PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044152

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044152

Carbon Composites - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

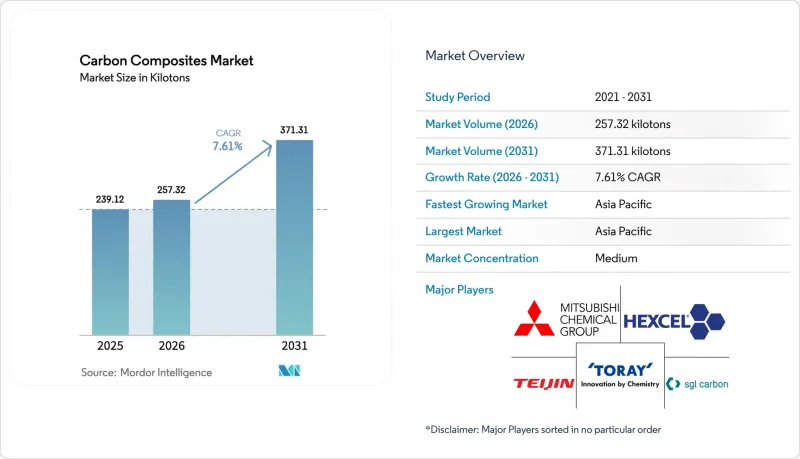

The Carbon Composites Market size is expected to increase from 239.12 kilotons in 2025 to 257.32 kilotons in 2026 and reach 371.31 kilotons by 2031, growing at a CAGR of 7.61% over 2026-2031.

Falling fiber prices, rapid offshore-wind scale-up, and the electrification push in transportation are expanding the addressable volume base for the Carbon composites market. Large-tow overcapacity in China reset average T300-grade prices to about USD 12 per kilogram by late 2024, accelerating adoption in wind-turbine blades and hydrogen vessels while compressing margins for incumbents. Automakers are gravitating toward fast-cycle thermoplastic platforms that deliver sub-5-minute part takt times, enabling structural battery-tray programs without autoclave bottlenecks. Aerospace keeps its premium share on the back of certified prepreg pipelines, yet capacity constraints in 6-meter-plus autoclaves are steering wide-body programs toward Out-of-Autoclave (OoA) resin systems.

Global Carbon Composites Market Trends and Insights

EV Range-Extension Imperative

Battery-electric models carry 400-600 kg battery packs. Carbon-fiber battery housings deliver 40-60% mass savings versus aluminum, yielding 15-25 km extra range for every 10 kg trimmed. SGL Carbon's COOLBat demonstrator reduced enclosure weight by 35% while integrating active cooling paths. Yet BMW's 2025 Neue Klasse program sidelined widespread carbon fiber use because lifecycle emissions still average 17.35 kg CO2-eq per kg of fiber under coal-based grids. Cost-competitive short-fiber thermoplastic housings priced at USD 8-10 per kg, co-developed by SABIC and Kautex, are now aimed at premium 500 km-plus range cars. The bifurcation signals that the Carbon composites market will depend on luxury and performance EVs until renewable-powered fiber lines push delivered costs toward USD 10 per kg.

Upsized Offshore Wind Blades (more than or equal to 100 m)

Blade lengths above 100 m demand carbon spar caps to meet 25-year fatigue life. MingYang's 143 m prototype uses Hengshen fiber to keep tip deflection under 8 m at rated wind speed. Dongfang Electric's 153 m blade trims 18% mass versus an all-glass layup, easing installation for floating foundations where crane-vessel rates exceed USD 500,000 per day. Vestas and Siemens Gamesa designs indicate carbon content rising from 8-12% of blade mass in 2025 to about 20% by 2030. TPI Composites reopened its Iowa plant in mid-2025 after a 10% blade price uplift driven by the longer-blade mix. As offshore additions accelerate, the Carbon composites market will benefit from 8-10 tonnes of fiber per new 12-15 MW turbine.

Al-Li and 3rd-Gen AHSS Substitution Threat

Aluminum-lithium alloys trim up to 10% weight in fuselage frames while cutting maintenance outlays by 15-20% because repairs use established metal techniques. Third-generation AHSS delivers 980-1,180 MPa strength at over 15% elongation, supporting 20-25% mass-down-gauging at markedly lower CO2 footprints. BMW's decision to skip broad carbon-fiber use on Neue Klasse EVs reflects these lifecycle and cost realities. The Carbon composites industry will remain exposed until renewable electricity systematically cuts precursor emissions.

Other drivers and restraints analyzed in the detailed report include:

- Chinese Large-Tow Price Impact (2026+)

- Hydrogen Logistics Type-IV/Type-V CFRP Vessels

- Global Autoclave Bottleneck (Wide-Body Aero)

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Polymer composites commanded 75.22% of the Carbon Composites market share in 2025 and are projected to advance at an 8.72% CAGR during the forecast period (2026-2031). Thermoplastic PEEK (Polyetheretherketone) and PPS (Polyphenylene Sulfide) parts for Airbus brackets now cure in under five minutes, while BMW i-series structures demonstrate recyclability and damage tolerance advantages. Metal-matrix and carbon-carbon formats stay at a low share because of high raw-material costs that exceed USD 500 per kg. Thermoplastic content inside the Polymer segment could rise to a nominal slice of the Carbon Composites market size by 2031 as polyamide 6 resin-transfer molding drops cycle times below 10 minutes.

Demand momentum rests on automotive battery trays, aerospace clips, and wind-blade trailing edges deploying hybrid epoxy-thermoplastic interlayers. Gurit's 98-m prototype validated the design through 5-million fatigue cycles per IEC 61400-23, cutting delamination complaints in the root end. Re-meltable thermoplastic off-cuts reduce scrap cost for tier-1 molders, buttressing the long-term sustainability narrative of the Carbon composites market.

The Carbon Composites Market Report is Segmented by Matrix (Hybrid, Metal, Ceramic, Carbon, and Polymer), Process (Prepreg Lay-Up, Pultrusion and Winding, and More), Application (Aerospace and Defense, Wind Turbines, Sports and Leisure, Civil Engineering, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle-East and Africa). The Market Forecasts are Provided in Terms of Volume (Tons).

Geography Analysis

Asia-Pacific retained 39.12% of the Carbon Composites market share in 2025, and is forecast to expand at an 8.66% CAGR during the forecast period (2026-2031). Chinese producers such as Zhongfu Shenying and Guangwei scaled large-tow lines to push domestic self-sufficiency beyond 80% in 2024, targeting 90% by 2026. Offshore-wind blade demand in Guangdong and Jiangsu alone consumed more than 10,000 tons of carbon fiber in 2025. Japan sustains leadership in T1000G and M60J high-modulus grades, with Toray's Ehime plant occupying the premium aviation niche.

North America ranks second in terms of the market share, underpinned by Hexcel prepreg supply into Boeing, Lockheed Martin, and Northrop Grumman. TPI Composites' Iowa re-opening in mid-2025 exemplifies supply-demand tightness for 100-m wind blades destined for Vineyard Wind and South Fork projects. Automotive composite uptake is moderate because the United States fuel-economy rules trail European CO2 norms, leaving cost-advantaged steel and aluminum prevalent in pickups and SUVs.

Europe's share, driven by Airbus programs and offshore-wind installations at Dogger Bank and Baltic Eagle. Germany and France lead automotive composites though BMW's strategy reset tempers volume forecasts. Gurit's Swiss engineering center and SGL Carbon's German plants secure critical mass in thermoplastic bracketry. Nordic marine applications, including electric ferries, absorb incremental composite tonnage but remain below 1,000 tons annually.

- Albany International

- China Composites Group Corporation Ltd

- Epsilon Composite

- Formosa Plastics Group

- GKN Aerospace

- Gurit Services AG

- Hexcel Corporation

- Huntsman International LLC

- Hyosung Advanced Materials

- Mitsubishi Chemical Group Corporation

- Nippon Carbon Co. Ltd

- Plasan

- Rockman

- SGL Carbon

- Syensqo

- Teijin Limited

- TORAY INDUSTRIES INC.

- TPI Composites

- Zoltek Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EV range-extension imperative

- 4.2.2 Upsized offshore wind blades (more than or equal to 100 m)

- 4.2.3 Chinese large-tow CF over-capacity price impact (2026+)

- 4.2.4 Hydrogen logistics Type-IV/Type-V CFRP vessels

- 4.2.5 Space-launch demand for reusable CFRP cryo-tanks

- 4.3 Market Restraints

- 4.3.1 Al-Li and 3rd-gen AHSS substitution threat

- 4.3.2 Global autoclave bottleneck (wide-body aero)

- 4.3.3 PFAS-linked bans on fluorinated sizing agents

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Degree of Competition

5 Market Size & Growth Forecasts (Volume)

- 5.1 By Matrix

- 5.1.1 Hybrid

- 5.1.2 Metal

- 5.1.3 Ceramic

- 5.1.4 Carbon

- 5.1.5 Polymer

- 5.1.5.1 Thermosetting

- 5.1.5.2 Thermoplastic

- 5.2 By Process

- 5.2.1 Prepreg Lay-up

- 5.2.2 Pultrusion and Winding

- 5.2.3 Wet Lamination and Infusion

- 5.2.4 Press and Injection Processes

- 5.2.5 Other Processes

- 5.3 By Application

- 5.3.1 Aerospace and Defense

- 5.3.2 Automotive

- 5.3.3 Wind Turbines

- 5.3.4 Sports and Leisure

- 5.3.5 Civil Engineering

- 5.3.6 Marine

- 5.3.7 Other Applications

- 5.4 By Geography

- 5.4.1 Asia-Pacific

- 5.4.1.1 China

- 5.4.1.2 India

- 5.4.1.3 Japan

- 5.4.1.4 South Korea

- 5.4.1.5 ASEAN Countries

- 5.4.1.6 Rest of Asia-Pacific

- 5.4.2 North America

- 5.4.2.1 United States

- 5.4.2.2 Canada

- 5.4.2.3 Mexico

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 NORDIC Countries

- 5.4.3.7 Russia

- 5.4.3.8 Rest of Europe

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle-East and Africa

- 5.4.5.1 Saudi Arabia

- 5.4.5.2 South Africa

- 5.4.5.3 Rest of Middle East and Africa

- 5.4.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share(%)/Ranking Analysis

- 6.4 Company Profiles (includes Global Overview, Market Overview, Core Segments, Financials, Strategic Information, Products and Services, Recent Developments)

- 6.4.1 Albany International

- 6.4.2 China Composites Group Corporation Ltd

- 6.4.3 Epsilon Composite

- 6.4.4 Formosa Plastics Group

- 6.4.5 GKN Aerospace

- 6.4.6 Gurit Services AG

- 6.4.7 Hexcel Corporation

- 6.4.8 Huntsman International LLC

- 6.4.9 Hyosung Advanced Materials

- 6.4.10 Mitsubishi Chemical Group Corporation

- 6.4.11 Nippon Carbon Co. Ltd

- 6.4.12 Plasan

- 6.4.13 Rockman

- 6.4.14 SGL Carbon

- 6.4.15 Syensqo

- 6.4.16 Teijin Limited

- 6.4.17 TORAY INDUSTRIES INC.

- 6.4.18 TPI Composites

- 6.4.19 Zoltek Corporation

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-need Assessment