PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044157

PUBLISHER: Mordor Intelligence | PRODUCT CODE: 2044157

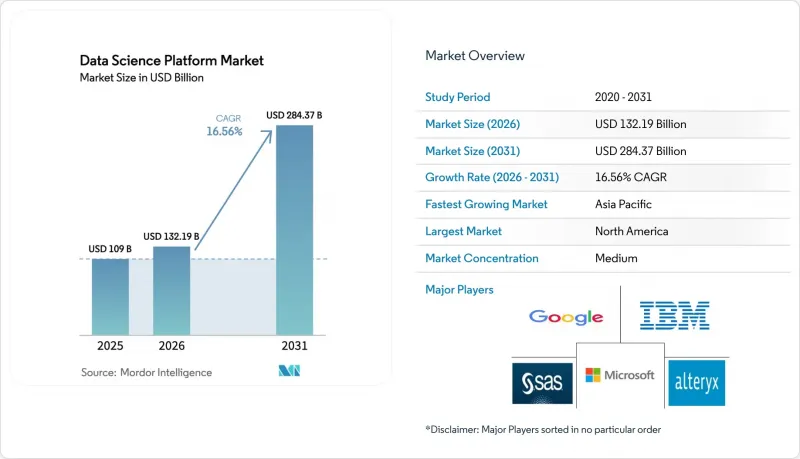

Data Science Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031)

The Data Science Platform Market size is expected to increase from USD 109 billion in 2025 to USD 132.19 billion in 2026 and reach USD 284.37 billion by 2031, growing at a CAGR of 16.56% over 2026-2031.

Steady growth is unfolding as enterprises shift from isolated machine-learning pilots toward production systems that integrate data ingestion, model training, governance, and edge inference. Integrated toolchains promise faster time-to-value, while hyperscalers bundle advanced functionality into existing cloud contracts, compressing margins for niche vendors. Meanwhile, domain-specific foundation models are redefining use cases in healthcare and finance, and sovereign AI programs are channeling billions of dollars into regional data centers and GPU clusters. Competitive positioning now hinges on seamless governance, feature-store performance, and the ability to serve retrieval-augmented generation workloads at scale.

Global Data Science Platform Market Trends and Insights

Proliferation of Open-Source ML Frameworks Catalyzing Platform Convergence

Open-source libraries power 87% of AI workloads, up eight percentage points from 2024, intensifying vendor competition on orchestration, governance, and enterprise support rather than core algorithms. Python remains the dominant language, with 66% adoption, as firms consolidate toolchains to curb training overhead. Security gaps in community packages push many buyers toward commercial distributions that bundle CVE scanning and license compliance, adding momentum to enterprise-grade open-source support models. Databricks built MLflow natively into its platform, enabling model versioning across TensorFlow, PyTorch, and scikit-learn without lock-in, a feature set that underpinned its record USD 10 billion Series J round in 2024. As hyperscalers bundle similar tooling at marginal cost, margins for niche AutoML vendors continue to compress.

Stricter Model-Governance Regulations Boosting Managed Platforms

The European Union AI Act, in force since August 2024, requires conformity assessments for high-risk AI systems, steering organizations toward platforms with built-in audit trails and explainability modules. Complementary banking guidance from the Basel Committee demands rigorous model validation and third-party audits. The United States FDA updated software-as-a-medical-device guidance in January 2025, specifying pre-market submissions and post-market surveillance protocols that platforms with strong version control handle more efficiently. IBM's watsonx.governance, launched 2024, automates EU AI Act reporting, trimming legal review cycles from weeks to days. Vendors lacking dedicated compliance teams risk disqualification from large enterprise bids.

Data-Residency Barriers Hindering Multi-Region Roll-Outs In Public Sector EU

GDPR Article 44 and national statutes prohibit transferring citizen data to non-EU regions without adequacy safeguards. The Gaia-X initiative lagged deployment by 18 months, delaying Azure and AWS migrations for French and German ministries. France's ministries postponed platform adoption until OVHcloud and T-Systems certified sovereign offerings. The EU Cloud Code of Conduct added further compliance layers that smaller vendors struggle to absorb. Resulting fragmentation pushes agencies toward on-premise or local-cloud installations, limiting economies of scale for global providers.

Other drivers and restraints analyzed in the detailed report include:

- Edge-To-Cloud Fabric Adoption Enabling Hybrid Platforms In Manufacturing

- Unstructured Video And IoT Data Explosion Requiring Scalable Feature Stores

- Shortage Of ML-Ops Engineers Undermining Complex Deployments

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services are poised for a 17.8% CAGR through 2031, nearly double that of platforms, as enterprises confront talent shortages. Databricks logged a 48% rise in professional services revenue in fiscal 2024, driven by lakehouse migration projects. IBM secured a USD 500 million banking contract in 2024 to deploy watsonx across 12 countries. Accenture and Microsoft staffed 2,500 new MLOps specialists for their joint practice, reflecting demand for advisory services. Vendors now embed success plans, dedicated architects, and quarterly reviews into annual subscriptions, recognizing that licenses rarely account for more than 40% of total cost of ownership.

Platform providers also court niche consultancies to reach mid-market buyers. Slalom and Deloitte launched dedicated data-science practices in 2024, filling a gap where hyperscaler advisory teams remain focused on flagship accounts. This collaboration underscores the Data Science Platform market's pivot toward blended software-plus-services contracts that guarantee outcome-based milestones and ongoing optimization.

Cloud computing held 67.50% share in 2025, and the Data Science Platform market size tied to cloud deployments is projected to grow at an 18.4% CAGR through 2031. Training a 70-billion-parameter model on AWS SageMaker costs roughly USD 350,000 per run and avoids the USD 15 million capital outlay for on-premises clusters. Microsoft added spot instances to Azure ML in 2024, cutting certain training costs by up to 80%. Google's Vertex AI Pipelines cut operational overhead by 60% compared with self-managed Kubernetes clusters.

On-premise deployments survive in tightly regulated environments. Basel III compliance favors in-house control among financial institutions. Hybrid designs bridge both worlds, with Databricks Unity Catalog offering unified governance across multi-cloud and on-premise estates. HPE's GreenLake for Machine Learning Operations delivers consumption-based pricing for on-premise hardware.

The Data Science Platform Market Report is Segmented by Product Offering (Platform, and Services), Deployment (On-Premise, and Cloud), Enterprise Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (IT and Telecom, BFSI, Retail and E-Commerce, Manufacturing, Energy and Utilities, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

North America claimed 47.23% share in 2025, supported by hyperscaler capacity and USD 25 billion in venture funding during 2024. The U.S. Executive Order on AI requires federal agencies to adopt governance frameworks, fueling demand for compliant platforms. Canada's Vector Institute trains 500 researchers a year, buoying domestic adoption.

Asia-Pacific is forecast for a 17.1% CAGR. In Western Asia, Saudi Arabia dedicated USD 100 billion to regional AI infrastructure, partnering with Huawei and Oracle, and the United Arab Emirates released open-source Falcon LLMs to reduce reliance on U.S. models. Japan pledged JPY 2 trillion (USD 13.4 billion) to AI chip fabrication and data center construction. China's market still expands despite export controls, propelled by domestic accelerators. India's Digital India initiative drove 35% year-over-year cloud-platform adoption in 2024.

Europe's trajectory is flatter due to residency mandates. Germany delayed public-sector migrations pending Gaia-X certification. The U.K. AI Safety Institute is crafting testing protocols that require robust safety guardrails. South America's growth centers on Brazilian banks deploying SageMaker for fraud detection. Middle East programs focus on smart-city mobility, as Dubai's traffic-optimization models trimmed congestion by 12%. African adoption remains nascent, limited to telecom churn-prediction pilots.

- IBM Corporation

- Google LLC (Alphabet Inc.)

- Microsoft Corporation

- Alteryx Inc.

- SAS Institute Inc.

- Databricks Inc.

- Snowflake Inc.

- Amazon Web Services Inc.

- The MathWorks Inc.

- RapidMiner Inc.

- DataRobot Inc.

- H2O.ai

- TIBCO Software Inc.

- KNIME GmbH

- Domino Data Lab Inc.

- Oracle Corporation

- SAP SE

- Cloudera Inc.

- Qlik Tech International

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Proliferation of Open-Source ML Frameworks Driving Platform Convergence

- 4.2.2 Stricter Model-Governance Regulations Boosting Managed Platforms

- 4.2.3 Edge-to-Cloud Fabric Adoption Enabling Hybrid Platforms in Manufacturing

- 4.2.4 Unstructured Video and IoT Data Explosion Requiring Scalable Feature Stores

- 4.2.5 Rise of Domain-Specific Foundation Models Accelerating Vertical Platforms

- 4.2.6 GPU Supply-Chain Localisation Policies Steering Regional Platform Build-outs

- 4.3 Market Restraints

- 4.3.1 Data-Residency Barriers Hindering Multi-Region Roll-outs in Public Sector EU

- 4.3.2 Shortage of ML-Ops Engineers Undermining Complex Deployments

- 4.3.3 Escalating Cloud Bills Creating Budget Pushback for Real-Time Training

- 4.3.4 Legacy Data Silos in Energy and Utilities Delaying Platform ROI

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Offering

- 5.1.1 Platform

- 5.1.2 Services

- 5.2 By Deployment

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Enterprise Size

- 5.3.1 Small and Medium Enterprises

- 5.3.2 Large Enterprises

- 5.4 By End-user Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Retail and E-commerce

- 5.4.4 Manufacturing

- 5.4.5 Energy and Utilities

- 5.4.6 Healthcare and Life Sciences

- 5.4.7 Government and Defense

- 5.4.8 Rest of End-user Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Egypt

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 IBM Corporation

- 6.4.2 Google LLC (Alphabet Inc.)

- 6.4.3 Microsoft Corporation

- 6.4.4 Alteryx Inc.

- 6.4.5 SAS Institute Inc.

- 6.4.6 Databricks Inc.

- 6.4.7 Snowflake Inc.

- 6.4.8 Amazon Web Services Inc.

- 6.4.9 The MathWorks Inc.

- 6.4.10 RapidMiner Inc.

- 6.4.11 DataRobot Inc.

- 6.4.12 H2O.ai

- 6.4.13 TIBCO Software Inc.

- 6.4.14 KNIME GmbH

- 6.4.15 Domino Data Lab Inc.

- 6.4.16 Oracle Corporation

- 6.4.17 SAP SE

- 6.4.18 Cloudera Inc.

- 6.4.19 Qlik Tech International

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment