PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044137

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044137

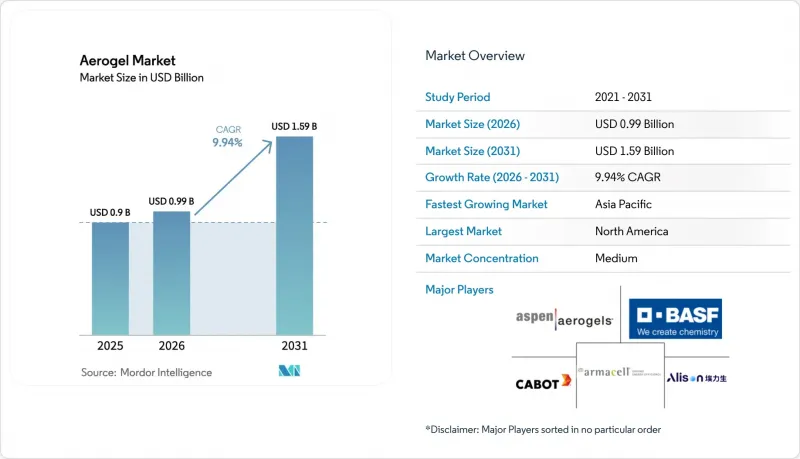

Aerogel - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Aerogel Market size is projected to expand from USD 0.90 billion in 2025 and USD 0.99 billion in 2026 to USD 1.59 billion by 2031, registering a CAGR of 9.94% between 2026 to 2031.

Mounting demand for ultra-lightweight yet thermally robust materials in energy, construction, and mobility applications keeps the growth curve steep. Heightened focus on circularity and recyclability puts aerogels in a favorable spotlight because the material can be reclaimed without large energy penalties. Steady capital expenditure on liquefied natural gas assets across Asia-Pacific, stricter building-energy rules in the United States, Canada, and Europe, and a rapid uptick in electric-vehicle battery safety retrofits jointly sustain revenue expansion in the Aerogel market. Major suppliers continue to widen production capacity, while process-streamlining steps such as ambient-pressure drying and solvent recycling progressively chip away at historical cost disadvantages.

Global Aerogel Market Trends and Insights

Rise in Adoption Owing to Reusability and Recyclability

Aerogels maintain structural integrity even after multiple service cycles, letting operators reclaim blankets or particles from pipelines, refineries, or facades without specialized tools. In offshore oil production, reused aerogel mats have logged up to three full maintenance cycles while still meeting Class A1 fire ratings. Industrial users thus cut overall lifecycle costs as landfill expense and fresh material purchases decline. Recyclability also aligns with extended-producer-responsibility provisions being rolled out in Germany, France, and several U.S. states. Government procurement teams increasingly specify circular thermal insulants, a move that strengthens the purchasing case for aerogels in public infrastructure tenders. Taken together, salvage potential and policy nudges remove earlier hesitancy around perceived wastefulness and widen the addressable Aerogel market in industrial maintenance programs.

Growing Construction Demand for High-Performance Insulation

Under mounting pressure to achieve net-zero buildings by 2030, large contractors are particularly focused on Northern Europe, where heating-degree days are notably high. Architects are turning to aerogel plasters, which, combined with silica blankets that achieve λ-values below 15 mW/m*K at densities under 200 kg/m3, allow them to meet stringent U-factor targets without resorting to thick wall sections. There's a notable opportunity in retrofitting aging multifamily units; for instance, a recent trial in Denmark showcased a significant reduction in heat loss when a 25 mm aerogel render was applied over brick facades. In U.S. climate zones 4 to 6, life-cycle models indicate a short payback period, given the current natural-gas tariffs. Such performance metrics and cost efficiencies are driving a surge in demand for aerogel blankets, fueling significant growth in the market, particularly in building envelopes.

