PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044146

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044146

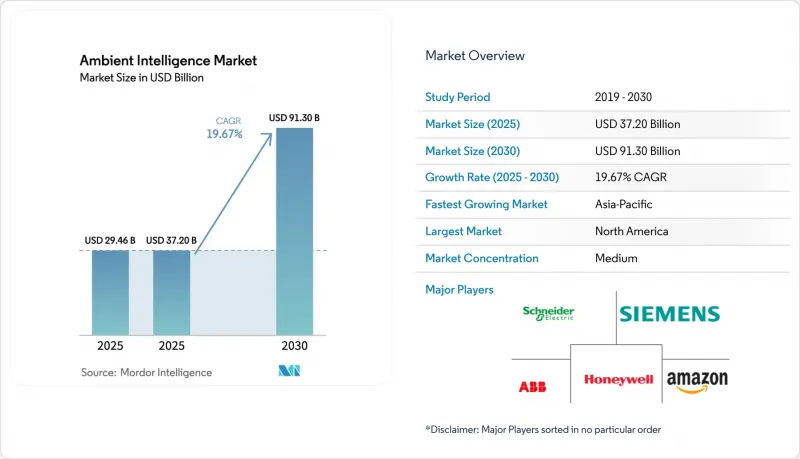

Ambient Intelligence - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2025 - 2030)

The ambient intelligence market size is expected to increase from USD 37.20 billion in 2026 to reach USD 91.30 billion by 2031, growing at a CAGR of 19.67% over 2026-2031.

Edge inference chips that consume less than 10 watts, sovereign-AI rules in major economies, and privacy-by-design mandates are accelerating commercial adoption. Hardware vendors are responding with embedded neural-processing units while service providers package predictive-maintenance contracts that stretch beyond initial installations. Smart-city capital programs in China, India, and the Gulf states are lowering deployment risk for private investors, and reimbursement codes for remote patient monitoring in the United States are widening healthcare demand. Competitive pressure is intensifying as consumer-electronics giants port smart-home ecosystems into commercial buildings, forcing industrial-automation incumbents to bundle value-added analytics with their controllers.

Global Ambient Intelligence Market Trends and Insights

Proliferation Of AI And IoT Devices

Low-power edge processors are eliminating latency linked to cloud round-trips, which is essential in automotive, industrial, and healthcare settings. Commercial smartphones now integrate ultra-wideband radios that provide centimetric positioning, demonstrating consumer hardware's readiness for enterprise workloads. Federated-learning rollouts on mobile operating systems have proven that models can improve without exporting raw data, setting precedents for privacy-preserving occupancy sensing in offices. Multi-year battery life achieved through mesh networking and power-efficient inference allows sensor grids to blanket large floorplates with minimal retrofit disruption. Deterministic networking standards are converging with these advances, enabling safety interlocks that must react within milliseconds when environmental thresholds are breached.

Government Smart-City Initiatives

China earmarked CNY 1.2 trillion (USD 168 billion) for more than 900 smart-city pilots that embed traffic, air-quality, and safety analytics, while India's Smart Cities Mission allocated INR 48,000 crore (USD 5.76 billion) across 100 urban centers. Saudi Arabia's USD 500 billion NEOM project, plus grants in Malaysia and smaller Southeast Asian economies, underscores public-sector commitment to digital urban infrastructure. These programs establish common data platforms, demonstrate measurable energy savings, and attract complementary private investments. Vendors that satisfy local content and data-sovereignty clauses gain preferential access, accelerating regional sales pipelines. The resulting reference sites validate interoperability frameworks that smaller municipalities later adopt, expanding the ambient intelligence market.

Data Security And Privacy Concerns

European regulators levied EUR 4.5 billion (USD 5.1 billion) in GDPR fines between 2018 and 2025, with ambient systems facing rising penalties for vague consent flows and excessive retention. The 2024 EU AI Act classifies public-space biometric identification as high risk, forcing lengthy conformity assessments that slow revenue conversion. U.S. healthcare providers confront HIPAA liability when sensors inadvertently capture protected health information. Although federated learning keeps raw data on-device, regulators have yet to clarify whether aggregated model updates count as personal data, creating legal ambiguity. Rising consumer awareness means buyers demand granular opt-in dashboards, raising development costs and elongating sales cycles.

Other drivers and restraints analyzed in the detailed report include:

- Demand For Energy-Efficient Smart Buildings

- Adoption Of Ambient-Assisted Living In Healthcare

- Lack Of Interoperability Standards

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hardware retained 59.61% of 2025 revenue, driven by capital outlays on sensors, gateways, and edge servers that anchor every ambient deployment. The ambient intelligence market size for services is projected to expand at a 20.17% CAGR as end users pivot toward subscription analytics, remote diagnostics, and continuous cybersecurity patching that safeguard mission-critical operations. Cost declines in microelectromechanical sensors and Bluetooth radios, along with volume production of inference accelerators, are compressing hardware margins and nudging manufacturers toward integrated offerings that wrap software and support around their devices.

Services revenue also benefits from the complexity inherent in tuning algorithms to local building physics and occupant behavior. Providers bundle domain expertise, regulatory compliance management, and outcome-based energy guarantees, creating stickier relationships than one-time equipment sales. Mergers between traditional OEMs and analytics startups foreshadow a landscape where differentiation hinges less on silicon and more on actionable insights delivered as a managed service.

Bluetooth Low Energy accounted for 24.43% technology revenue in 2025, reflecting its ubiquity in smartphones and beacon networks that enable multi-year battery life. Ultra-wideband, however, is on track to post a 21.72% CAGR through 2031 as automotive safety mandates and warehouse-robot localization demand sub-30 centimeter accuracy. The ambient intelligence market size linked to ultra-wideband benefits from IEEE 802.15.4z compliance, which fosters multivendor interoperability in emerging asset-tracking ecosystems.

Legacy RFID maintains relevance in supply-chain applications that tolerate meter-level precision, while sensor-fusion stacks integrate motion, temperature, and gas detectors to enrich contextual awareness. Edge software agents dynamically balance bandwidth and power budgets among devices, optimizing network resilience as node counts surge into the thousands. Nanotechnology-enabled sensors embedded in concrete or structural steel open new inspection workflows, while affective-computing modules surface real-time sentiment analytics in retail and healthcare environments.

Ambient Intelligence Market Report is Segmented by Component (Hardware, Software, and Services), Technology (BLE, RFID, Sensors, Biometrics, UWB, and More), End-User (Residential, Retail, Healthcare, Industrial, Office, and More), Application (Building Management, AAL, Home Automation, Retail Analytics, Manufacturing IoT, Mobility, Safety, Energy, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America held 34.84% of global revenue in 2025, supported by early smart-building retrofits, federal grants, and healthcare reimbursement codes that underwrite remote patient monitoring. U.S. municipalities leveraged USD 160 million in Smart Cities and Communities funding to pilot ambient applications that showcase carbon and operational savings. Canadian investments in privacy-preserving edge analytics align with national AI-ethics strategies, while Mexico's manufacturing clusters adopt industrial IoT to lift productivity and shore up near-shoring competitiveness. A robust cadre of system integrators distinguishes the region, shortening deployment timelines and fostering multiyear service contracts.

Asia-Pacific is projected to post a 20.44% CAGR through 2031 as China's 900-plus smart-city pilots, India's INR 48,000 crore allocation, and South Korea's USD 2.1 billion smart-city fund create fertile ground for large-scale sensor rollouts. Japan's Society 5.0 agenda embeds ambient intelligence across urban planning and disaster response, demonstrating integrated human-centric design. Australia and New Zealand concentrate on net-zero building retrofits, using occupancy analytics to meet aggressive carbon targets. Technical-standard fragmentation and data-localization statutes complicate cross-border harmonization, yet government capital outlays and rapid urbanization sustain momentum.

Europe's growth is anchored by stringent privacy and energy directives that favor on-device processing. Germany, France, the United Kingdom, Italy, and Spain capture the bulk of regional expenditure as corporate real-estate owners upgrade to comply with increasingly rigorous building-energy codes. The Middle East's greenfield megaprojects, led by Saudi Arabia's USD 500 billion NEOM and the United Arab Emirates' Smart City 2030 blueprint, integrate ambient platforms from inception, setting benchmarks for seamless occupant experiences. Africa and South America are emerging opportunity zones where mobile-first populations leapfrog fixed infrastructure, deploying battery-powered sensor networks that deliver foundational security and environmental functions despite constrained municipal budgets.

- Schneider Electric SE

- Siemens Aktiengesellschaft

- Honeywell International Inc.

- ABB Ltd.

- Amazon.com, Inc.

- Koninklijke Philips N.V.

- Johnson Controls International plc

- Google LLC

- Apple Inc.

- Microsoft Corporation

- Samsung Electronics Co., Ltd.

- Robert Bosch GmbH

- Cisco Systems, Inc.

- Legrand S.A.

- Ingersoll Rand Inc.

- Tunstall Healthcare (UK) Ltd.

- CareTech AB

- GETEMED Medizin- und Informationstechnik AG

- Televic N.V.

- VITAPHONE GmbH

- Xiaomi Corporation

- Assisted Living Technologies, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of AI and IoT Devices

- 4.2.2 Government Smart-City Initiatives

- 4.2.3 Demand for Energy-Efficient Smart Buildings

- 4.2.4 Adoption of Ambient-Assisted Living in Healthcare

- 4.2.5 Federated Learning Enhancing On-Device Context Awareness

- 4.2.6 Integration of Ambient Intelligence with Digital Twins for Predictive Facility Management

- 4.3 Market Restraints

- 4.3.1 Data Security and Privacy Concerns

- 4.3.2 Lack of Interoperability Standards

- 4.3.3 High Contextual Bias Risks in AI Decision-Making

- 4.3.4 Limited On-Device Power Budget for Complex Inference in Legacy Buildings

- 4.4 Industry Value-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Hardware

- 5.1.2 Software and Solutions

- 5.1.3 Services

- 5.2 By Technology

- 5.2.1 Bluetooth Low Energy

- 5.2.2 RFID

- 5.2.3 Sensors

- 5.2.4 Software Agents

- 5.2.5 Affective Computing

- 5.2.6 Nanotechnology

- 5.2.7 Biometrics

- 5.2.8 Ultra-Wideband

- 5.2.9 Other Technologies

- 5.3 By End-user Industry

- 5.3.1 Residential

- 5.3.2 Retail

- 5.3.3 Healthcare

- 5.3.4 Industrial

- 5.3.5 Office Building

- 5.3.6 Automotive

- 5.3.7 Automotive

- 5.3.8 Education

- 5.3.9 Other End-user Industries

- 5.4 By Application

- 5.4.1 Smart Building Management

- 5.4.2 Ambient-Assisted Living

- 5.4.3 Smart Home Automation

- 5.4.4 Smart Retail Analytics

- 5.4.5 Smart Manufacturing and Industrial IoT

- 5.4.6 Smart Mobility and Transportation

- 5.4.7 Public Safety and Security

- 5.4.8 Energy Management

- 5.4.9 Environmental Monitoring

- 5.4.10 Other Applications

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Schneider Electric SE

- 6.4.2 Siemens Aktiengesellschaft

- 6.4.3 Honeywell International Inc.

- 6.4.4 ABB Ltd.

- 6.4.5 Amazon.com, Inc.

- 6.4.6 Koninklijke Philips N.V.

- 6.4.7 Johnson Controls International plc

- 6.4.8 Google LLC

- 6.4.9 Apple Inc.

- 6.4.10 Microsoft Corporation

- 6.4.11 Samsung Electronics Co., Ltd.

- 6.4.12 Robert Bosch GmbH

- 6.4.13 Cisco Systems, Inc.

- 6.4.14 Legrand S.A.

- 6.4.15 Ingersoll Rand Inc.

- 6.4.16 Tunstall Healthcare (UK) Ltd.

- 6.4.17 CareTech AB

- 6.4.18 GETEMED Medizin- und Informationstechnik AG

- 6.4.19 Televic N.V.

- 6.4.20 VITAPHONE GmbH

- 6.4.21 Xiaomi Corporation

- 6.4.22 Assisted Living Technologies, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment