

NIS2 expanded the pool of regulated organizations from roughly 20,000 to 160,000 and DORA added heavy, scenario-based penetration-test obligations for 22,000 financial entities. Together, the statutes have created a steady pipeline of first-time buyers that previously relied on self-attestation. Early-enforcing states such as Germany and France already ask for test reports within 72 hours of critical findings, pushing enterprises toward SaaS platforms that can generate evidence artifacts on demand. Cloud providers and MSPs serving banks must also undergo audits, cascading compliance pressure through the supply chain. Over the medium term, this legal architecture institutionalizes security testing as a recurring operating expense, smoothing revenue visibility for vendors and raising the baseline demand floor across the continent.

Shortage of CREST-Certified Security Testers

Europe needed at least 6,000 CREST-accredited professionals in 2025 but had only 4,200 on the rolls. Daily rates for senior testers rose 40% in two years, lengthening scheduling queues to as long as three months for regulated penetration tests. Some buyers have downgraded credential requirements to keep projects on track, eroding the standardization regulators intended. Tool vendors are exploiting the gap by touting continuous automated scanning as an interim substitute, but supervisors have yet to confirm whether such automation satisfies DORA's threat-led scope. In the near term, the talent drought will remain a drag on Europe security testing market growth and will amplify wage inflation, especially in Germany and the Netherlands.

Other drivers and restraints analyzed in the detailed report include:

- Shift-Left DevSecOps Adoption in Software Supply-Chain

- Industrial IoT Penetration in German Mittelstand Factories

- Budget Freeze across EU-27 SMEs amid 2024 Credit-Tightening

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud platforms generated 48.23% of 2025 revenue, reflecting the appeal of pay-per-scan economics and zero appliance overhead in the Europe security testing market size. Demand stayed strong into 2026 as enterprises prioritized rapid scale-up for quarterly vulnerability sweeps. Hybrid approaches, however, show the highest 18.73% CAGR because regulated banks and hospitals keep sensitive data on-premise, routing only metadata to SaaS consoles for centralized policy enforcement. The arrangement satisfies national data-sovereignty statutes without sacrificing elastic compute, giving vendors with local datacenter footprints an edge.

On-premise appliances now serve a shrinking niche of defense contractors and air-gapped OT plants, but they remain non-negotiable where external connections are prohibited. Vendors are responding with containerized scanners shipped as virtual images that slot into existing private-cloud stacks, creating a stepping stone toward future hybrid conversions. Over the forecast window, improvements in confidential-computing chipsets and EU-level certification schemes are likely to narrow the perceived risk gap, nudging late adopters toward at least partial cloud orchestration.

Application-level techniques represented 42.73% of 2025 turnover, confirming that exploitable code paths, not perimeter firewalls, now define enterprise exposure across the Europe security testing market. Within this bucket, cloud application security testing is accelerating at 19.26% CAGR because microservices, serverless functions, and ephemeral containers cannot be scanned by legacy network probes. Static analysis, dynamic analysis, and software composition analysis are routinely chained together in CI/CD pipelines, pushing scan counts into the thousands each month for large DevOps shops.

Mobile and web application testing remains relevant, particularly among digital-banking and e-commerce providers bound by PSD2 secure-communication clauses. Yet the deepest innovation capital is migrating to cloud-native runtime visibility, where interactive testing tools instrument code and correlate data-flow evidence to slash false positives. Vendor differentiation now stems from how seamlessly platforms slot into GitHub Actions, GitLab CI, and Bitbucket workflows, and from their ability to flag vulnerable open-source libraries before pull requests are merged.

The Europe Security Testing Market Report is Segmented by Deployment (On-Premise, Cloud, and Hybrid), Type (Network Security Testing Including VPN Testing, and Application Security Testing Including Mobile), Testing Type (SAST, DAST, IAST, and RASP), End-User Industry (Government, BFSI, and More), Testing Tool (Web Application Testing Tool, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- Accenture plc

- Atos SE

- Cisco Systems, Inc.

- Core Security, LLC

- CrowdStrike Holdings, Inc.

- Fortinet, Inc.

- Hewlett Packard Enterprise Company

- IBM Corporation

- Tenable Holdings, Inc.

- Micro Focus International plc

- Snyk Limited

- HackerOne, Inc.

- Offensive Security, LLC

- Orange Cyberdefense SAS

- Paladion Networks Private Limited

- PricewaterhouseCoopers International Limited

- Qualys, Inc.

- Securonix, Inc.

- Synopsys, Inc.

- Veracode, Inc.

- Rapid7, Inc.

- Checkmarx Ltd.

- NCC Group plc

- TUV Rheinland AG

- Bureau Veritas S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Heightened Post-2023 Critical-Infrastructure Cyber-Attacks in Power and Rail

- 4.2.2 Accelerated EU NIS2 and DORA Compliance Deadlines

- 4.2.3 Shift-Left DevSecOps Adoption in Software Supply-Chain

- 4.2.4 Industrial IoT Penetration in German Mittelstand Factories

- 4.2.5 Mandatory Penetration-Testing Clauses in European Public-Sector Tenders

- 4.2.6 Quantum-Resistant Crypto Migration Pilots

- 4.3 Market Restraints

- 4.3.1 Shortage of CREST-Certified Security Testers

- 4.3.2 Budget Freeze across EU-27 SMEs amid 2024 Credit-Tightening

- 4.3.3 Fragmented Data-Sovereignty Rules Slowing Cloud-Based Testing

- 4.3.4 False-Positive Fatigue Reducing Test Frequency

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitute Products

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment

- 5.1.1 On-Premise

- 5.1.2 Cloud

- 5.1.3 Hybrid

- 5.2 By Type

- 5.2.1 Network Security Testing

- 5.2.1.1 VPN Testing

- 5.2.1.2 Firewall Testing

- 5.2.1.3 Other Service Types

- 5.2.2 Application Security Testing

- 5.2.2.1 Mobile Application Security Testing

- 5.2.2.2 Web Application Security Testing

- 5.2.2.3 Cloud Application Security Testing

- 5.2.2.4 Enterprise Application Security Testing

- 5.2.1 Network Security Testing

- 5.3 By Testing Type

- 5.3.1 SAST

- 5.3.2 DAST

- 5.3.3 IAST

- 5.3.4 RASP

- 5.4 By End-User Industry

- 5.4.1 Government

- 5.4.2 BFSI

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 IT and Telecom

- 5.4.6 Retail

- 5.4.7 Other End-User Industries

- 5.5 By Testing Tool

- 5.5.1 Web Application Testing Tool

- 5.5.2 Code Review Tool

- 5.5.3 Penetration Testing Tool

- 5.5.4 Software Testing Tool

- 5.5.5 Other Testing Tools

- 5.6 By Country

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global-level Overview, Market-level overview, Core Segments, Financials, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Accenture plc

- 6.4.2 Atos SE

- 6.4.3 Cisco Systems, Inc.

- 6.4.4 Core Security, LLC

- 6.4.5 CrowdStrike Holdings, Inc.

- 6.4.6 Fortinet, Inc.

- 6.4.7 Hewlett Packard Enterprise Company

- 6.4.8 IBM Corporation

- 6.4.9 Tenable Holdings, Inc.

- 6.4.10 Micro Focus International plc

- 6.4.11 Snyk Limited

- 6.4.12 HackerOne, Inc.

- 6.4.13 Offensive Security, LLC

- 6.4.14 Orange Cyberdefense SAS

- 6.4.15 Paladion Networks Private Limited

- 6.4.16 PricewaterhouseCoopers International Limited

- 6.4.17 Qualys, Inc.

- 6.4.18 Securonix, Inc.

- 6.4.19 Synopsys, Inc.

- 6.4.20 Veracode, Inc.

- 6.4.21 Rapid7, Inc.

- 6.4.22 Checkmarx Ltd.

- 6.4.23 NCC Group plc

- 6.4.24 TUV Rheinland AG

- 6.4.25 Bureau Veritas S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet Need Analysis