High Production Cost Versus Conventional Insulators

Despite ongoing efforts to optimize processes, silica blankets command higher average selling prices than mineral wool, when compared on a delivered basis. In traditional batch processes, supercritical drying and solvent exchange significantly contribute to total energy consumption, driving up overhead costs. When project budgets tighten, smaller construction contractors often pivot to more affordable foams, stunting volume growth in the price-sensitive residential sector. While the introduction of rapid-cycle ambient-pressure reactors in 2026 promises to reduce energy consumption, industry experts predict a noticeable price convergence won't materialize until after 2028. This delay hinders the Aerogel market's full integration into low-margin building projects.

Other drivers and restraints analyzed in the detailed report include:

- Energy-Efficiency Regulations in North America and Europe Spur Demand

- Expansion of LNG Infrastructure Across Asia-Pacific

- Limited Availability and Price Swings of Silica Precursors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Global demand for silica aerogels stood at 72.87% of the total Aerogel market share in 2025, driven by a mature manufacturing base and broad application compatibility. Silica blankets continue to secure large oil and gas pipe insulation tenders, while powder derivatives advance as thermal additives in building plasters. The silica cohort benefits from scalable sol-gel chemistry, ample precursor availability, and a relatively benign environmental profile compared with carbonized resorcinol-formaldehyde systems. At a projected 10.87% CAGR to 2031, silica remains the backbone of overall growth, stretching the market in high-volume industrial segments.

Carbon aerogels, valued for superior electrical conductivity, gain traction in supercapacitor electrodes and EMI shielding for aerospace interiors. Still, high pyrolysis energy requirements and costly organic precursors restrain mass adoption. Alumina aerogels occupy a niche in aggressive chemical processing environments thanks to excellent acid resistance. Producers like Aspen Aerogels added a pilot alumina line in 2026, yet commercial volumes remain modest. As customers align thermal, electrical, and chemical priorities, multi-material hybrid formulations enter the commercialization funnel, hinting at gradual portfolio diversification inside the aerogel global market.

Blanket products generated 64.19% of the Aerogel market revenue in 2025 because refineries, LNG operators, and building retrofit teams value roll-out convenience and consistent handling. Pre-laminated jacketing further trims installation time, translating into lower field labor costs. Although blanket penetration stays strong, particle aerogels register the swiftest 10.92% CAGR forecast, fueled by their dispersibility in cementitious plasters and polymer masterbatches. Manufacturers can adjust thermal conductivity and density through powder integration, all without the need to redesign finished parts. While block and panel forms serve specialized roles-like daylight-transmitting facade elements and research-grade cryostats-they currently make up a small portion of the Aerogel market share.

There's a growing emphasis in research and development on monolithic panel processes, which eliminate binders for enhanced optical clarity. Pilot lines in Sweden and Japan have successfully advanced panel production techniques. If these techniques are scaled, they could open new avenues in architectural facades and solar thermal collectors, further energizing the already diverse Aerogel industry.

The Aerogel Market Report is Segmented by Type (Silica, Carbon, Alumina, and Other Types), Form (Blanket, Particle, Block, and Panel), Application (Thermal Insulation, Acoustic Insulation, and More), End-User Industry (Oil and Gas, Construction, Automotive, Marine, Aerospace, and Other End-User Industries), and Geography (Asia-Pacific, North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America retained revenue leadership with a 41.18% share of the Aerogel market in 2025, anchored by a well-established oil and gas sector in the United States and Canada and reinforced by above-average construction retrofit activity. Federal tax incentives for energy-efficient commercial buildings, coupled with LNG export terminal build-outs along the Gulf Coast, translate directly into large blanket order books. The region's mature procurement practices and robust code-enforcement culture accelerate specification of high-performance materials, underscoring North America's continuing influence on global Aerogel market dynamics.

Europe remains a premium-priced demand center, propelled by the continent's stringent building-energy laws and early adoption of electrified mobility. Countries such as Germany, Italy, and the United Kingdom channel public subsidies into deep renovation programs, catalyzing demand for particle-enhanced plasters on heritage structures where wall thickness must stay limited for aesthetic reasons. With the European Commission's 2025 Renovation Wave update driving consistent renovation activity, aerogel suppliers in the construction sector benefit from a steady pipeline. Concurrently, Norway's bolstering of its carbon-capture infrastructure carves out specialized niches for high-temperature insulation, broadening the region's income avenues.

Asia-Pacific emerges as the fastest-growing cluster with a 10.36% CAGR through 2031, riding on China's rapid LNG import ramp-up, South Korea's battery-manufacturing surge, and India's urban-infill construction boom. Regional governments intensify performance-based building codes, pushing architects toward slim, high-R-value assemblies where aerogels excel. Local blanket manufacturers like Guangdong Alison Technology secure provincial incentives for energy-efficient material lines, lowering landed costs and improving accessibility. The compound effect of industrial heat-integration programs in Japan and South Korea, plus inflows from Southeast Asian refinery upgrades, broadens the aerogel market across Asia-Pacific, enabling the region to close the gap with North America over the forecast horizon.

- Acoustiblok, Inc.

- Active Aerogels

- Aerogel Technologies, LLC

- aerogel-it

- Armacell

- Aspen Aerogels, Inc.

- BASF

- Blueshift Materials Inc.

- Cabot Corporation

- ENERSENS

- Guangdong Alison Technology Co., Ltd.

- JIOS Aerogel

- Knauf Insulation

- Nano Tech Co., Ltd.

- Ningbo Surnano Aerogel Co., Ltd

- Porex

- Sino Aerogel

- Svenska Aerogel AB

- TAASI Corporation

- Thermablok Aerogels Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rise in adoption due to re-usability and recyclability

- 4.2.2 Growing construction demand for high-performance insulation

- 4.2.3 Energy-efficiency regulations in North America and Europe spur demand

- 4.2.4 Expansion of LNG infrastructure across Asia-Pacific

- 4.2.5 Emergence of EV-battery fire-protection blankets

- 4.3 Market Restraints

- 4.3.1 High production cost vs. conventional insulators

- 4.3.2 Limited availability / price swings of silica precursors

- 4.3.3 Competition from high-performance polymer foams in buildings

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Silica

- 5.1.2 Carbon

- 5.1.3 Alumina

- 5.1.4 Other Types

- 5.2 By Form

- 5.2.1 Blanket

- 5.2.2 Particle

- 5.2.3 Block

- 5.2.4 Panel

- 5.3 By Application

- 5.3.1 Thermal Insulation

- 5.3.2 Acoustic Insulation

- 5.3.3 Catalyst and Adsorbent

- 5.3.4 Battery and Energy Storage

- 5.3.5 Day-lighting and Translucent Panels

- 5.3.6 Other Applications

- 5.4 By End-user Industry

- 5.4.1 Oil and Gas

- 5.4.2 Construction

- 5.4.3 Automotive

- 5.4.4 Marine

- 5.4.5 Aerospace

- 5.4.6 Other End-user Industries

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 India

- 5.5.1.3 Japan

- 5.5.1.4 South Korea

- 5.5.1.5 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 Italy

- 5.5.3.4 France

- 5.5.3.5 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle-East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Nigeria

- 5.5.5.5 Rest of Middle-East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)}

- 6.4.1 Acoustiblok, Inc.

- 6.4.2 Active Aerogels

- 6.4.3 Aerogel Technologies, LLC

- 6.4.4 aerogel-it

- 6.4.5 Armacell

- 6.4.6 Aspen Aerogels, Inc.

- 6.4.7 BASF

- 6.4.8 Blueshift Materials Inc.

- 6.4.9 Cabot Corporation

- 6.4.10 ENERSENS

- 6.4.11 Guangdong Alison Technology Co., Ltd.

- 6.4.12 JIOS Aerogel

- 6.4.13 Knauf Insulation

- 6.4.14 Nano Tech Co., Ltd.

- 6.4.15 Ningbo Surnano Aerogel Co., Ltd

- 6.4.16 Porex

- 6.4.17 Sino Aerogel

- 6.4.18 Svenska Aerogel AB

- 6.4.19 TAASI Corporation

- 6.4.20 Thermablok Aerogels Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment