PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044151

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044151

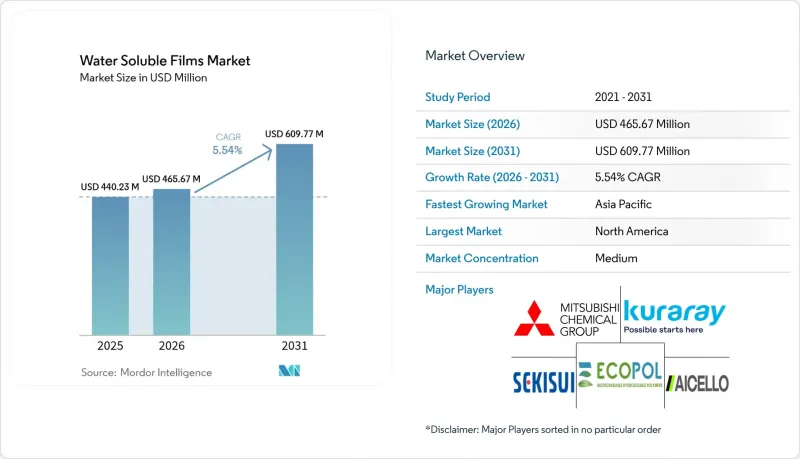

Water Soluble Films - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Water Soluble Films Market size was valued at USD 440.23 million in 2025 and is estimated to grow from USD 465.67 million in 2026 to reach USD 609.77 million by 2031, at a CAGR of 5.54% during the forecast period (2026-2031).

The growth curve rests on three pillars: rising demand for convenient unit-dose packaging, regulatory momentum favoring compostable materials, and manufacturers' success in refining cold water grades that match household washing habits. Yet progress is tempered by the high raw-material cost of polyvinyl alcohol (PVA) versus polyethylene, moisture-sensitivity that inflates logistics expenses in tropical climates, and ambiguity around future wastewater discharge limits for PVA. Competitive intensity is increasing as vertically integrated Chinese suppliers narrow the price gap with Japanese and European incumbents, while bio-based challengers explore starch or seaweed routes that could reset the cost-performance frontier over the next decade.

Global Water Soluble Films Market Trends and Insights

Surging Adoption of Unit-Dose Detergent and Dish-Wash Pods

Laundry and dishwasher brands continue to shift volume into pod formats that dissolve in ambient water, allowing concentrated actives to be delivered without residue complaints. Brands report 20-30% price premiums over bulk detergents, while opaque or bitter-coated films introduced in 2025 have cut accidental-ingestion incidents by around 30%. Penetration now stands near 45% of U.S. automatic-washer households, although handwashing prevalence keeps adoption lower in India and parts of Southeast Asia.

Expansion of Agrochemical Single-Use Sachets

Water soluble sachets eliminate measuring errors for smallholder farmers and reduce active-ingredient waste by up to 25%, helping regulators curb groundwater contamination. Subsidy programs in Maharashtra and Karnataka partially offset the 10-15% price premium versus bulk packaging, sustaining double-digit growth in India.

Moisture-Sensitivity and Shelf-Life Issues

PVA films absorb up to 10% moisture at 80% relative humidity, forcing converters to use laminated or desiccant-lined packaging that adds USD 0.05-0.08 per m2 and shortens effective shelf-life in tropical climates to as little as four months. Barrier coatings cut vapor transmission up to 60% but can slow dissolution, making a perfect balance elusive. Cold-chain distribution for pharmaceutical oral films further inflates landed costs by 15-20% in emerging markets.

Other drivers and restraints analyzed in the detailed report include:

- Global Policy Push for Biodegradable Packaging

- Edible Single-Serve Food and Beverage Sachets

- High Production Costs vs. Conventional Plastics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cold water-soluble films held 85.26% of the water soluble films market in 2025, reflecting alignment with household washing practices where 70-80% of loads use cold or warm cycles. The water soluble films market size for cold water grades is advancing at 5.75% CAGR as pod formats deepen in emerging urban centers. Ongoing R&D optimizes plasticizer blends to balance flexibility with 30-second dissolution at 20 °C, while premium hot water grades remain vital in hospital laundry and industrial dyeing where process water exceeds 60 °C.

Second-generation hot water variants command 15-20% price premiums, leveraging vinyl-acetate copolymers that delay dissolution until elevated temperatures are met, preventing premature breakdown in humid storerooms. Japan's stringent food-contact regime, enforced since mid-2025, favors incumbents able to document every additive, slowing new-entrant expansion but ensuring consistent quality in niche high-temperature applications.

The Water Soluble Films Market Report is Segmented by Type (Cold Water-Soluble Films and Hot Water-Soluble Films), Dissolution Rate (Fast-Soluble Films, Medium-Soluble Films, and Difficult-Soluble Films), End-User Industry (Packaging, Pharmaceutical and Healthcare, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

North America captured 39.91% of global volume in 2025, supported by detergent and dish-wash pod penetration above 40% in U.S. metro households. Growth decelerates because incremental adoption now depends on converting late-adopter rural consumers and diversifying into agrochemical or healthcare niches where cost hurdles persist. Voluntary safety guidelines introduced in 2024 continue to push suppliers toward opaque or bitter-coated films, adding pennies per unit but protecting brand equity.

Asia-Pacific is the fastest-growing region at 6.20% CAGR through 2031 as China and India enforce EPR mandates that penalize multilayer flexibles. Local suppliers exploit lower resin costs to expand in agrochemicals, embroidery backing, and increasingly in entry-level detergent pods sold through e-commerce platforms. Japan's 3R+Renewable incentives trigger modest substitution toward bio-based or high-biodegradability PVA variants, rewarding suppliers that certify EN 13432 compliance.

In Europe, looming 2030 recyclability and compostability deadlines intensify scrutiny of residual PVA in wastewater. Germany, France, and the United Kingdom anchor demand through high dishwasher ownership rates that value pod convenience, but potential microplastic classification could spur reformulation toward faster-biodegrading copolymers. Southern and Eastern European markets lag in infrastructure, tempering volume growth despite shared regulatory ambitions.

- AICELLO CORPORATION

- AMC (UK) Ltd

- Arrow Greentech Ltd.

- Changzhou Greencradleland Macromolecule Materials Co., Ltd.

- Cortec Corporation

- ECOMAVI SRL

- Ecopol S.p.A.

- Foshan Polyva Materials Co. Ltd

- Green Cycles

- Guangdong Proudly New Material Technology Co. Ltd

- HARKE GROUP

- INFHIDRO

- KURARAY CO., LTD.

- Mitsubishi Chemical Group Corporation

- Mondi

- Noble Industries

- Novacel

- SEKISUI CHEMICAL CO., LTD.

- Soltec Development

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging adoption of unit-dose detergent and dish-wash pods

- 4.2.2 Expansion of agrochemical single-use sachets

- 4.2.3 Global policy push for biodegradable packaging

- 4.2.4 Edible single-serve food and beverage sachets

- 4.2.5 3-D-printing dissolvable support materials

- 4.3 Market Restraints

- 4.3.1 Moisture-sensitivity and shelf-life issues

- 4.3.2 High production costs vs. conventional plastics

- 4.3.3 Tightening PVA discharge limits in wastewater

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Type

- 5.1.1 Cold Water-soluble Films

- 5.1.2 Hot Water-soluble Films

- 5.2 By Dissolution Rate

- 5.2.1 Fast-soluble Films

- 5.2.2 Medium-soluble Films

- 5.2.3 Difficult-soluble Films

- 5.3 By End-user Industry

- 5.3.1 Packaging

- 5.3.2 Textile

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Other End-user Industries

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 France

- 5.4.3.3 United Kingdom

- 5.4.3.4 Italy

- 5.4.3.5 Benelux

- 5.4.3.6 Austria

- 5.4.3.7 Czech Republic

- 5.4.3.8 Poland

- 5.4.3.9 Hungary

- 5.4.3.10 Switzerland

- 5.4.3.11 NORDIC Countries

- 5.4.3.12 Slovakia

- 5.4.3.13 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Morocco

- 5.4.5.4 Rest of Middle-East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 AICELLO CORPORATION

- 6.4.2 AMC (UK) Ltd

- 6.4.3 Arrow Greentech Ltd.

- 6.4.4 Changzhou Greencradleland Macromolecule Materials Co., Ltd.

- 6.4.5 Cortec Corporation

- 6.4.6 ECOMAVI SRL

- 6.4.7 Ecopol S.p.A.

- 6.4.8 Foshan Polyva Materials Co. Ltd

- 6.4.9 Green Cycles

- 6.4.10 Guangdong Proudly New Material Technology Co. Ltd

- 6.4.11 HARKE GROUP

- 6.4.12 INFHIDRO

- 6.4.13 KURARAY CO., LTD.

- 6.4.14 Mitsubishi Chemical Group Corporation

- 6.4.15 Mondi

- 6.4.16 Noble Industries

- 6.4.17 Novacel

- 6.4.18 SEKISUI CHEMICAL CO., LTD.

- 6.4.19 Soltec Development

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment